Table of contents:

Introduction.

Risks and limitations of the strategy.

The mathematical anatomy of the Iron Condor.

The Greeks.

Beyond the payoff diagram.

Trading Vega.

Algorithmic entry and strike selection logic.

Before you begin, remember that you have an index with the newsletter content organized by clicking on “Read full story” in this image.

Introduction

The iron condor’s appeal is statistically seductive: a high-probability, defined-risk structure promising steady income from time decay and volatility erosion. Yet beneath its deceptively flat payoff profile lies a quantitatively intricate reality—one where theoretical win rates often mask a negative expected value. This isn’t a flaw in the strategy itself, but a consequence of its dynamic risk profile and the operational friction inherent in live trading.

The core paradox is straightforward: a position boasting a 90% theoretical probability of profit (POP) can systematically underperform due to three quantifiable forces. First, negative gamma accelerates losses nonlinearly as the underlying breaches short strikes, transforming modest moves into structural damage. Second, negative vega exposes the position to volatility shocks—where a spike in implied volatility alone can erase gains without price breaching strikes. Third, transaction costs—bid-ask spreads, multi-leg slippage, and execution latency—systematically erode the edge, particularly in high-turnover regimes. Together, these factors invert the strategy’s apparent statistical edge: frequent small wins are overwhelmed by infrequent but severe losses, yielding a negative Sharpe ratio despite the comforting 90% POP.

This isn’t a retail-trader cautionary tale. For systematic traders, the challenge is structural: How do you isolate and neutralize the latent risks that backtests obscure? Static payoff diagrams ignore the path-dependent dynamics of the Greeks; naive strike selection ignores volatility surface curvature; and "set-and-forget" execution ignores real-world market microstructure. The solution demands a rigorous, adaptive framework—one that treats the iron condor not as a static trade, but as a dynamic system requiring continuous recalibration of risk exposure, strike selection, and adjustment triggers.

Today we dissect that framework. We move beyond the oversimplified narrative of selling volatility to address the quantifiable mechanics of this strategy. For deeper insights check this:

The goal isn’t to promise consistent profits, but to define the precise conditions under which the strategy’s statistical edge could survive the market. However, in future articles we will see that there are many more latent pitfalls due to the Black Scholes model and that they will be addressed with an arbitrage-aware framework.

Risks and limitations of the strategy

The primary risk of the Iron Condor strategy is its asymmetric risk/reward profile: you accept the low probability of a potentially large loss in exchange for the high probability of a small, limited gain.

Market-related risks:

While the strategy profits from a sideways market, a sharp, significant price movement in either direction can cause substantial losses. Due to the position's negative gamma—direction risk—these losses accelerate the further the price moves against you. A small move might be manageable, but a fast, large move can quickly erase the initial premium and lead to the maximum loss.

An Iron Condor is a short volatility strategy—Vega risk. This means it profits when implied volatility (IV) decreases or stays the same. If market fear spikes and implied volatility rises suddenly, the value of your position will decrease, creating a loss even if the underlying price hasn't breached your short strikes.

Strategy-specific risks & limitations:

Your maximum profit is always capped at the net credit you received when you opened the trade. You can never make more than this initial amount, no matter how perfectly the trade works out.

Typically, the maximum potential loss on an Iron Condor is significantly greater than the maximum potential profit. For example, you might risk $850 to make a maximum of $150. This means one max-loss trade can wipe out the gains from five or more winning trades.

The high probability and defined risk nature can make traders complacent. While the maximum loss is defined, it is often a substantial amount of capital. A high win rate does not guarantee long-term profitability if the few losing trades are not managed correctly.

If you are trading American-style options—like those on most individual stocks—the person who bought the options from you can exercise their right to assign you shares at any time before expiration. This can force you into an unexpected stock position (either long or short) and disrupt your strategy—assignment risk.

The mathematical anatomy of the Iron Condor

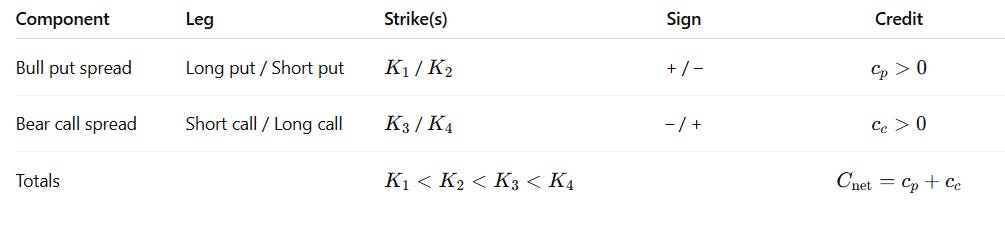

Before we can automate, we must first define. The Iron Condor is a four-legged options strategy composed of two distinct vertical spreads: a bear call spread and a bull put spread. The key is that both spreads are sold, making it a net credit strategy, and they are centered around the current price of the underlying asset, creating a market-neutral stance.

