Table of contents:

Introduction.

Dilution analysis.

Income.

Balance.

Cash flow.

Ratios.

Segment.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

We are opening a new subsection inside MarketOps dedicated to small-cap opportunities. The goal of this series is to analyze companies that may be overlooked by the broader market but still present interesting financial, operational, or strategic characteristics for investors. This first report marks the beginning of that new series!!!

Rush Street Interactive, Inc. (ticker: RSI) is an online gambling and sports betting company operating within the Consumer Cyclical sector, specifically in the Gambling industry. RSI should be analyzed as a digital gaming operator whose value depends on its ability to grow revenue, retain users, improve margins, and manage dilution in a highly competitive and regulated market.

The company’s business is centered on online casino gaming, sports betting, and related digital wagering products. Unlike traditional casino operators, RSI does not depend primarily on physical casino properties, hotel capacity, or destination traffic. Its business model is more closely tied to digital platform performance, market access, customer acquisition, regulatory approvals, payment infrastructure, product experience, and player retention. This gives RSI a different investment profile from land-based gambling businesses.

The main attraction of RSI is its exposure to the continued legalization and expansion of online gambling. As more jurisdictions allow regulated online betting and iGaming, companies with existing platforms, licenses, and operating experience can expand their addressable market. Growth in this industry requires significant spending on marketing, promotions, compliance, technology, and customer support.

RSI’s investment case depends on four main areas:

Revenue quality.

Margin expansion.

Balance sheet strength

Dilution control.

Strong revenue growth is valuable only if it leads to better operating leverage and cash generation. Improving EBITDA is useful, but investors should also examine net income, operating cash flow, free cash flow, and the difference between adjusted and reported profitability.

Overall, RSI can be introduced as a small-cap digital gambling company with exposure to a structurally growing industry, but also with meaningful execution and capital structure risks. The company operates in an attractive market, but its investment value depends on whether management can convert market growth into sustainable profitability and improved per-share value. For that reason, RSI deserves a detailed analysis across dilution, income statement quality, balance sheet position, cash flow generation, operating ratios, and segment performance.

All information and data presented in this article have been sourced from the QuantX platform.

