[INTEL REPORT] Systemic risk in five vectors

U.S. domestic fracture, the AI debt bubble, the dollar–yuan war, the Nigerian resource front, and Europe’s self-inflicted irrelevance.

Table of contents:

Introduction.

Risk vector 1: U.S. domestic fracture—banking stability.

Risk vector 2: The AI bubble—debt, profitability, and systemic linkage.

Risk vector 3: The global currency war—the dollar vs. the yuan.

Risk vector 4: The new scramble for Africa—Nigeria as geopolitical flashpoint.

Risk vector 5: European fragmentation and regulatory risk

View of the systemic risk for investor.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

The series of distinct political, financial, and geopolitical crises unfolding in November 2025 are not isolated events. They represent a polycrisis in which domestic, financial, technological, and geopolitical risks are deeply interconnected, creating a single, fragile, and highly leveraged global system. The perceived stability in certain asset classes, such as the low volatility in U.S. markets, is not a sign of health but a symptom of a critical information vacuum that is masking systemic risk.

The core risk loop this report identifies is a causal chain:

A U.S. domestic crisis, centered on an unprecedented 43-day government shutdown, is creating an information fog by withholding key economic data. This shutdown simultaneously threatens a potential credit event via the November 15th payment deadline, a risk explicitly highlighted by the U.S. Treasury.

This domestic instability directly threatens the Artificial Intelligence market bubble. This bubble is not, as widely believed, built on profits, but on a massive, cycle of corporate debt. This debt finances AI ventures that are currently unprofitable and requires permanent, low-cost financing from a Federal Reserve that is now data-blind.

The fragility of this domestic tech-market system compels the U.S. to pursue aggressive geopolitical wins, manifesting as a two-front global conflict with China. This conflict is being waged as both:

A currency war: Using the dollar as a coercive bailout tool to force geopolitical alignment and sever third-party ties with China, with Argentina serving as the new model of coercion.

A resource war: Using a humanitarian pretext to justify military intervention in Africa, specifically Nigeria, to secure critical hydrocarbon and mineral assets that China currently dominates.

This global confrontation is exacerbated by the strategic weakness of key allies. Europe, in particular, is proving to be a fragmented and strategically irrelevant actor. It is ceding the global digital currency race to its own banking lobby, delaying its digital euro until 2029, while simultaneously creating new systemic risks through its own flawed governance and regulatory overreach.

To know more about this polycrisis check this:

The primary takeaway for investors is that traditional risk models are failing. Market volatility is artificially suppressed by a lack of data, corporate valuations are based on circular financing structures, and geopolitical risk is now the primary driver of market access, currency stability, and resource security.