Let's define the elements that translate the relationships of the strategy into mathematical equations.

Structure:

Let the underlying price at expiry be ST. Choose strikes

\(K_1<K_2<K_3<K_4,\)with the trade typically centered so that the entry spot S0 (and the expected ST) lie between K2 and K3.

The Iron Condor is the simultaneous sale of:

A bull put spread: short put at K2, long put at K1;

A bear call spread: short call at K3, long call at K4.

Let the credits received be

\(c_p=\text{credit from put spread},\qquad c_c=\text{credit from call spread},\qquad C_{\text{net}} = c_p+c_c.\)Now we define wing widths

\(W_{\text{put}}=K_2-K_1,\qquad W_{\text{call}}=K_4-K_3.\)No‑arbitrage implies 0≤cp≤Wput and 0≤cc≤Wcall, hence

\(0\le C_{\text{net}}\le W_{\text{put}}+W_{\text{call}}.\)Option payoffs at expiry:

For any strike K,

\(C(S_T,K)=\max(0,S_T-K),\qquad P(S_T,K)=\max(0,K-S_T),\)and a short position is the negative of the corresponding long payoff.

The four legs therefore contribute:

\(\begin{aligned} \text{Long }K_1\text{ put: } & +\, (K_1-S_T)^+,\\ \text{Short }K_2\text{ put: } & -\, (K_2-S_T)^+,\\ \text{Short }K_3\text{ call: }& -\, (S_T-K_3)^+,\\ \text{Long }K_4\text{ call: }& +\, (S_T-K_4)^+. \end{aligned}\)Adding the entry credit Cnet gives the expiry payoff—profit, excluding financing:

\(\boxed{ \Pi(S_T)= C_{\text{net}} +(K_1-S_T)^+-(K_2-S_T)^+ -(S_T-K_3)^+ + (S_T-K_4)^+ . }\)Equivalently,

\(\Pi(S_T)= C_{\text{net}} -\big[(K_2-S_T)^+-(K_1-S_T)^+\big] -\big[(S_T-K_3)^+-(S_T-K_4)^+\big],\)i.e., minus the intrinsic of each short spread plus the credit.

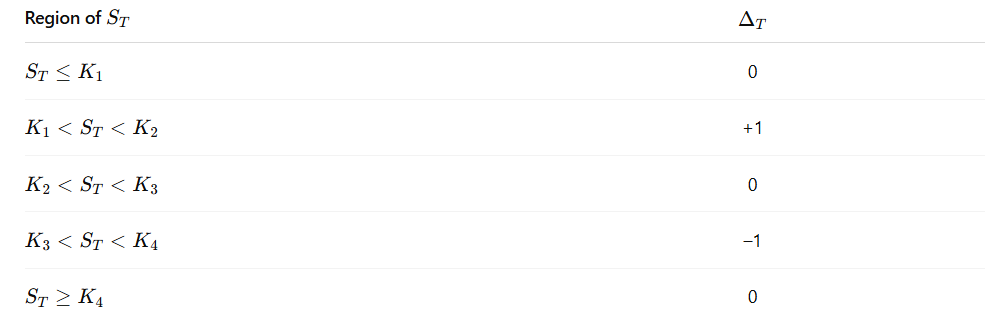

Piecewise form and interpretation of the five regions:

\(\Pi(S_T)= \begin{cases} \displaystyle C_{\text{net}}+K_1-K_2 = C_{\text{net}}-W_{\text{put}}, & S_T\le K_1 \quad \text{(max loss floor, downside)},\\[6pt] \displaystyle C_{\text{net}}-K_2+S_T, & K_1<S_T\le K_2 \quad \text{(loss zone, slope }+1),\\[6pt] \displaystyle C_{\text{net}}, & K_2<S_T<K_3 \quad \text{(max‑profit plateau)},\\[6pt] \displaystyle C_{\text{net}}+K_3-S_T, & K_3\le S_T<K_4 \quad \text{(loss zone, slope }-1),\\[6pt] \displaystyle C_{\text{net}}+K_3-K_4 = C_{\text{net}}-W_{\text{call}}, & S_T\ge K_4 \quad \text{(max loss floor, upside)}. \end{cases}\)Why these shapes?