Dilution analysis

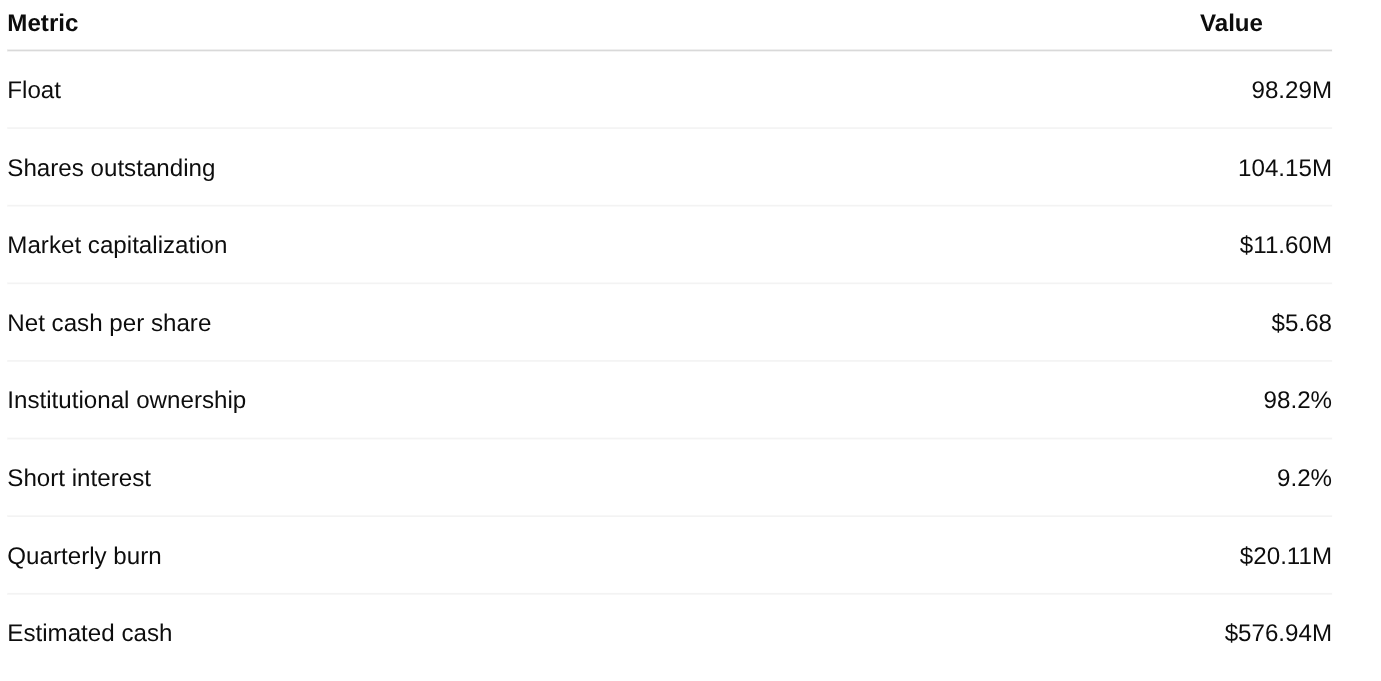

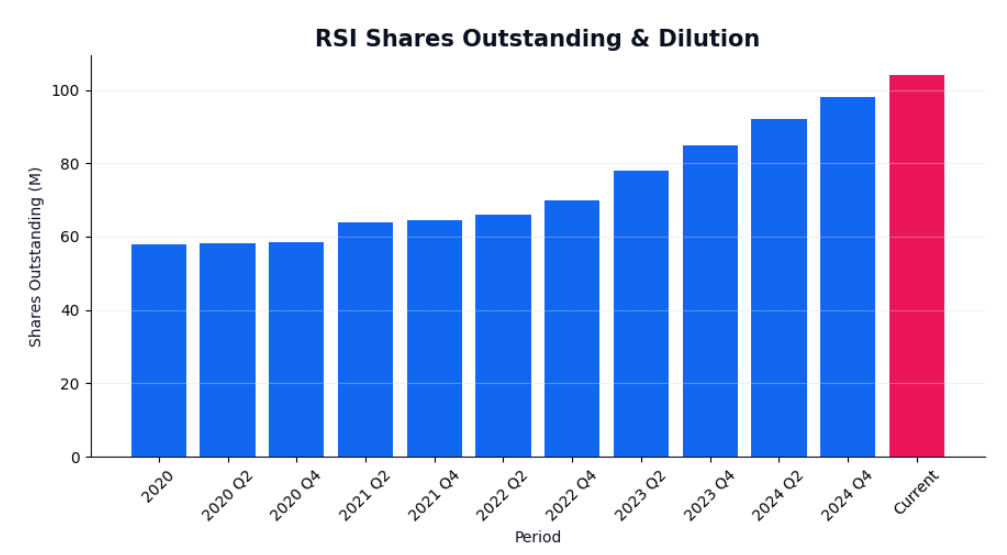

Rush Street Interactive’s dilution profile is a relevant part of the equity analysis because the company has a meaningful public share base and a visible increase in shares outstanding over time. The dilution panel shows 104.15 million shares outstanding and a float of 98.29 million shares, which means that most of the company’s share base is already available for public trading.