Risk vector 1: U.S. domestic fracture—banking stability

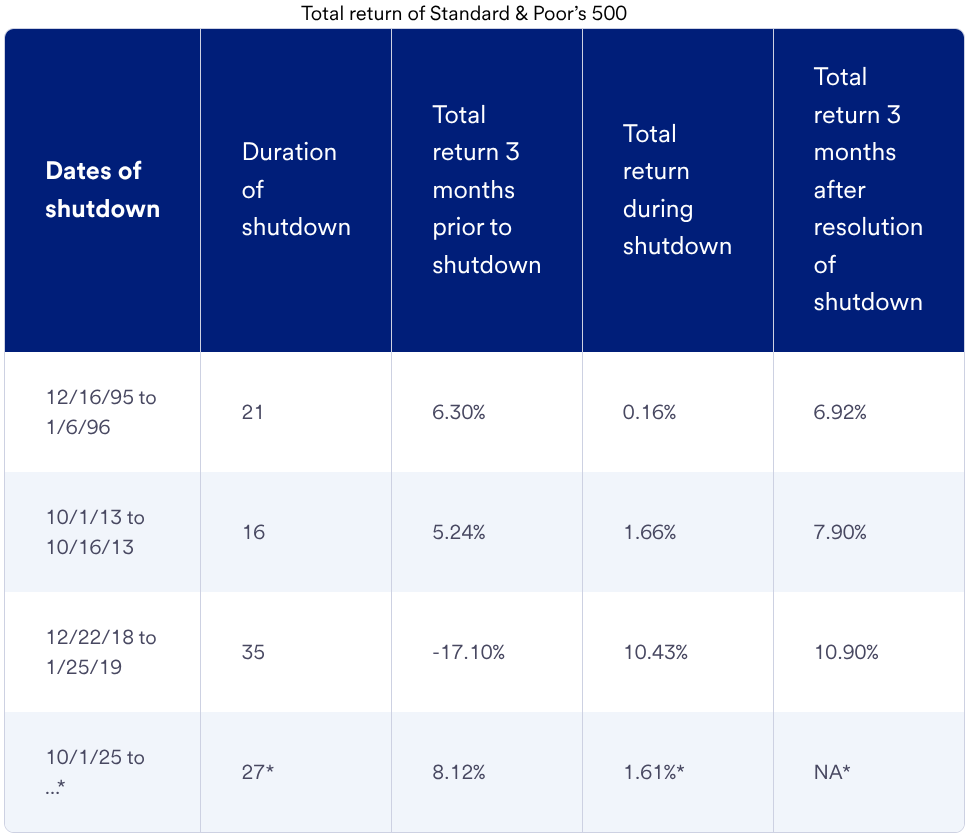

The market is dangerously mispricing the impact of the ongoing 43-day government shutdown. The consensus view treats this as political theater, with some analysts noting that past shutdowns have had limited broad economic impacts. This view is dangerously complacent.

The primary risk, which is being under-discussed in financial media, is the acute threat to banking stability. This is not about the long-term economic drag from furloughed workers, but the immediate, technical impact on financial plumbing.

The mechanism for this risk is the liquidity withdrawals resulting from the halt in federal spending. Analyst reports confirm this is creating a liquidity crisis by impacting the Treasury General Account and causing a spike in interbank lending rates. J.P. Morgan’s analysis from November 7, 2025, confirms this, noting tightening pressure on the financing markets that is expected to subside once the shutdown is alleviated. The shutdown is, in effect, a government-induced credit squeeze on the very banking system that underpins the economy.

This generalized pressure is set to become a full-blown crisis event. The source analysis identifies a specific deadline: November 15, 2025.

This date has been confirmed by Treasury Secretary Scott Bessent. He issued a public warning on CBS that payments are not guaranteed after November 15th. This transforms the shutdown from an appropriations dispute into a de facto U.S. credit default event. This looming deadline, just two days from this report, is the true X-date for this crisis, threatening immediate and severe instability in the U.S. Treasury market.

The direct economic impact of this impasse is no longer theoretical. The almost 40 million people who rely on food aid are the first victims. On November 1, 2025, the Trump administration officially paused all SNAP (Supplemental Nutrition Assistance Program) contributions. This immediate halt to a $21 billion program delivers a severe shock to the internal demand that the U.S. economy is built upon, directly impacting the low-income households who are most vulnerable.

The most sophisticated and under-appreciated risk of this shutdown is not the lack of spending, but the lack of data. The low volatility observed in financial markets is a trap; it is the calm of an information vacuum.

A November 4, 2025, letter from the Treasury Borrowing Advisory Committee (TBAC) to the Treasury Secretary explicitly states that financial markets have exhibited low volatility because key US economic data have been delayed. J.P. Morgan and U.S. Bank confirm that the Bureau of Labor Statistics has not published its monthly employment report or new inflation data.

The TBAC letter contains an explicit warning: Once the government reopens and delayed data is released, we may see investors and policymakers rapidly update their outlook for the US economy.

The shutdown is poised to end. The Senate approved a funding package late Monday, and the House is expected to vote on it as soon as Wednesday, November 12. This means the data-release shock is imminent. When the government reopens, weeks of back-dated economic reports will be released at once, forcing the Federal Reserve and all market participants to re-price assets instantly.

This, not furloughed workers, is the banking stability risk. It is a volatility event created by the sudden, chaotic return of information to a market that has been flying blind.

Risk vector 2: The AI bubble—debt, profitability, and systemic linkage

The domestic fragility detailed in Vector 1 is directly linked to the precariousness of the U.S. equity market, which is being driven to record highs by the AI bubble. This bubble is defined by an debt that is absolutely elephantine and surpasses the dot-com era.

