Table of contents:

Introduction.

Market sentiment.

The “AI Debt Bubble”.

Is it a bubble? (Morgan Stanley vs. Goldman Sachs).

Case study: Oracle.

How China complicates the AI bet.

The political and geopolitical risk.

Re-evaluating the portfolio.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

The era of growth at any cost funded by zero-interest rates is definitively over. It has been replaced by a new, more dangerous investment at any cost era, specifically in Artificial Intelligence. This new paradigm is funded by a massive, accelerating cycle of corporate debt. In 2025 alone, companies within Goldman Sachs’s AI equity basket have issued $141 billion in debt, surpassing the total for all of 2024. Total AI-related debt issuance this year has surged past $200 billion, accounting for over a quarter of the entire net supply of U.S. corporate debt. Tech giants are even turning to off-balance-sheet Special Purpose Vehicles to finance this spending, raising concerns about transparency and hidden leverage.

This dynamic has created a structurally unsound barbell market, defined by extreme leverage risk in the tech sector—the AI Debt Bubble—on one side, and non-correlated macro opportunities on the other. The central thesis of this report is that the market is bifurcating into two distinct economies:

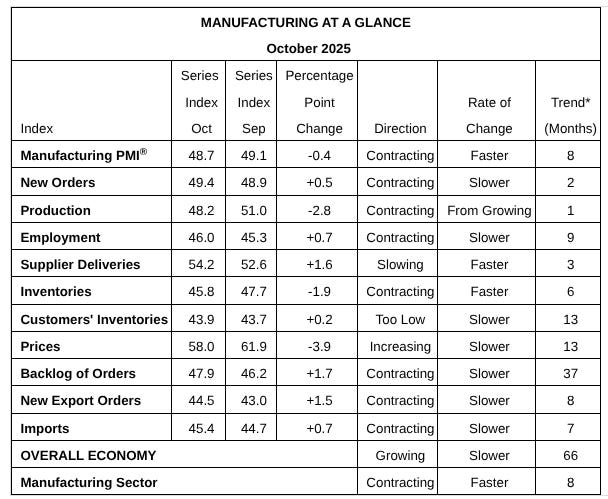

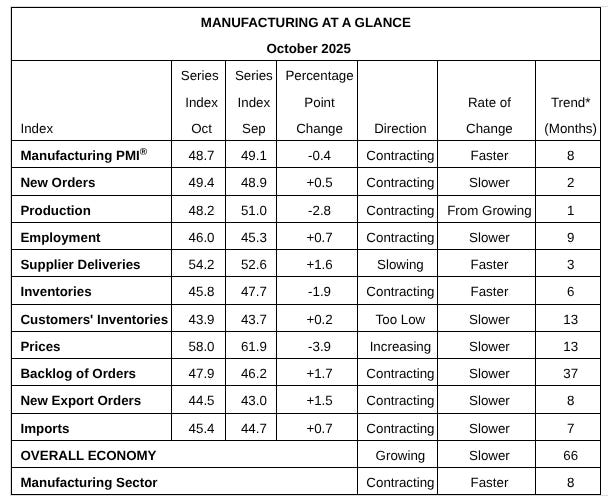

The real economy: This sector is sunk and contracting. The October ISM Manufacturing PMI, released Monday, registered at 48.7, marking the eighth consecutive month of contraction. Internal comments from the report confirm this weakness is linked to political risk, with “nearly every comment... lamenting tariffs”.

The AI economy: This sector is booming, but financing its existence with unsustainable levels of debt. This disconnect is stark: AI-related firms have accounted for 80% of U.S. stock gains and AI-equipment investment drove 92% of GDP growth in the first half of 2025.

This AI Debt Bubble is precarious. While valuations have soared—with Nvidia becoming the first $5 trillion company and Microsoft and Apple hitting $4 trillion —the foundation is questionable. While Goldman Sachs analysts argue we are not in a bubble... yet, others are sounding the alarm. Morgan Stanley’s investment committee believes the market is closer to the seventh inning than the first or second. The core risk is the funding source and the return on investment. Of the $3 trillion in datacenter spending projected by 2028, an estimated $1.5 trillion must be financed from sources outside Big Tech’s cash flow, namely private credit —a structural risk to the overall global economy. This debt is being raised for speculative assets, a thesis supported by a recent MIT study showing that 95% of organizations are getting zero return on their generative AI pilot investments.

Check this MIT study here:

Investors must immediately re-allocate portfolios to reflect this new reality. The strategy of buying broad, market-cap-weighted tech indices is now unacceptably risky. The AI arms race, described as a sperm race where only one winner will emerge, is a capital-expenditure contest where winning is secondary to survival. Meta, Microsoft, and Alphabet have all recently hiked their 2025 capex forecasts, and Microsoft has warned that its 2026 spending will rise at an even faster pace. This mandatory spending validates the arms dealer thesis. The optimal strategy is to SELL the over-leveraged, low-cash-flow AI contenders and BUY the AI arms dealers (e.g., semiconductors) and AI infrastructure (e.g., energy, utilities) that profit regardless of which contender wins the race.