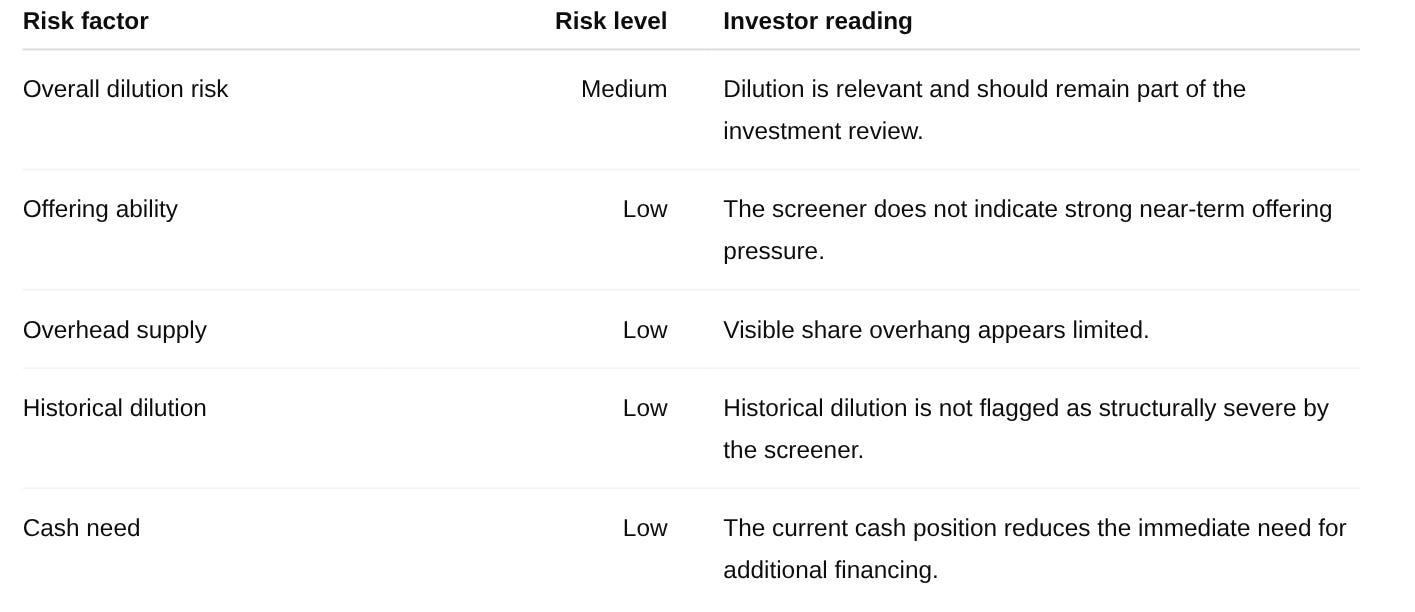

The first important observation is that RSI is classified with medium overall dilution risk. The share-count chart shows a clear upward trend from roughly 58 million shares in 2020 to 104.15 million shares currently. That increase is material from a shareholder perspective because the ownership base has expanded over the period shown.

The chart shows that RSI’s share count increases in a gradual way. A company can increase revenue, improve its operating footprint, and expand into new markets, but if the share count also rises materially, the economic benefit must be measured on a per-share basis.

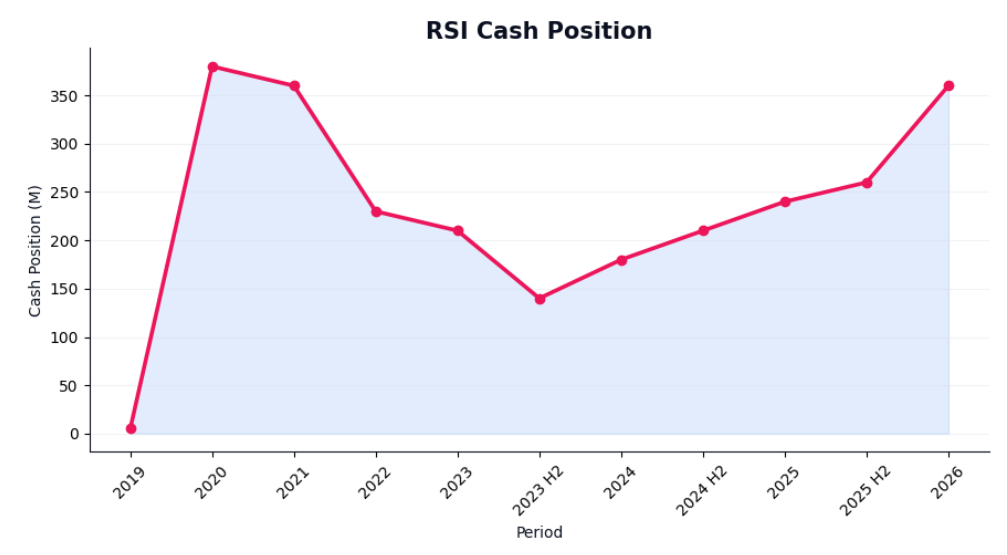

At the same time, the dilution risk is partly offset by the company’s cash position. RSI’s data shows net cash per share of $5.68, estimated cash of $576.94 million, and quarterly burn of $20.11 million. These figures confirm that RSI is not under immediate financing pressure. The cash need indicator is marked as low, which is consistent with the idea that the company has enough liquidity to reduce the near-term probability of raising capital through additional equity issuance.

The cash position chart shows a sharp increase around 2020, followed by a multi-year decline and then a recovery into the most recent period. This pattern shows that RSI’s balance sheet has experienced both cash drawdown and cash rebuilding. The decline from the earlier peak indicates that cash has been consumed or redeployed over time, while the recent recovery suggests improved liquidity.

The quarterly burn of $20.11 million is also important. Even with a large estimated cash balance, burn rate must be monitored because persistent cash consumption can gradually change the dilution profile. At the current level shown, the company appears to have enough liquidity to absorb ongoing burn. If burn decreases as revenue scales and margins improve, dilution risk declines further. If burn remains persistent or increases, the company’s future need for capital becomes more relevant.

