Portfolio: Portfolio of uncorrelated systems

Uncover the hidden dangers of correlated trading bots—before your portfolio pays the price

Table of contents:

Introduction.

Bots doing their homework.

The portfolio zoo—aka mix of bot strategies.

What are the dangers of having correlated bots?

Guide to building a portfolio of uncorrelated systems.

Balancing wins and losses.

Before you begin, remember that you have an index with the newsletter content organized by clicking on “Read full story” in this image.

Introduction

Trading bots are like the star players in a high-stakes orchestra—each with its own instrument, playing a unique tune. But when they’re all jamming together in the same portfolio, their harmony (or lack thereof) can either create a masterpiece or a cacophony. Today, we’re diving into the world of trading bots and how their interactions can make your portfolio sing or screech. The key idea? If bots move in sync, your portfolio can skyrocket or nosedive. But if they dance to their own beats, you’ll enjoy smoother, more predictable returns.

Let’s kick things off by decoding what a bot’s “PnL” really means and how to tell if two bots are best buddies or bitter rivals.

Bots doing their homework

In the trading world, PnL—Profit and Loss—is like a bot’s report card. It tells you how well the bot is performing. When we say two bots have correlated PnL, it means they tend to score high or low at the same time. This is measured using the correlation coefficient, denoted by ρ.

The correlation coefficient between two bots’ PnLs, PnLA and PnLB, is calculated as follows:

Where:

Covariance (Cov) measures how two variables move together.

σA and σB are the standard deviations of the PnLs of Bot A and Bot B.

If ρPnL = 1, the bots are perfectly correlated—they move exactly in sync. If ρPnL = −1, they are perfectly anti-correlated—when one wins, the other hedge losses. And if ρPnL = 0, their moves are independent. Think of it like two classmates: sometimes they work together on a project—high correlation—and sometimes they work separately—zero correlation.

Our goal is for them to work independently, together but not mixed. The higher the correlation, the greater the risk. And a negative correlation can either be a real disaster or a well-coordinated portfolio of systems.

A simple example. Consider two bots:

Bot A trades technology stocks.

Bot B also trades technology stocks.

If both bots take a hit on the same day because of a tech crash, they’re highly correlated. But if one bot loses while the other gains—maybe by trading different sectors—they’re uncorrelated or even negatively correlated.

Now that we have defined PnL correlation, let’s look at how mixing different types of bots creates a diverse portfolio—much like mixing different flavors in a juice!

The portfolio zoo—aka mix of bot strategies

Different bots follow different strategies. Here are three common types:

Arbitrage bot: The sneaky ninja of trading, exploiting tiny price differences between markets.

Trend-following bot: The surfer, riding the waves of rising or falling markets.

Mean-reversion bot: The bargain hunter, buying low and selling high when prices return to average.

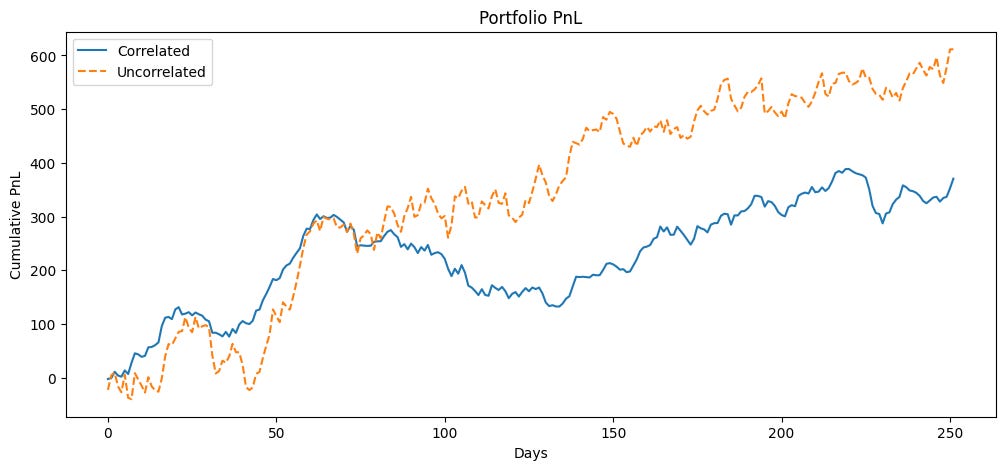

When these bots have uncorrelated PnLs, combining them creates a robust portfolio. It’s like a zoo where lions, penguins, and sloths all contribute in their own unique ways. The result? Their risks don’t pile up destructively. And example here:

The cumulative PnLs are plotted to show how the portfolios perform over time. The uncorrelated portfolio is expected to be smoother, while the correlated one might exhibit more volatility.

After seeing how a mix of bots affects your portfolio’s performance, the next natural question is: What happens when all the bots decide to behave in the same way?

What are the dangers of having correlated bots?

When multiple bots chase the same market signals, their PnLs become highly correlated. This scenario is dangerous because it means that when one bot makes a mistake, all of them do. Think of it as a sports team where every player runs in the same direction—if that direction turns out to be wrong, the whole team suffers.

The variance of a portfolio consisting of N bots can be expressed as:

Here, wi is the weight—or allocation—to bot i, σi is its standard deviation, and ρij is the correlation between bots i and j.

If ρij ≈ 1 for all pairs:

The second term adds up dramatically, making the portfolio extremely volatile. This is like building a tower out of jelly—it collapses easily!

Remember 2018? Several hedge funds using similar momentum strategies experienced massive losses because their bots acted in unison. When one bot dropped, others followed, and the losses compounded.

Knowing the dangers of highly correlated bots, let’s move to a practical guide on how to build an uncorrelated bot army. This is where the diversity of system typologies becomes your best friend—and by systems I don't mean vectors, but this is something we will cover in future articles.