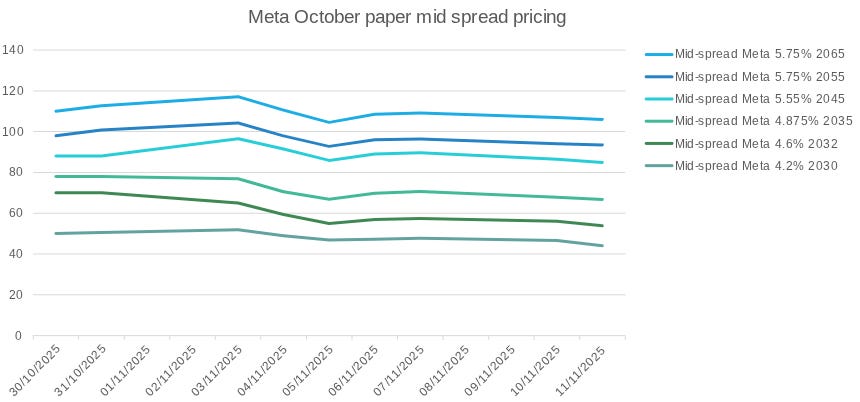

This claim is not hyperbole. It is confirmed by recent capital market activity. On October 30, 2025, Meta Platforms issued a massive $30 billion bond. This was one of the largest U.S. corporate bond offerings of the year. The stated purpose for this enormous debt issuance was explicitly to fund AI expansion and ramp up AI infrastructure.

This fact directly contradicts the dominant market narrative. Analysts at Invesco and Wells Fargo have argued that the 2025 AI boom is not a bubble precisely because its mega-cap leaders are highly profitable and are funding these projects from operating cash flow and cash reserves.

The market is conflating legacy profits with AI spending. The Invesco and Wells Fargo analyses are dangerously misleading. The core of the risk is this: AI is not profitable today.

This assessment is validated by OpenAI’s own leadership and financial disclosures. OpenAI CEO Sam Altman has warned of insane valuations and stated it could be 4 or 5 years” before the technology is profitable. A November 10, 2025, report in The Guardian detailed the “chasm-like gap between OpenAI’s $1.4 trillion... spending commitment over the next eight years and its $13 billion in annual revenues.

Meta’s $30 billion bond offering is the definitive proof. The bull case is a fallacy. The legacy businesses (Meta/Google advertising) are profitable. The AI buildout is a massive, unprofitable cash drain. Meta is funding its unprofitable AI divisions with debt, using its legacy profits as collateral. This action does not prove stability; it proves the company is becoming more leveraged and more fragile, not less.

The AI bubble is not just unprofitable; it may be an echo chamber. A Yale Insights report from October 2025 details a liquidity-go-round of circular investments that should alarm any investor.

This analysis maps the circular financing:

Nvidia is investing $100 billion in OpenAI.

OpenAI is taking a 10% equity stake in AMD.

Microsoft, already OpenAI’s major shareholder, is also a major customer of AI cloud company CoreWeave.

Nvidia holds a significant equity stake in CoreWeave.

This is not a supply chain; it is a closed loop. If Nvidia invests $100 billion in OpenAI, and OpenAI uses those funds to buy $100 billion of Nvidia’s chips (to meet its $1.4 trillion commitment), Nvidia’s revenue is inflated by $100 billion. This revenue justifies its stock price, which in turn props up the entire S&P 500, where the tech sector now represents an all-time high of 35%. This is financial engineering, not sustainable economic growth.

This brings us to the critical link between Vector 1 and Vector 2. An unprofitable, debt-fueled, circularly-financed bubble requires one thing to survive: that the Fed lowers interest rates.

The AI bubble (Vector 2) is entirely dependent on the Federal Reserve to keep the cost of its debt at or near zero. This makes the entire U.S. equity market a hostage to accommodative monetary policy.

This creates the critical tension for November 2025:

The Fed must stay accommodative to save the AI bubble.

The Fed is losing the data it needs (Vector 1) to justify doing so.

The end of the shutdown and the subsequent “data-release shock” could reveal inflation or employment numbers that prevent the Fed from cutting rates, thereby pulling the one pin holding the entire AI bubble structure together.

Check more about the AI bubble here:

![[Intel Report] The AI debt cycle](https://substackcdn.com/image/fetch/$s_!AJt2!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F5cedd76e-1949-481c-a904-be1a249336c5_1280x1280.png)