Tails are flat when ST≤K1 (deep downside), both puts are ITM by the same amount; the ST terms cancel and you realize the put‑spread loss Wput offset by the credit. Symmetrically, for ST≥K4 the calls are both ITM and you realize Cnet−Wcall.

We have two sloped zones:

K1<ST≤K2: only the short K2 put is ITM, so each $1 rise in ST reduces that intrinsic value by $1; payoff slope +1.

K3≤ST<K4: only the short K3 call is ITM; each $1 rise in ST increases loss by $1; slope −1.

The center remains flat if K2<ST<K3: all options OTM; payoff equals the entry credit.

At expiry the position delta (slope of Π) is 0, +1, 0, −1, across the five regions; gamma is zero except at the kinks K1, K2, K3, K4.

How do we calculate the extremes?

The extremes are immediate. The maximum payoff occurs on the plateau:

\(\boxed{\Pi_{\max}=C_{\text{net}}} \quad \text{for } K_2<S_T<K_3.\)The minimum payoff is the lower of the two floors:

\(\boxed{\Pi_{\min}=C_{\text{net}}-\max\!\big(W_{\text{put}},W_{\text{call}}\big)}.\)So the maximum loss in cash is:

\(\boxed{L_{\max}=\max\!\big(W_{\text{put}},W_{\text{call}}\big)-C_{\text{net}}.}\)Per side, the losses are:

\(L_{\text{down}}=W_{\text{put}}-c_p,\qquad L_{\text{up}} =W_{\text{call}}-c_c,\qquad L_{\max}=\max(L_{\text{down}},L_{\text{up}}).\)Symmetric wings are created by Wput=Wcall=W:

\(\Pi_{\min}=C_{\text{net}}-W,\qquad L_{\max}=W-C_{\text{net}}.\)

How do we calclulate the break-even levels?

Set Π(ST)=0 on the sloped segments:

\(\begin{aligned} 0 &= C_{\text{net}}-K_2+S_T &&\Rightarrow& \boxed{S_T^{\text{BE-}}=K_2-C_{\text{net}}}\in[K_1,K_2],\\[4pt] 0 &= C_{\text{net}}+K_3-S_T &&\Rightarrow& \boxed{S_T^{\text{BE+}}=K_3+C_{\text{net}}}\in[K_3,K_4]. \end{aligned}\)A larger Cnet widens the break‑even interval and raises both floors, but given cp≤Wput and cc≤Wcall, the loss on each side remains non‑negative.

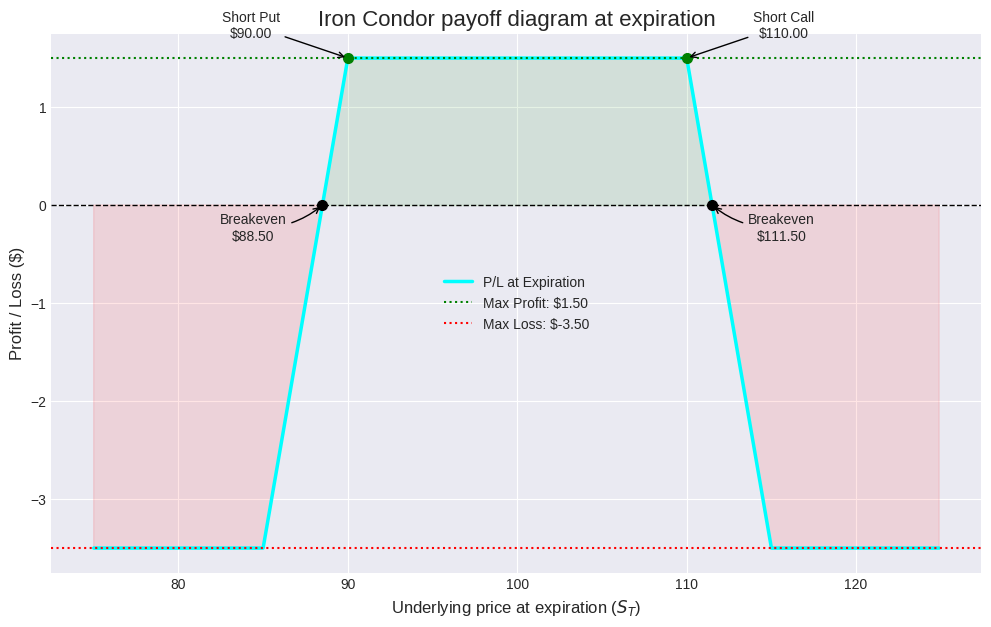

It is more simple than the math explained before. Let's visualize this step by step. The first code snippet defines a function to calculate the Iron Condor payoff.

import numpy as np

import matplotlib.pyplot as plt

def iron_condor_payoff(s_t, k1, k2, k3, k4, c_net):

"""

Calculates the P/L of an Iron Condor at expiration.

