[INTEL REPORT] Economic policy and structural adjustments

Analysis of United States monetary policy, japanese fiscal strategy, and technology infrastructure capital expenditure

Table of contents:

Introduction.

The transition of United States monetary policy.

Japanese fiscal expansion and economic strategy (2026–2041).

The economics of AI infrastructure.

Evolution of digital banking and financial markets.

Asset allocation and portfolio reallocation.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

The global financial architecture enters a phase of profound structural realignment. In the United States, the ascension of Kevin Warsh to the chairmanship of the Federal Reserve establishes a new paradigm for monetary policy. This regime prioritizes strategic ambiguity, concise communication, and an insulation of policy actions from market expectations.

Cross-border economic dynamics mirror this institutional transformation. Japan embarks on an expansive macroeconomic doctrine under Prime Minister Sanae Takaichi. The multi-decade investment framework combines state capital with structural reforms to foster domestic technology hubs and automation systems, accepting sovereign balance sheet expansion as a necessary trade-off for long-term production growth.

The catalyst for global capital movement remains the physical construction of artificial intelligence infrastructure. Corporate entities allocate immense capital budgets toward advanced silicon accelerators, specialized liquid-cooled data facilities, and direct power grid access. This investment cycle transitions technical software capabilities from passive digital applications into autonomous agentic systems, altering corporate expenditure structures.

Parallel disruptions redefine the financial services sector. Cloud-native digital banks secure full regulatory charters, dismantling legacy moats through multi-engine platforms. Diversified streams of interest income, asset management, and subscription products yield sustainable corporate profitability, transforming consumer habits and global market shares.

Go deeper by checking:

These combined shifts mandate a thorough restructuring of investment strategies. Effective asset allocation demands precise duration management in fixed income portfolios, active regional strategies within emerging markets, and a balance between technology growth assets and cash-generating cyclical industries. The subsequent sections detail these structural microeconomic changes and outline concrete frameworks for institutional capital reallocation.

The transition of United States monetary policy

“Real transparency doesn’t always mean more. But it should always mean better... If you’re not very good at something, you should do less of it. Stop talking so much. More thinking, less talking.”

— Kevin Warsh, outlining his reform doctrine prior to taking office as the 17th Chair of the Federal Reserve.

The transition of leadership at the Federal Reserve in mid-2026 represents one of the most volatile, legally contested, and philosophically disruptive chapters in the history of modern central banking. Following the swearing-in of Kevin Warsh as the 17th Chair of the Federal Reserve on May 22, 2026, the institution has embarked on a fundamental regime shift. Confronted by sticky inflation driven by Middle East energy supply shocks and a vocal, growth-oriented executive branch, Warsh has initiated an aggressive overhaul of monetary policy communications and structural frameworks. This transition of the Federal Reserve chairmanship was defined by unprecedented institutional friction, cutting across all three branches of the federal government and challenging long-standing norms of monetary independence.

The political battle to confirm Kevin Warsh began in earnest within a polarized Senate. On May 13, 2026, the United States Senate confirmed Warsh as Chairman of the Board of Governors by a razor-thin margin of 54 votes in favor to 45 against. This vote established a record for the narrowest confirmation margin for a Federal Reserve Chair in U.S. history, eclipsing the previous record set by Ben Bernanke’s 70 - 30 confirmation vote in 2010. The division was partisan, reflecting deep ideological splits over the future of monetary policy and central bank oversight. The Republican majority voted as a unified block in favor of Warsh, viewing him as a reformer capable of bringing accountability and market discipline to an institution they argued had overstepped its mandate. Democratic Senator John Fetterman of Pennsylvania crossed party lines to join the Republican majority, citing Warsh’s explicit commitment during hearings to increase congressional responsiveness and dismantle what he termed the “incomprehensible jargon” of Fed communications. Conversely, prominent progressive critics, led by Senator Elizabeth Warren, fiercely opposed Warsh. They labeled him a “sock puppet” for the executive branch and Wall Street, citing his regulatory positions during the 2008 global financial crisis and his public alignment with President Donald Trump’s pro-growth, low-interest-rate rhetoric in the lead-up to his nomination.

The nomination path was logjammed for months within the Senate Banking Committee due to a high-stakes standoff involving outgoing Chair Jerome Powell. Senator Thom Tillis placed a temporary hold on Warsh’s nomination, demanding that the Department of Justice terminate its criminal investigation into Powell regarding a controversial, multi-million-dollar renovation of the Federal Reserve’s Washington headquarters. Tillis and other committee members argued that the Department of Justice probe was a “frivolous, politically motivated prosecution” designed to compromise central bank independence and coerce the Fed into lowering interest rates. On April 24, 2026, the Department of Justice announced it would drop the criminal probe and refer the matter to the Federal Reserve’s independent Inspector General. This concession broke the legislative deadlock, allowing the Senate Banking Committee to advance Warsh’s nomination to the Senate floor in a tense, party-line 13-11 vote.