Offering ability is marked low, which indicates that the screener does not currently identify strong near-term offering pressure. Overhead supply is also marked low, suggesting that visible selling pressure from prior issuance or overhang is not considered severe by the screener. Historical dilution is marked low, although this should be interpreted carefully because the chart still shows a meaningful increase in shares outstanding over time.

The institutional ownership figure is also notable. Data shows 98.2% institutional ownership, which implies that RSI’s shareholder base is concentrated among institutions. This can be interpreted in two ways. On one hand, high institutional ownership can indicate that professional investors are involved in the stock. On the other hand, it can also make the stock more sensitive to institutional portfolio adjustments, block sales, or changes in sentiment. When institutional ownership is this high, investors should monitor ownership changes, insider activity, secondary offerings, and large holder transactions.

Short interest is shown at 9.2%. A short interest level of this size can indicate skepticism or hedging activity, but dilution risk depends more directly on the company’s share issuance behavior, cash burn, capital needs, and financing structure. For RSI, the short interest figure should be viewed as a secondary market signal rather than the main determinant of shareholder risk.

Overall, RSI’s dilution profile is mixed but positive. The company has a rising share count, which creates a real per-share issue. However, the current risk indicators are mostly low, and the cash position reduces immediate financing pressure.

RSI must show that growth translates into better per-share economics. The most relevant confirmation would come from stable or declining share count, improving net income, stronger operating cash flow, lower cash burn, and consistent growth in cash flow per share. If the company continues to grow while limiting new issuance, the dilution risk becomes manageable. If the share count continues to rise faster than profitability and cash generation, shareholder