Args:

s_t (np.array): Array of underlying prices at expiration.

k1 (float): Long put strike.

k2 (float): Short put strike.

k3 (float): Short call strike.

k4 (float): Long call strike.

c_net (float): Net credit received for the position.

Returns:

np.array: P/L for each underlying price.

"""

long_put_payoff = np.maximum(0, k1 - s_t)

short_put_payoff = -np.maximum(0, k2 - s_t)

short_call_payoff = -np.maximum(0, s_t - k3)

long_call_payoff = np.maximum(0, s_t - k4)

total_payoff = c_net + long_put_payoff + short_put_payoff + short_call_payoff + long_call_payoff

return total_payoff

# Strategy Parameters

# Let's assume the underlying is trading at $100.

K1_put_long = 85.0

K2_put_short = 90.0

K3_call_short = 110.0

K4_call_long = 115.0

Net_Credit = 1.50 # Example credit received in $

# Plotting

S_T = np.arange(75, 125, 0.1) # Range of underlying prices at expiration

payoff = iron_condor_payoff(S_T, K1_put_long, K2_put_short, K3_call_short, K4_call_long, Net_Credit)

# Calculate key points

max_profit = Net_Credit

max_loss = Net_Credit - (K2_put_short - K1_put_long)

breakeven_down = K2_put_short - Net_Credit

breakeven_up = K3_call_short + Net_Credit

This plot is the classic, static representation. It is essential, but it tells us nothing about the expiration. The next part will explore the dynamics of the position before this final payoff is realized.

The Greeks

The payoff diagram is a static snapshot at a single point in time: expiration. To manage the strategy effectively, a quant must understand the position's real-time risk profile. This is where the Greeks come in. They are the partial derivatives of the option's price with respect to various market variables.

The aggregate Greeks of the four legs define its behavior. Where the price is simply the sum of the prices of its components: Vcondor=P(K1)−P(K2)−C(K3)+C(K4)

Where P(K) and C(K) are the Black-Scholes prices for put and call options with strike K. The Greeks of the Condor are therefore the sum of the Greeks of the individual options.

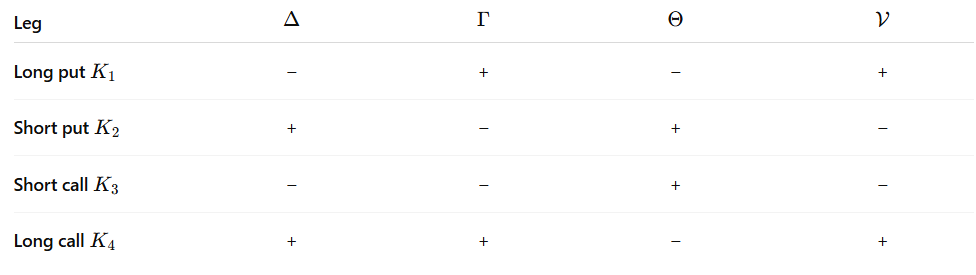

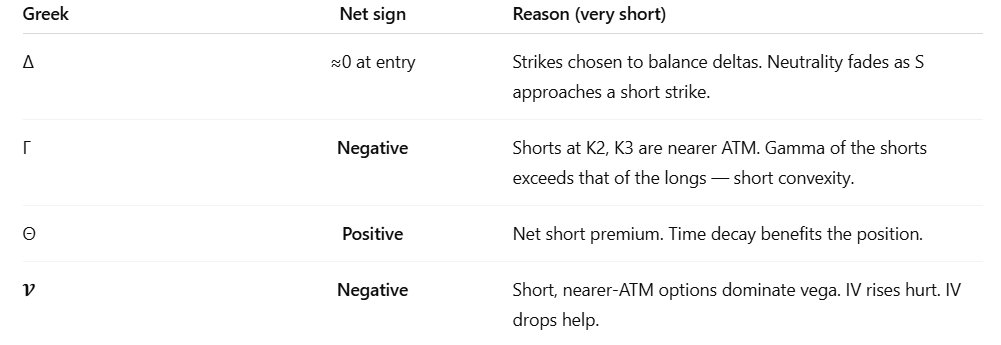

We now examine the key Greeks for this strategy:

Delta → Δ=∂V/∂S:

Delta measures the rate of change of the option's price with respect to a $1 change in the underlying asset's price.