Simultaneously, political risk is no longer a tail risk; it is an immediate, binary event. Today, November 4, is the New York City mayoral election, where President Trump has explicitly threatened to withhold federal funds if Zohran Mamdani wins, stating he won’t send good money after bad. Tomorrow, November 5, the Supreme Court will hear oral arguments in Learning Resources v. Trump to decide if the president’s unilateral use of the IEEPA for tariffs is constitutional. A ruling against the administration would blow a $1.8 trillion hole in projected tax revenue. This environment demands a barbell strategy and a significant allocation to non-correlated assets of fear. This thesis has been mainstreamed by BlackRock CEO Larry Fink, who recently stated that investors own Gold and Bitcoin when they are frightened of the debasement of your assets.

Market sentiment

The market’s sharp negative open on November 3, 2025, is the catalyst for this analysis. It reveals a crisis of confidence driven by a widening divergence between a contracting real economy and a debt-fueled AI economy.

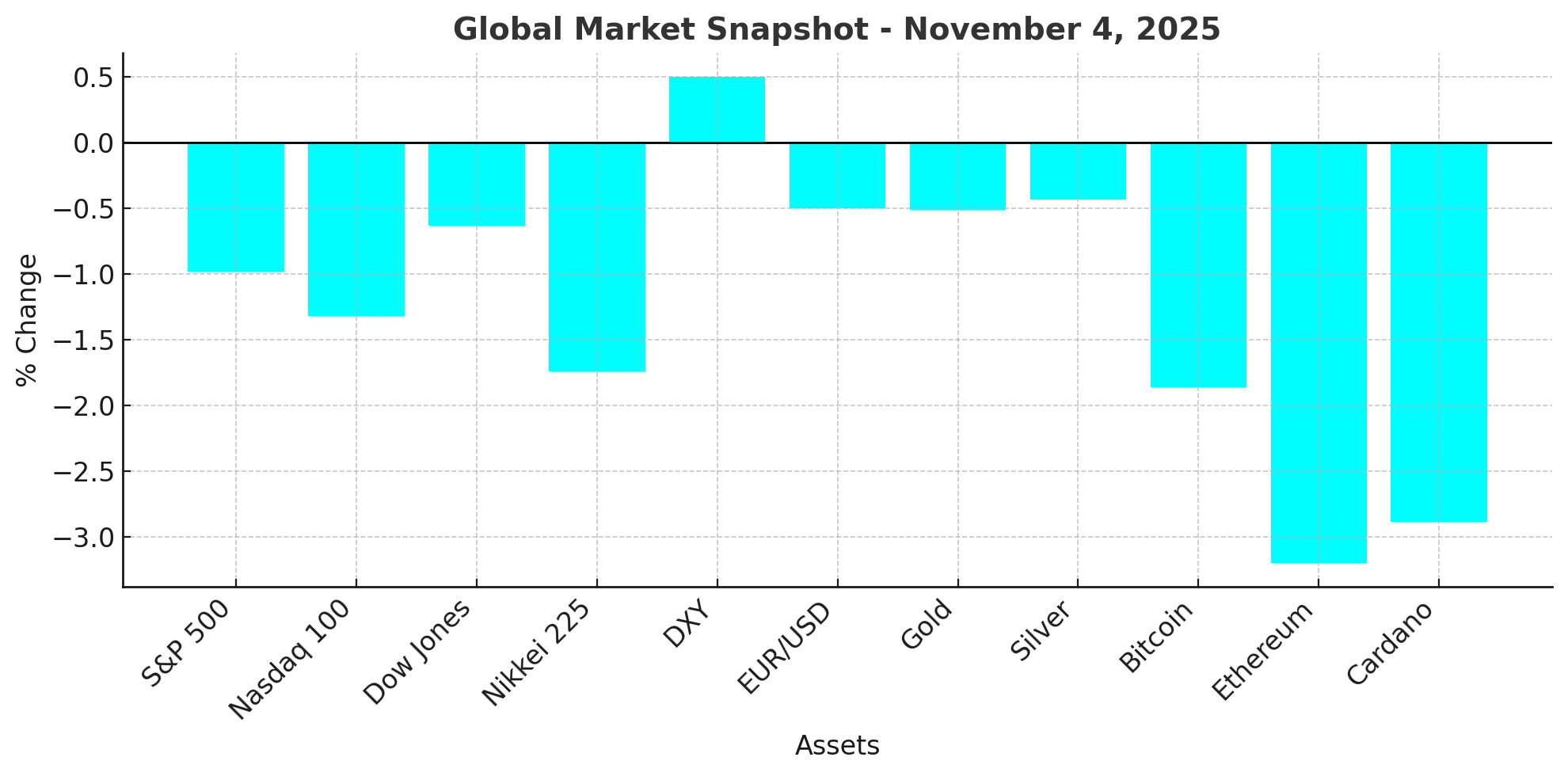

Global markets are experiencing a significant risk-off event. The Nasdaq 100 is down 1.32%, the S&P 500 has fallen 0.98%, and the Dow Jones is 0.63% in the negative. This sell-off is global, with Asian markets showing heavy losses, including Japan’s Nikkei falling 1.74%.