Income

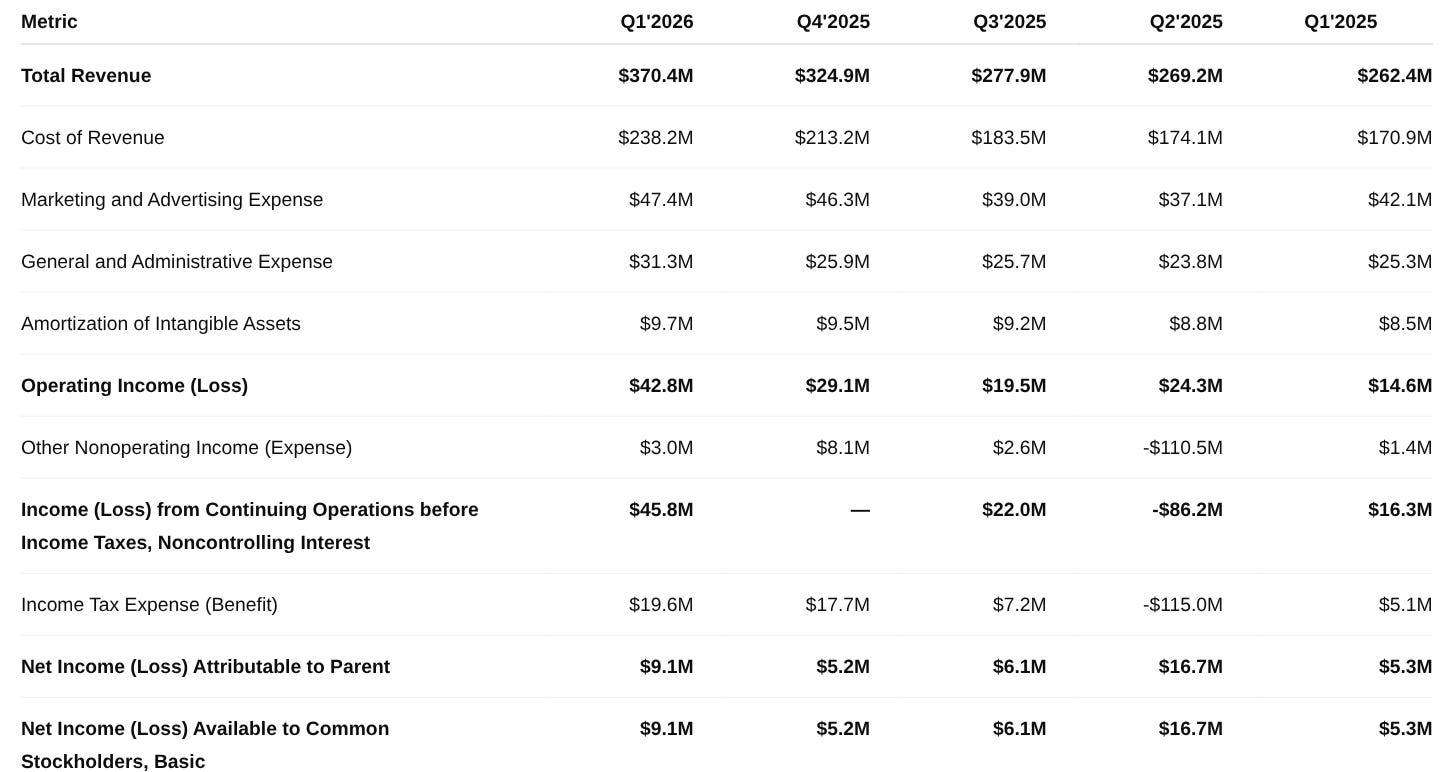

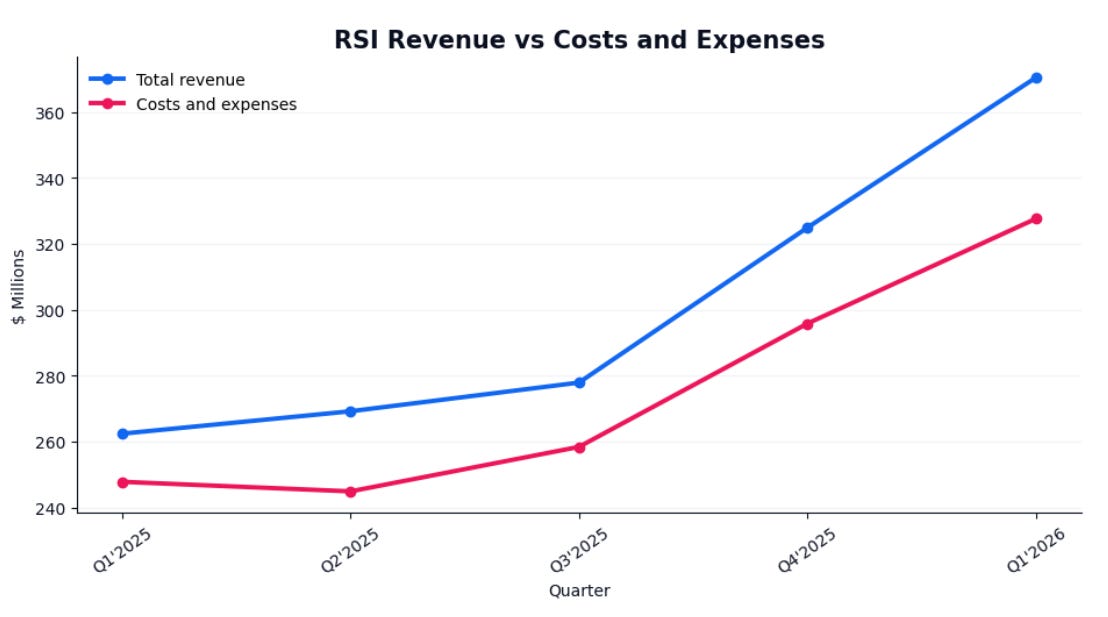

The income statement shows a company with strong top-line growth and improving operating leverage. Total revenue increased from $262.4M in Q1 2025 to $370.4M in Q1 2026, representing approximately 41% year-over-year growth. Sequentially, revenue also increased from $324.9M in Q4 2025 to $370.4M in Q1 2026, showing that the company continued to expand beyond the previous quarter.