Long put (K1): Negative Delta.

Short put (K2): Positive Delta.

Short call (K3): Negative Delta.

Long call (K4): Positive Delta.

When a Condor is initiated at-the-money, the strikes are chosen to balance these positive and negative deltas, creating a delta-neutral position. This means, for small movements in the underlying, the position's value shouldn't change much. However, as the price moves towards one of the short strikes, this neutrality is lost.

Gamma → Γ=∂2V/∂S2:

Gamma measures the rate of change of Delta. It's the convexity of the position.

Long options (puts or calls): Positive Gamma.

Short options (puts or calls): Negative Gamma.

The Iron Condor is a net short option position (2 short, 2 long, but the shorts are closer to the money and have higher gamma). This results in net negative Gamma. This is the single most important risk factor. Negative gamma means that as the underlying moves against you, your Delta becomes more adverse. If the price rises, your Delta becomes more negative. If the price falls, your Delta becomes more positive. You are short convexity, and losses accelerate.

Theta → Θ=-∂V/∂t:

Theta measures the rate of change of the option's price with respect to the passage of time (time decay).

Long options: Negative Theta (they lose value as time passes).

Short options: Positive Theta (they gain value as time passes).

The Iron Condor is a net short premium strategy, resulting in net positive Theta. This is the profit engine of the strategy. Every day that passes, assuming the underlying price and volatility remain constant, the position should make money from time decay. The core trade-off of the Iron Condor is this: You accept negative Gamma risk in exchange for positive Theta profit.

Vega → V=∂V/∂σ:

Vega measures sensitivity to a 1% change in implied volatility (sigma).

Long Options: Positive Vega.

Short Options: Negative Vega.

Since the short options (K2, K3) are closer to the money, they have higher Vega than the far out-of-the-money long options (K1, K4). This results in net negative Vega. A rise in implied volatility will hurt the position, while a fall in implied volatility will help it. This is why Iron Condors are often initiated in high implied volatility environments, with the expectation that IV will revert to its mean.

We can summarize this information in the next tables:

Much better. Okay! For this example we will use a library like py_vollib to calculate the Black-Scholes price and Greeks for each leg and then aggregate them.

#!pip install py_vollib

import py_vollib.black_scholes.greeks.analytical as greeks

from py_vollib.black_scholes import black_scholes as bs

def calculate_condor_greeks(s, k1, k2, k3, k4, t, r, sigma):

"""

Calculates the aggregated Greeks for an Iron Condor.

Args:

s (float): Current underlying price.

k1, k2, k3, k4 (float): Strike prices.

t (float): Time to expiration in years.

r (float): Risk-free interest rate.

sigma (float): Implied volatility.

Returns:

dict: A dictionary containing the position's delta, gamma, theta, and vega.

"""

# Calculate greeks for each leg

delta1 = greeks.delta('p', s, k1, t, r, sigma)

delta2 = -greeks.delta('p', s, k2, t, r, sigma)

delta3 = -greeks.delta('c', s, k3, t, r, sigma)

delta4 = greeks.delta('c', s, k4, t, r, sigma)

gamma1 = greeks.gamma('p', s, k1, t, r, sigma)

gamma2 = -greeks.gamma('p', s, k2, t, r, sigma)

gamma3 = -greeks.gamma('c', s, k3, t, r, sigma)

gamma4 = greeks.gamma('c', s, k4, t, r, sigma)

theta1 = greeks.theta('p', s, k1, t, r, sigma) / 365.25

theta2 = -greeks.theta('p', s, k2, t, r, sigma) / 365.25

theta3 = -greeks.theta('c', s, k3, t, r, sigma) / 365.25

theta4 = greeks.theta('c', s, k4, t, r, sigma) / 365.25

vega1 = greeks.vega('p', s, k1, t, r, sigma) / 100

vega2 = -greeks.vega('p', s, k2, t, r, sigma) / 100

vega3 = -greeks.vega('c', s, k3, t, r, sigma) / 100

vega4 = greeks.vega('c', s, k4, t, r, sigma) / 100

# Aggregate greeks

total_delta = delta1 + delta2 + delta3 + delta4

total_gamma = gamma1 + gamma2 + gamma3 + gamma4

total_theta = theta1 + theta2 + theta3 + theta4

total_vega = vega1 + vega2 + vega3 + vega4

return {'delta': total_delta, 'gamma': total_gamma, 'theta': total_theta, 'vega': total_vega}