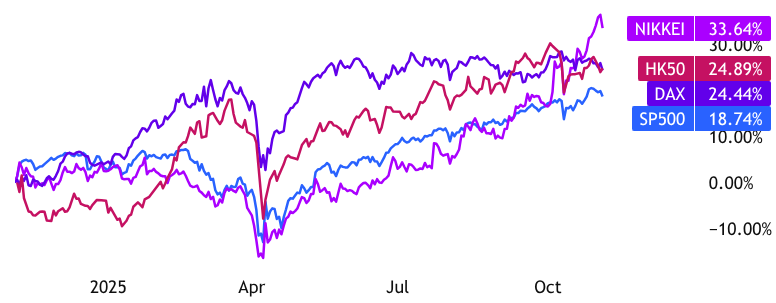

This pullback is not a random event; it is a profit-taking wave following a period of record-breaking euphoria. The S&P 500 reached an all-time high of 6921.75 in October 2025 , as did Japan’s Nikkei 225, which hit 52,659 in November. In fact, the Nikkei just posted its largest-ever monthly point rise in October.

A market that has just experienced a record-breaking rally should be resilient. Its inability to absorb negative news—specifically, weak US manufacturing data and the paradoxical reaction to Palantir’s earnings—indicates that investor conviction is shallow. The jump in Wall Street’s “fear gauge,” the VIX index, confirms this “risk-off” panic is underway.

Here a global market snapshot (November 4, 2025):

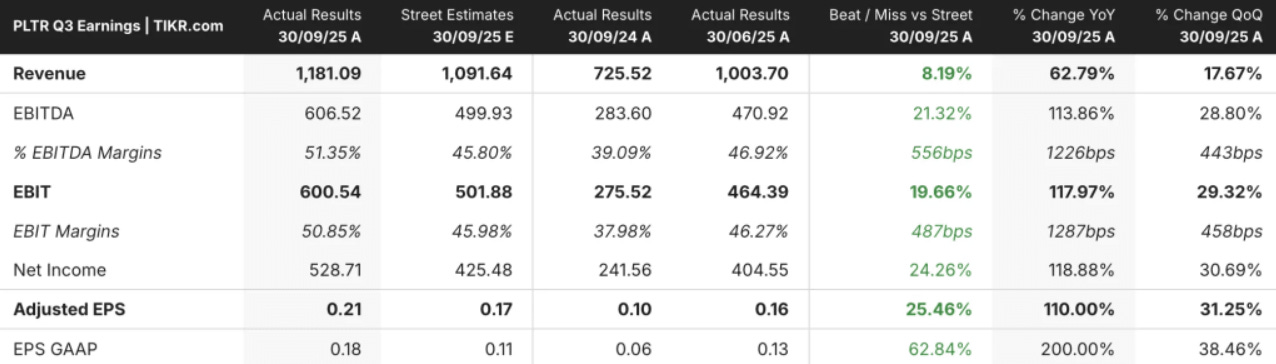

A primary driver of market doubt is the reaction to Palantir’s results. This presents a critical paradox. Palantir’s Q3 2025 earnings, released November 3, were not just a beat; they were a crush.

The beat: Q3 revenue jumped 63% year-over-year (vs. 50% expected), and adjusted EPS surged 110% (vs. 70% expected).

The growth: U.S. Commercial revenue exploded by 121%.

The guidance: Management significantly raised its full-year 2025 revenue guidance.

Despite this blowout report, the stock is down over 4% in pre-market trading. This is a sell the news event and a classic canary in the coal mine for valuation risk. The market is not selling Palantir’s business, which is booming; it is selling its valuation. Analysts note the stock’s valuation was disconnected from fundamentals and traded at an extreme multiple. One report identifies Palantir as a stock to sell when the hype fades due to its excessive stock gains.

This reaction signals a market top for high-growth, high-multiple AI names. When a company delivers perfect, accelerating results and the stock still falls, it means that market expectations have reached a level of perfection that is mathematically impossible to sustain.

The market’s anxiety is rooted in a fundamental disconnect between the booming AI economy and the sunk real economy.

The real economy: The US manufacturing sector has contracted for the eighth consecutive month. The October ISM Manufacturing PMI was 48.7 , missing consensus forecasts of 49.5 and remaining firmly in contraction territory (any reading below 50). The internal components of the report are even weaker: Manufacturing Employment is a dismal 46.0, and New Orders are at 49.4. This signals weak internal demand, a problem exacerbated by inflation.

ISM ® Manufacturing PMI ® Report data The AI economy: This sunk reality is completely divorced from the AI narrative. In 2025, AI-related companies have accounted for 80% of all gains in U.S. stocks. Investment in computer equipment alone accounted for an astonishing 92% of GDP growth in the first half of 2025. Companies are investing $400 billion in AI this year alone.

This divergence is the central, unsustainable macro risk. The AI economy is spending $400 billion on the assumption that a healthy real economy will eventually buy its services. The ISM data proves this assumption is currently false. A hidden link connects these two worlds: within the negative ISM report, nearly every comment was lamenting tariffs. This links the real economy’s weakness directly to the black swan political risk of the Supreme Court tariff case.