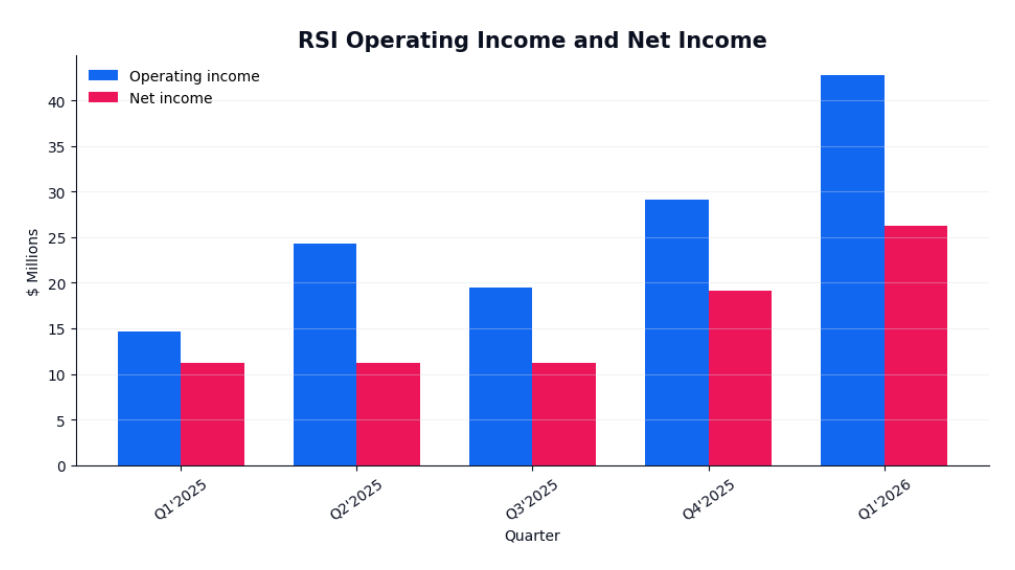

Operating income also improved significantly. RSI generated $42.8M in Q1 2026, compared with $14.6M in Q1 2025. That represents an increase of almost 193% year over year. This is a positive signal because operating income grew much faster than revenue, which indicates that the company is gaining operating leverage. Basically, RSI is converting a larger portion of its revenue into operating profit.

Cost of revenue increased from $170.9M in Q1 2025 to $238.2M in Q1 2026. This increase is expected given the higher revenue base, but it grew slightly slower than revenue. As a result, gross profit improved from $91.5M in Q1 2025 to approximately $132.2M in Q1 2026. Gross margin also improved slightly, from around 34.9% to 35.7%. This margin stability is important because it shows that RSI’s revenue growth is not being achieved through a major deterioration in direct profitability.

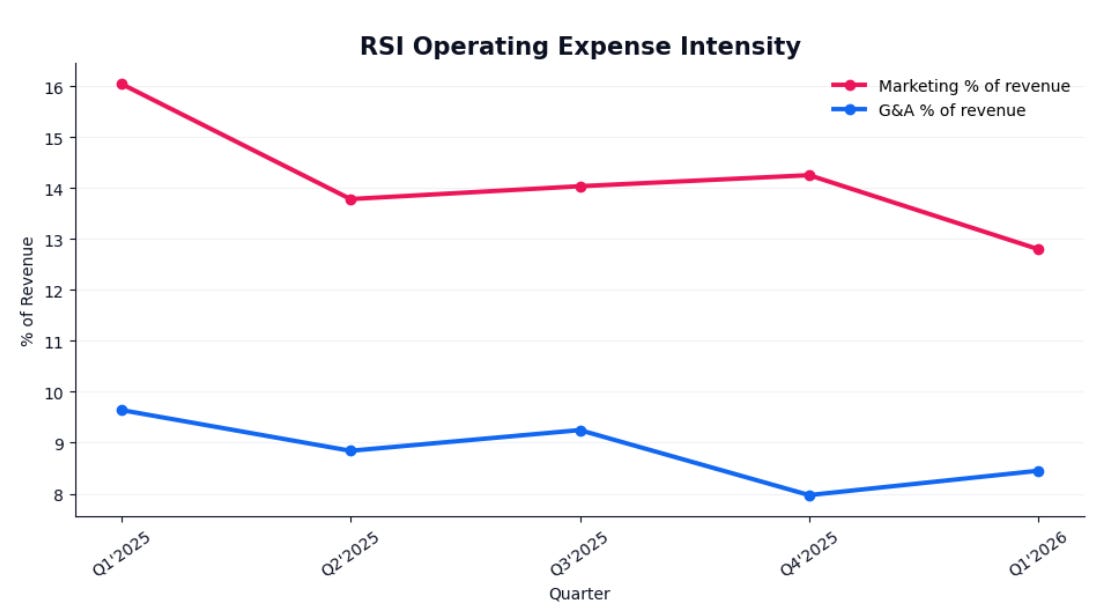

Marketing and advertising expense is especially important for an online gambling company because customer acquisition is one of the main drivers of both growth and risk. RSI spent $47.4M on marketing and advertising in Q1 2026, compared with $42.1M in Q1 2025. In absolute terms, marketing expense increased. However, as a percentage of revenue, it declined from 16.0% in Q1 2025 to 12.8% in Q1 2026. It indicates that RSI generated more revenue without increasing marketing spend at the same pace. From an investor’s perspective, this suggests improved marketing efficiency and better customer monetization.