# Parameters for Greek Calculation

S_range = np.arange(80, 121, 1) # Price range to analyze

T = 45.0 / 365.25 # 45 days to expiration

R = 0.05 # 5% risk-free rate

SIGMA = 0.20 # 20% implied volatility

# Use the same strikes as before

K1, K2, K3, K4 = 85, 90, 110, 115

# Calculate greeks across the price range

condor_greeks_list = [calculate_condor_greeks(s, K1, K2, K3, K4, T, R, SIGMA) for s in S_range]

# Extract individual greeks for plotting

deltas = [g['delta'] for g in condor_greeks_list]

gammas = [g['gamma'] for g in condor_greeks_list]

thetas = [g['theta'] for g in condor_greeks_list]

vegas = [g['vega'] for g in condor_greeks_list]

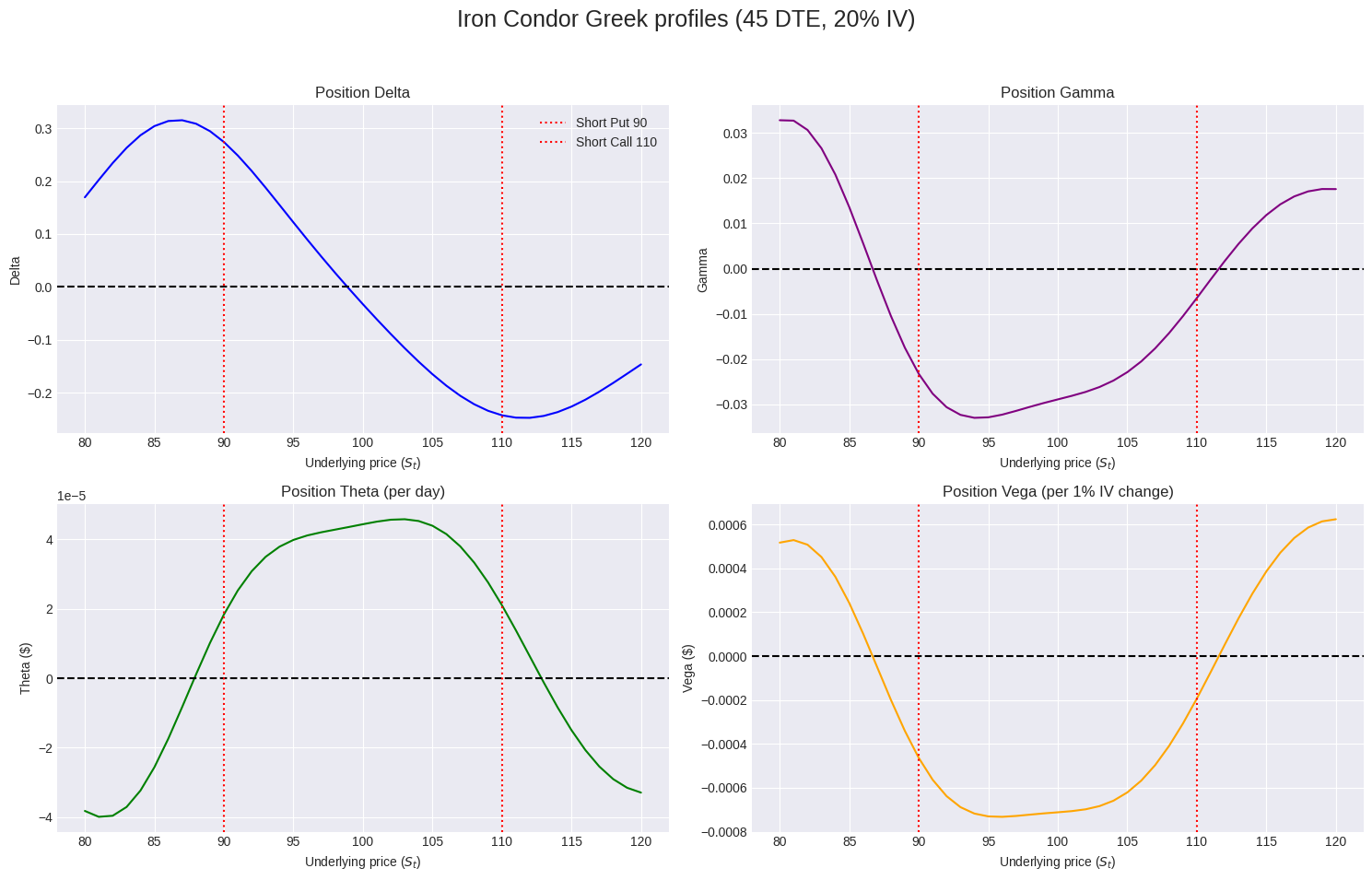

The plots reveal the dynamic nature of the risk.

Delta is near zero between the short strikes but quickly becomes positive below K2 and negative above K3. This is the directional risk.

Gamma is negative across the board, but most strongly negative near the short strikes. This is the acceleration risk.

Theta is positive, peaking between the strikes. This is the income.

Vega is negative, also most strongly near the strikes. This is the volatility risk.

An algorithmic system must monitor these Greeks in real-time. A rule might be: If absolute position Delta exceeds 0.10, trigger an adjustment, or If the underlying price moves to a point where Gamma is below -0.05, raise an alert.

Beyond the payoff diagram

The most common mistake traders make with Iron Condors is conflating a high POP with a positive Expected Value. You might advertise a trade with a 90% chance of success, which sounds fantastic. However, if the 10% of losing trades lose, on average, more than 9 times the amount gained from the winners, the strategy has a negative EV and is a long-term loser.

For an Iron Condor, the Avg. Win is capped at the net credit received. The Avg. Loss can be significantly larger. A quantitative approach demands that we move beyond the simple POP and analyze the full probability distribution of outcomes.

