DO YOU WANT TO RESEARCH FINANCIAL MARKETS?

Quant Research, Systematic Investment and Algorithmic Trading

Not sure where to begin?

Here’s a quick roadmap to guide you through the highlights of this newsletter.

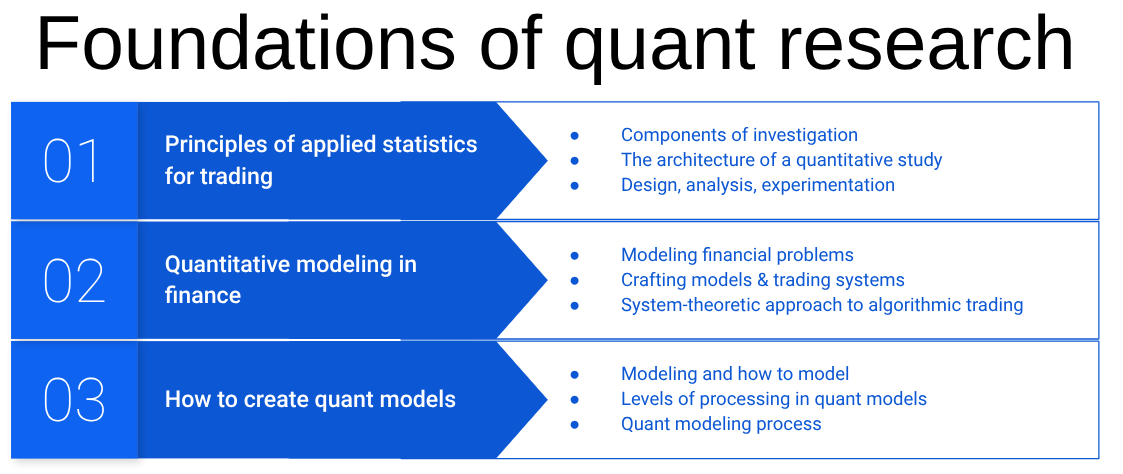

The nature of a quantitative trading hypothesis:

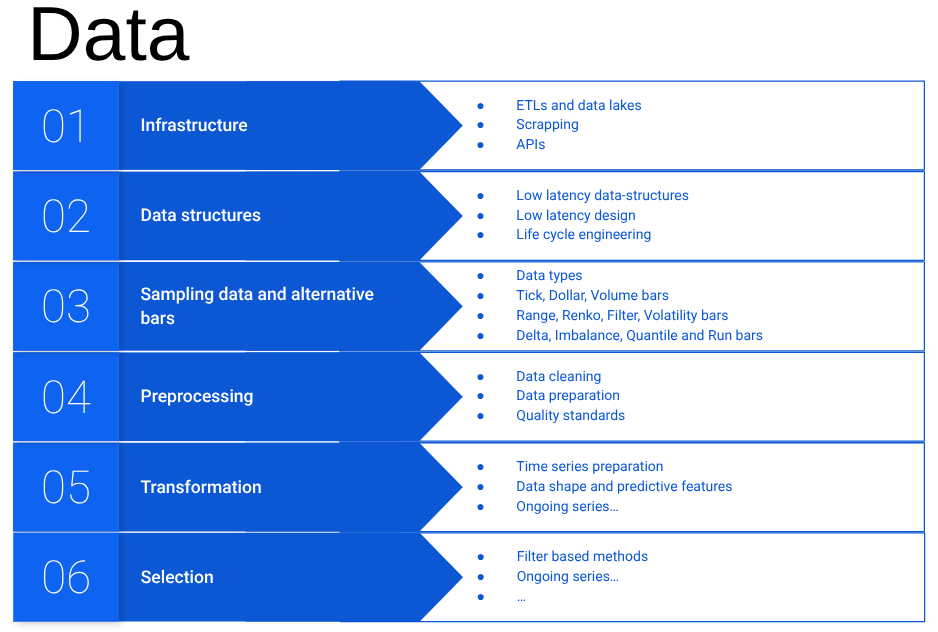

Infrastructure:

Data structures:

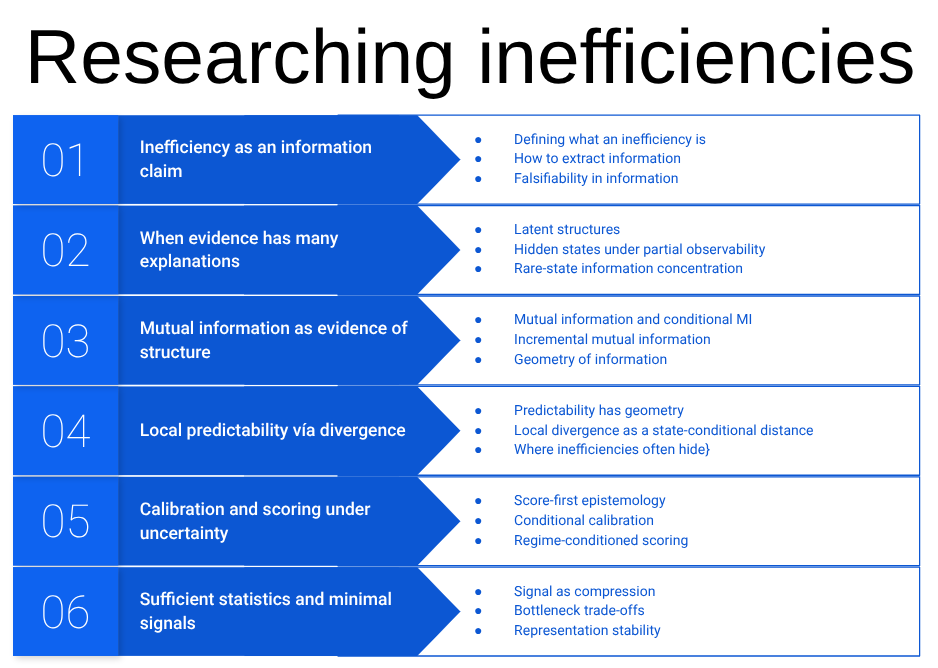

Sampling data and alternative bars:

Preprocessing:

Transformation:

Selection

Ongoing series…

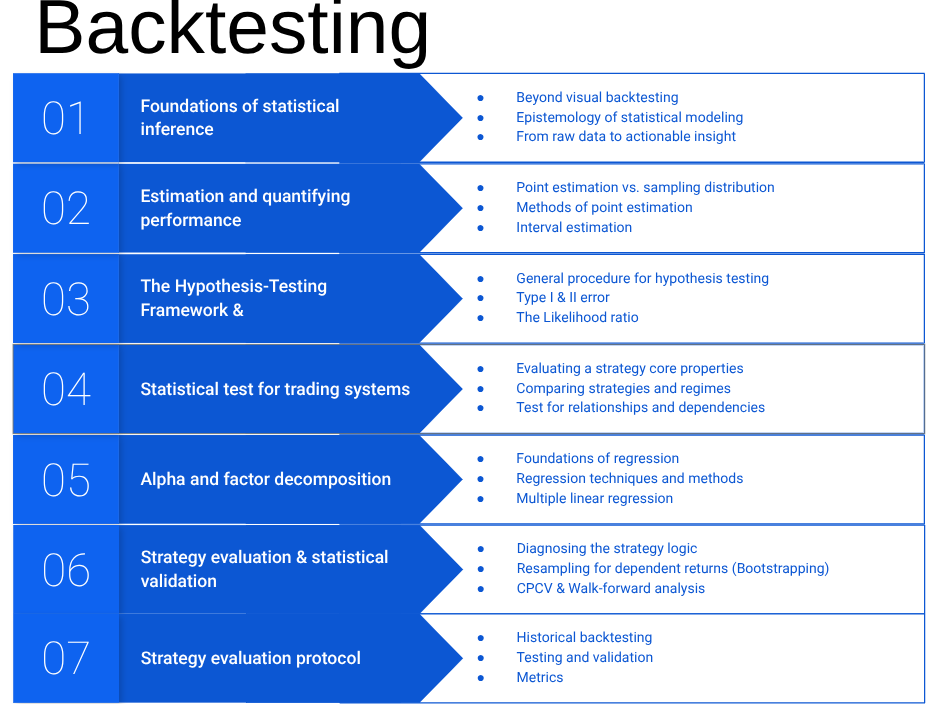

Strategy evaluation protocol:

This is a small sample of what you’ll find here. Through this newsletter, I’m excited to share the insights, strategies, and behind-the-scenes moments that shape my work.

Whether you’re a curious investor or a seasoned quant, I’m here to challenge conventional thinking, inspire bold ideas, and guide you through the complex, ever-evolving world of quantitative finance.

Let’s explore the future together!

For now, buckle up—it’s gonna be a wild ride.

—Quant Beckman

Founder of Trading the Breaking

Continue sharing your information, thanks!