General and administrative expense increased from $25.3M in Q1 2025 to $31.3M in Q1 2026. The increase is material, but it remained controlled relative to revenue growth. As a percentage of revenue, G&A declined from approximately 9.6% to 8.5%. This supports the same operating leverage argument. The company is scaling revenue faster than some of its operating cost categories.

Total costs and expenses increased from $247.8M in Q1 2025 to $327.6M in Q1 2026, an increase of 32%. Since revenue increased by 41%, the income statement shows a favorable spread between revenue growth and expense growth. This spread is what drives the improvement in operating income. This shows that the company’s growth is translating into better profitability.

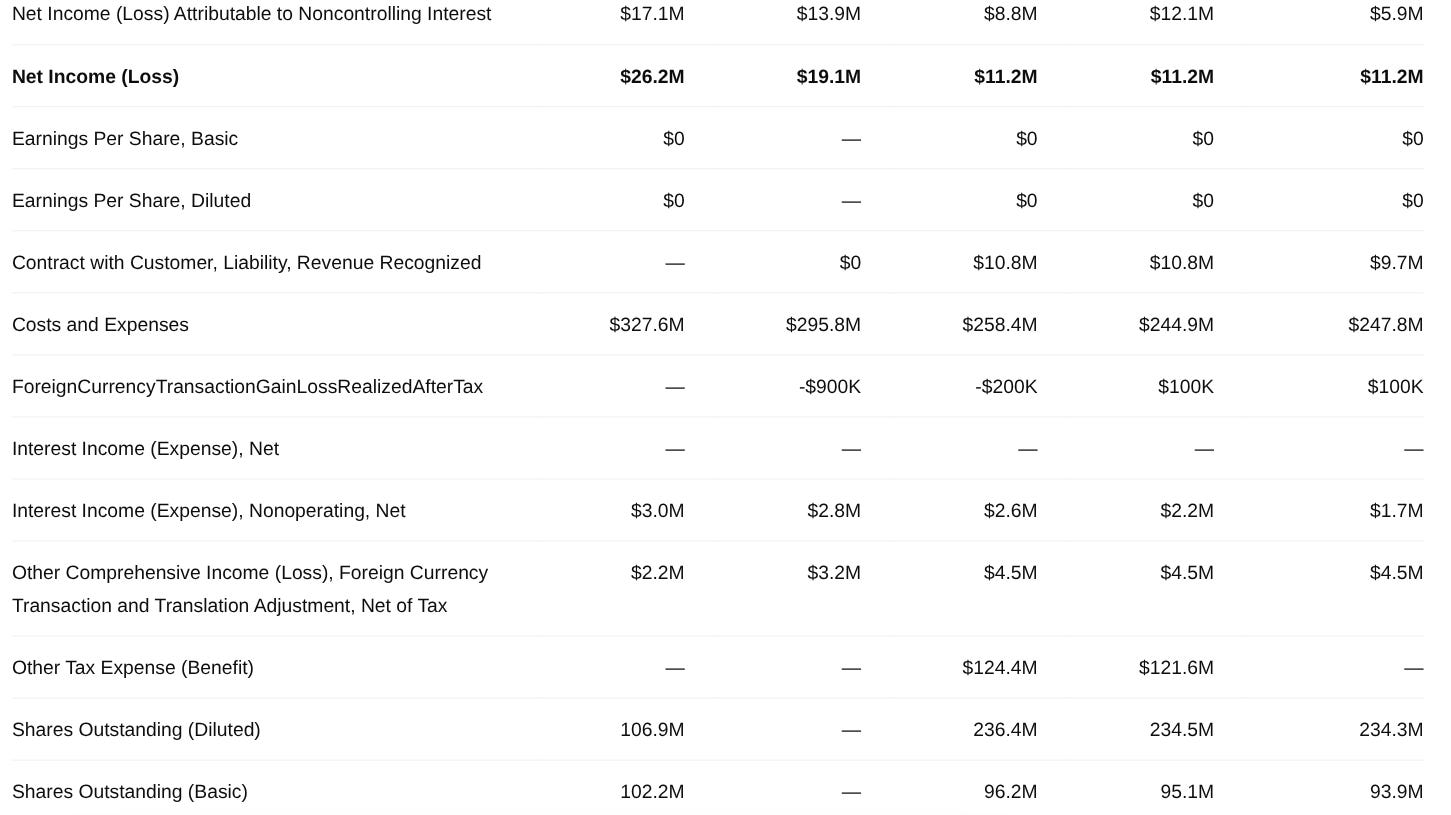

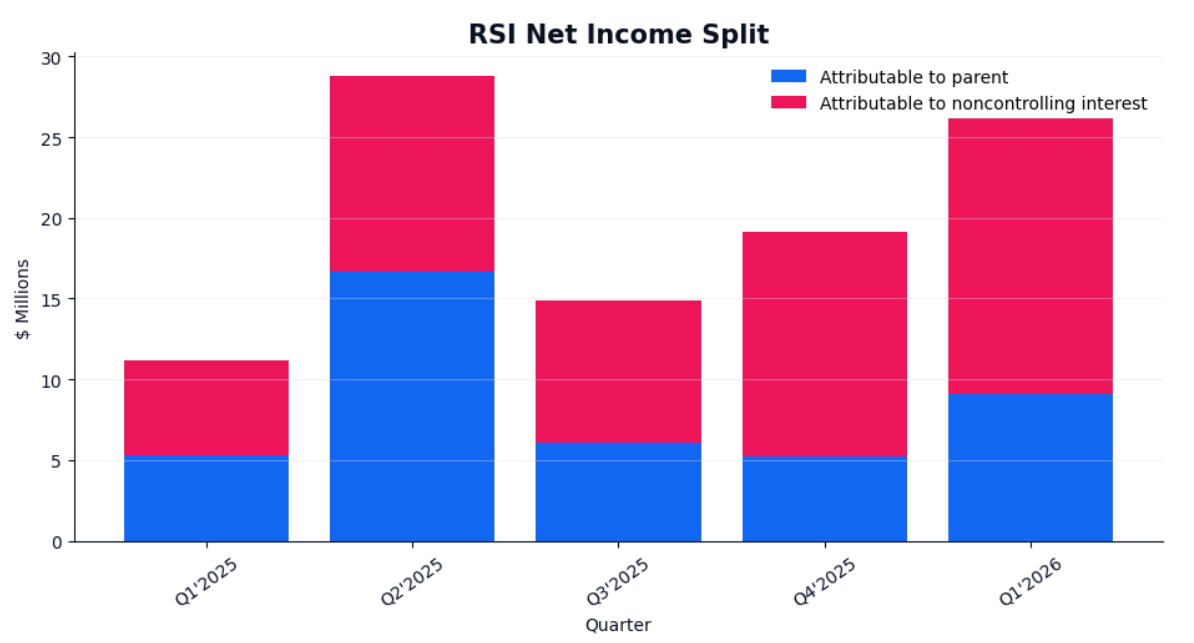

Net income also improved. RSI reported $26.2M of net income in Q1 2026, compared with $11.2M in Q1 2025. That represents growth of 134% year over year. Sequentially, net income increased from $19.1M in Q4 2025 to $26.2M in Q1 2026. This confirms that the improvement is visible also at the bottom line.

However, the data also shows that not all net income belongs directly to common shareholders. Net income attributable to the parent was $9.1M in Q1 2026, while net income attributable to noncontrolling interest was $17.1M. RSI’s structure means that investors should continue separating consolidated net income from income available to common shareholders.