To calculate these probabilities, we need a model for the future distribution of the underlying asset's price. The standard model in finance is that asset prices follow a Geometric Brownian Motion, which means that log-returns are normally distributed. Consequently, the price at expiration, ST, follows a log-normal distribution.

The parameters for this distribution are:

Current Price: ST.

Time to Expiration: T.

Drift: mu (often assumed to be the risk-free rate, r, in the risk-neutral world).

Volatility: sigma (the implied volatility derived from option prices).

The expected price at expiration is E[ST]=STemu·T. The standard deviation of the log price is σ√T

The POP is the probability that the underlying price S_T will finish between the breakeven points at expiration.

Breakeven down: KBE, down=K2 −Cnet

Breakeven up: KBE, up=K3+Cnet

So, we need to calculate P(KBE,down < ST< KBE,up). Using the log-normal assumption, this can be calculated from the cumulative distribution function (CDF) of the normal distribution.

Let

We assume

Then the probability of profit is modeled by:

Let's write Python code to calculate the POP and, more importantly, to visualize the entire P/L distribution. This gives a much richer view of the risk-reward tradeoff than a single EV number.

import scipy.stats as stats

def analyze_condor_probabilities(s_t, k1, k2, k3, k4, c_net, t, r, sigma):

"""

Analyzes the probabilistic outcomes of an Iron Condor.

Returns:

dict: Containing POP, EV, and data for plotting.

"""

# Breakeven points

breakeven_down = k2 - c_net

breakeven_up = k3 + c_net

# Lognormal distribution parameters for S_T

mu = (r - 0.5 * sigma**2) * t

std_dev = sigma * np.sqrt(t)

# Calculate Probability of Profit (POP)

z_down = (np.log(breakeven_down / s_t) - mu) / std_dev

z_up = (np.log(breakeven_up / s_t) - mu) / std_dev

pop = stats.norm.cdf(z_up) - stats.norm.cdf(z_down)

# Simulate a large number of outcomes for EV and plotting

num_simulations = 250000

# S_T = s_t * np.exp(mu + std_dev * np.random.randn(num_simulations)) # Lognormal sample

# Using stats.lognorm.rvs for clarity

lognorm_dist = stats.lognorm(s=std_dev, scale=np.exp(mu) * s_t)

simulated_s_t = lognorm_dist.rvs(size=num_simulations)

