Table of contents:

Introduction.

Architectural elements of position sizing.

Quantitative signal analysis.

Volatility-responsive calibration.

Portfolio correlation architecture.

Exit valuation mechanics.

Strategic deployment patterns.

Minimal position deployment protocol.

Maximum position deployment protocol.

Aggressive allocation dynamics.

Execution and framework integration.

Geometric position scaling.

Capital-risk calibration matrix.

Moderate-opportunity impact assessment.

Algorithmic positioning.

Optimization framework.

Integration of temporal dimensions.

Continuous recalibration mechanisms.

RiskOps paradigm.

Before you begin, remember that you have an index with the newsletter content organized by clicking on “Read full story” in this image.

Introduction

Algorithmic traders face a perpetual paradox: How much capital should be committed to each opportunity? This isn't merely a question of numbers—it's the fundamental tension that defines successful algorithmic trading strategies.

Imagine yourself standing at the edge of a vast financial market, algorithms humming beneath your feet, each one scanning millions of price movements per second. Your trading system has detected a promising signal—perhaps a statistical anomaly in the futures market or a fleeting correlation pattern across currency pairs. The question that follows is deceptively simple yet profoundly consequential: how much of your capital should you deploy?

This decision—position sizing—represents the fulcrum upon which algorithmic trading success balances. Too timid, and even the most brilliant strategy yields negligible returns. Too aggressive, and a single market hiccup can devastate your capital base. Worse still, the optimal answer shifts continuously as market conditions evolve.

The risks lurking within this decision matrix are manifold:

Allocation imbalance risk: Deploying excessive capital to correlated assets, potentially magnifying losses during sector-wide movements.

Volatility misjudgment risk: Failing to adjust position sizes appropriately as market turbulence changes.

Exit opportunity risk: Insufficient consideration of how quickly positions can be unwound in various market conditions.

Signal confidence miscalibration: Over-allocating to weaker signals or under-allocating to high-conviction opportunities.

The pivotal moment that crystallizes this dilemma often arrives without fanfare—perhaps when an algorithm encounters its first genuine market crisis, or when a previously reliable signal suddenly falters across multiple assets simultaneously. This critical juncture forces a fundamental reassessment of how position sizing decisions are made within the algorithmic framework.

Architectural elements of position sizing

Position sizing in algorithmic trading is far more than a simple fixed percentage or a static rule applied uniformly across all opportunities. Instead, in systemaric approaches, it represents a dynamic and critical architectural layer, weaving together multiple quantitative and contextual factors to determine the optimal capital allocation for each trade at any given moment. This complex interplay of variables dictates not just what to trade, but how much, fundamentally shaping the risk profile and return potential of the entire portfolio.

Quantitative signal analysis

At the heart of position sizing lies the algorithm's capacity to quantify its own edge. The strategy advantage—a mathematical representation of the algorithm's statistical edge—serves as the primary regulator of trading frequency. Like a master conductor determining the tempo of a symphony, this dictates the rhythm of market engagement.

High-conviction represents moments when the algorithm detects particularly strong signals—perhaps when multiple independent factors align in perfect mathematical harmony. During these rare convergences, the algorithm may justifiably increase position sizes, much as a poker player might raise significantly when holding a royal flush.

The dynamic relationship between these advantages creates an algorithmic tension: when to maintain consistent position sizes versus when to amplify capital deployment in response to exceptional opportunities.

Volatility-responsive calibration

Market volatility acts as both threat and opportunity—a dualistic force requiring response mechanisms. Consider the algorithm as a sailor navigating treacherous waters:

In calm seas—low-volatility markets—smaller sails—position sizes—suffice, as dramatic progress is unlikely. In moderate winds—trending markets—larger sails capture more energy. But when storms rage—extreme volatility—sail area must be reduced again to prevent capsizing.

This sailing metaphor illustrates the non-linear relationship between volatility and optimal position sizing—a relationship that many algorithmic systems fail to properly encode, creating exploitable inefficiencies for more competitors.

Portfolio correlation architecture

The number of correlated assets within the portfolio creates a complex mathematical relationship affecting individual position sizes. As correlation increases, the effective risk concentration intensifies, even when nominal position sizes remain constant.

Imagine a multi-dimensional chess game where each piece's movement affects the vulnerability of others. An algorithm must maintain awareness of these invisible connections, dynamically adjusting individual position sizes as correlation structures evolve—often imperceptibly to human observers.