The Q2 2025 column contains unusual items that distort comparability. Other nonoperating income was negative $110.5M, while income tax expense showed a benefit of $115.0M. These two large items heavily affected pre-tax income and tax expense, making Q2 2025 less useful as a clean operating comparison. For that reason, Q1 2026 should be compared more directly with Q1 2025, Q3 2025, and Q4 2025 when analyzing recurring income statement performance.

Earnings per share is shown as $0 across the quarters. This means EPS is not very informative, likely because of rounding, share structure, or the relationship between consolidated income and income attributable to common stockholders.

Basic shares outstanding increased from 93.9M in Q1 2025 to 102.2M in Q1 2026, an increase of approximately 8.8%. This is relevant because the company’s profitability improved, but shareholders also experienced dilution. The key investor question is whether earnings and cash flow are growing faster than the share count. In Q1 2026, profit growth exceeded share count growth, but the share count still needs to be monitored.

Overall, RSI’s income statement shows a stronger operating profile than the prior year. Revenue growth is strong, operating income is expanding faster than revenue, marketing expense is becoming more efficient as a percentage of sales, and net income is improving. The main investor watchpoints are the split between consolidated net income and income attributable to common shareholders, the unusual nonoperating and tax effects in Q2 2025, and the continued increase in basic shares outstanding.