# Calculate P/L for each simulated outcome

simulated_pl = iron_condor_payoff(simulated_s_t, k1, k2, k3, k4, c_net)

expected_value = np.mean(simulated_pl)

return {

'pop': pop,

'expected_value': expected_value,

'simulated_s_t': simulated_s_t,

'simulated_pl': simulated_pl,

'dist': lognorm_dist

}

# Parameters

S_t = 100.0

K1, K2, K3, K4 = 85, 90, 110, 115

C_net = 1.50

T = 45.0 / 365.25

R = 0.05

SIGMA = 0.20 # 20% IV

# Run analysis

analysis = analyze_condor_probabilities(S_t, K1, K2, K3, K4, C_net, T, R, SIGMA)

print(f"Probability of Profit (POP): {analysis['pop']:.2%}")

print(f"Expected Value (EV) from Simulation: ${analysis['expected_value']:.4f}")

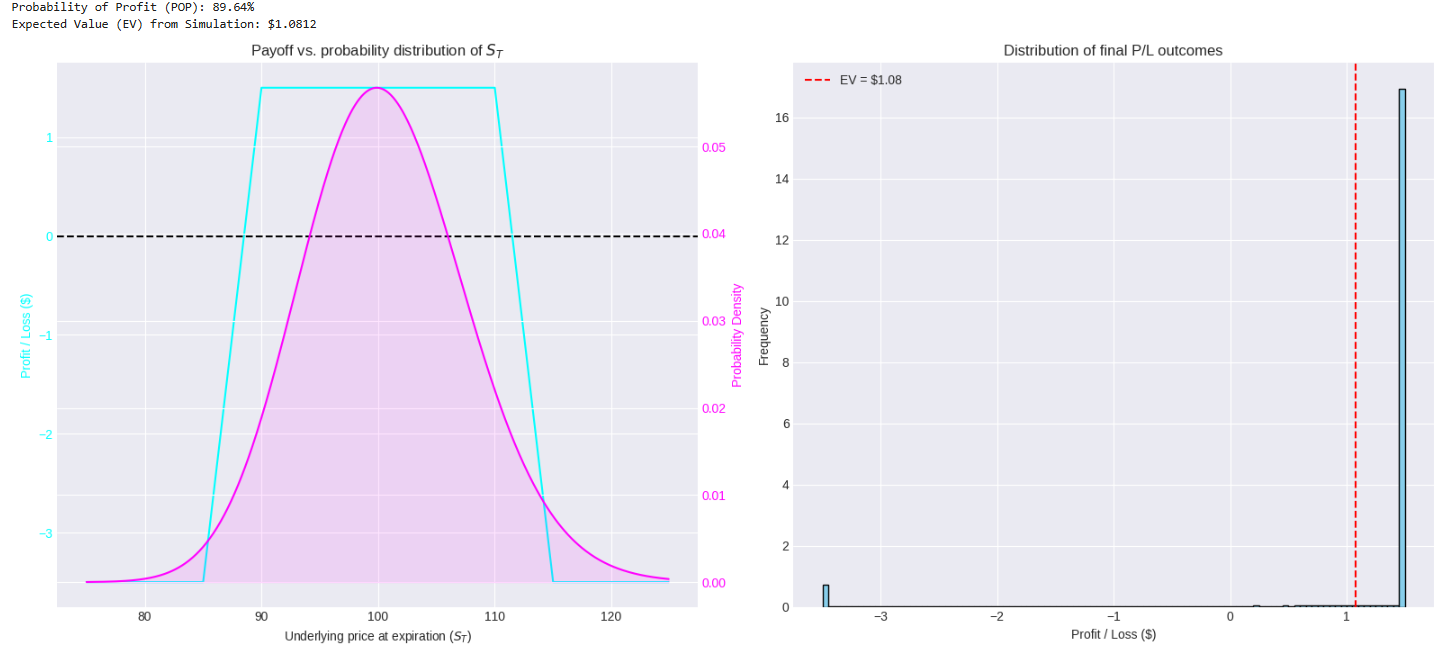

This analysis provides a much clearer picture.

The first plot shows why the POP is high: the bulk of the probability distribution for the final price lies squarely within the profitable range of the condor. However, it also shows the tails of the distribution extending into the max loss zones.

The second plot, the P/L distribution, is the most sobering. It typically shows a large spike at the max profit value and smaller, but significant, frequencies in the loss regions. The negative skew is apparent: the potential for large losses pulls the mean (the Expected Value) down. In this specific example, the EV might be positive, but a small increase in volatility or a wider spread could easily turn it negative, even with a high POP.

An algorithmic system can run this analysis before placing any trade, refusing to enter positions with a negative EV, regardless of the POP. This is a fundamental quantitative filter.