Exit valuation mechanics

The value of exit opportunity introduces a fascinating temporal dimension to position sizing. This concept quantifies the expected utility of terminating positions under various market conditions.

When the potential value of rapid position exit is low—perhaps in a range-bound market where quick directional moves are improbable—smaller positions become optimal. Conversely, when exit value is high—during trend formation phases or volatility breakouts—larger positions may capture greater value, provided appropriate risk constraints remain in place.

This dynamic exit valuation creates a feedback loop within algorithms, allowing them to modify position sizes not just based on entry conditions, but on expected exit scenarios—a form of temporal arbitrage invisible to other systems.

Strategic deployment patterns

Effective position sizing extends beyond calculating the optimal allocation for a single trade; it involves adopting overarching strategic deployment patterns that dictate the aggregate approach to capital allocation based on prevailing market conditions, the nature of available trading opportunities, and the portfolio's current state.

Rather than applying a monolithic sizing rule, algorithms dynamically select from distinct deployment protocols, each designed to optimize outcomes under specific circumstances:

This strategic layer ensures that the algorithm's capital is not merely allocated, but deployed in a manner aligned with the immediate tactical needs and long-term objectives, ranging from prioritizing capital preservation in uncertain times to aggressively pursuing growth during periods of exceptional opportunity.

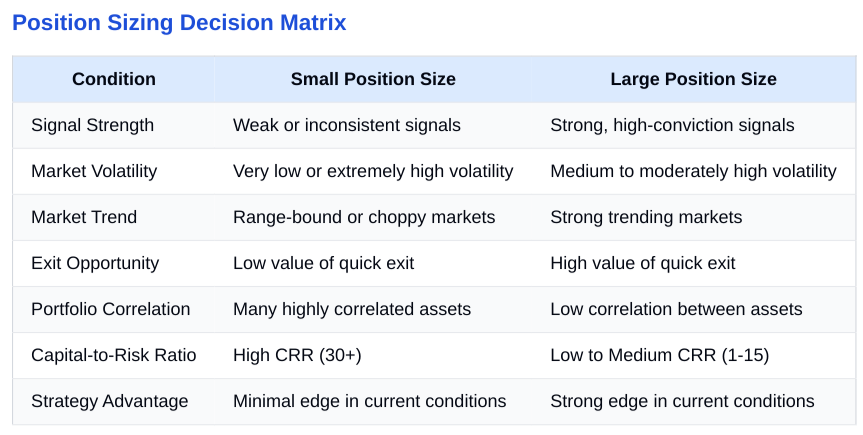

Minimal position deployment protocol

Small position sizes become optimal under specific market conditions and signal configurations. These situations represent scenarios where capital preservation takes precedence over aggressive growth, creating a conservative deployment pattern focused on longevity rather than explosive returns.

The algorithm may adopt minimal position sizing when:

Market signals suggest potential adverse movements of significant magnitude.

The strategy detects few high-return opportunities relative to risk.

Quick position exit would provide minimal value—low exit opportunity value.

The portfolio contains numerous moderate-potential positions requiring protection.

High-conviction opportunities are scarce.

Markets exhibit strong range-bound characteristics.

The algorithm detects high-probability but low-magnitude opportunities.

Market volatility reaches extreme levels, exceeding historical calibration parameters.

Strong mean-reversion patterns dominate price action.

Counter-trend strategies appear dominant among market participants.

Each of these conditions creates a mathematical environment where capital preservation through position size restriction optimizes the algorithm's long-term expectancy, even at the cost of immediate profit potential.

Maximum position deployment protocol

Conversely, large position sizes become optimal when market conditions and signal quality align to create exceptional opportunities. These represent moments when the algorithm can justifiably concentrate capital to maximize return potential while maintaining acceptable risk parameters.

The algorithm may implement maximum position sizing when:

Signals indicate minimal potential for adverse price movement—like Trump news.

Numerous high-quality opportunities present favorable return-to-risk ratios.

Rapid exit would provide substantial value—high exit opportunity value.

The strategy detects multiple high-conviction signals simultaneously.

The algorithmic framework naturally focuses on high-magnitude price movements.

Dynamic or trending markets create substantial directional bias.

Protection against unfavorable reversals remains cost-effective.

Strong directional signals align with favorable market structure.

Market conditions decisively favor the algorithm's strategic approach.

Few moderate-potential trades compete for capital allocation.

These conditions create an environment where concentrated capital deployment optimizes expected returns without excessive risk exposure—the algorithmic equivalent of pressing a strong advantage.

Aggressive allocation dynamics