Simultaneously, the Federal Reserve became the battleground for one of the most critical executive power disputes in American history. In August 2025, President Donald Trump attempted to terminate Board Governor Lisa Cook—originally appointed by President Joe Biden to a 14-year term ending in 2038—alleging mortgage fraud on her historical loan agreements. Cook unequivocally denied the allegations, characterizing them as a bad-faith pretext to clear a seat on the Board for a monetary dove. Cook sued to halt her removal, arguing that under 12 U.S.C., Federal Reserve Governors may only be removed by the President “for cause” and are entitled to robust due process. On June 29, 2026, the Supreme Court ruled 5 - 4 in Trump v. Cook (No. 25A312) to uphold a lower court’s preliminary injunction, blocking her removal.

Chief Justice John Roberts delivered the majority opinion, joined by Associate Justice Brett Kavanaugh and the three liberal justices (Justices Sotomayor, Kagan, and Jackson). The Court held that while the executive branch possesses broad authority over executive departments, the Federal Reserve’s unique role in maintaining economic stability requires protection from arbitrary political interference. The Court ruled that Cook was entitled to basic due process—including an explanation of the evidence, a formal notice, and a meaningful opportunity to respond—and that because the administration failed to provide this, the attempted removal was “erroneous and void.” The dissent, led by Justice Clarence Thomas and joined by Justices Alito, Gorsuch, and Barrett, argued that the President’s Article II removal power should extend unconditionally to all independent agency heads.

Jerome Powell’s official chairmanship expired on May 15, 2026, but his 14-year term as a Fed Governor is legally protected until January 2028. To defend institutional continuity and preserve the Board’s legal defenses amid the ongoing Inspector General probe, Powell took the rare step of choosing to remain on the Board of Governors as a regular member. This decision triggered an immediate structural shift. To make room for Warsh’s confirmation to the Board, temporary Trump appointee Stephen Miran—a vocal monetary dove who had registered formal dissents in favor of interest rate cuts at six consecutive meetings—was displaced. With Miran off the Board and Powell remaining alongside Cook, Warsh must now build consensus within a deeply divided, legally embattled seven-member Board of Governors, navigating factions that are highly protective of Powell’s policy legacy.

Do you need to make better decisions when buying or selling stocks? Take a look at QuantX.es

The Federal Open Market Committee convened on June 16–17, 2026, for its inaugural session under Chairman Warsh. While the committee’s decision to maintain the federal funds target range at 3.50% - 3.75% was anticipated by Wall Street, the shift in operational style, post-meeting statement architecture, and communications philosophy took market participants by surprise. In a calculated break from two decades of hyper-detailed central bank communication, Warsh slashed the post-meeting statement to a mere 114 words. This was a reduction from the 244 words issued in April and historical averages of over 300 words. The radical brevity of the June statement accomplished three key objectives:

Omission of forward guidance: The statement removed all explicit qualitative and quantitative guidance regarding future interest rate trajectories, replacing references to “additional firming” or “gradual easing” with a blank slate.

Elimination of the participant roster: The customary list of meeting attendees and their individual voting records was removed from the primary statement, consolidating the policy decision under the corporate identity of the Committee.

Macroeconomic condensation: Rather than providing granular details on consumer spending, employment metrics, and business fixed investment, the document condensed the economic landscape into a single sentence, stating that economic activity is “expanding at a robust pace, and productivity and investment remain strong.”

Warsh has long been a vocal academic and professional critic of forward guidance, arguing that the practice has transformed the Fed from a reactive monetary authority into a captive of market expectations. In his view, the Fed’s 2021 - 2022 failure to contain inflation stemmed directly from its self-imposed forward-guidance trap, which made the central bank hesitant to raise rates for fear of triggering market volatility. By introducing “strategic ambiguity,” Warsh seeks to reintroduce two-way risk to financial markets. Under this philosophy, the Fed treats market pricing as an organic, independent source of information rather than a metric to be managed and massaged. The central bank communicates only its core objective—price stability—and leaves the precise path of interest rates intentionally vague, forcing market participants to conduct independent fundamental analysis. The policy statement is no longer used as a monetary tool in itself, but rather as a direct, unvarnished summary of current actions.

The macroeconomic backdrop in mid-2026 is challenging, exhibiting classic signs of stagflationary stress. Geopolitical escalations in the Middle East have severely disrupted global shipping lanes and energy infrastructure, pushing domestic Brent crude prices back above $100 per barrel. Consequently, the consumer price index climbed to a three-year peak of 4.2% in May 2026. The June Summary of Economic Projections reflected these mounting pressures. The core Personal Consumption Expenditures inflation forecast for 2026 was marked up significantly from 2.7% in March to 3.6% in June, while real GDP growth expectations were revised downward by 20 basis points to 2.2%.

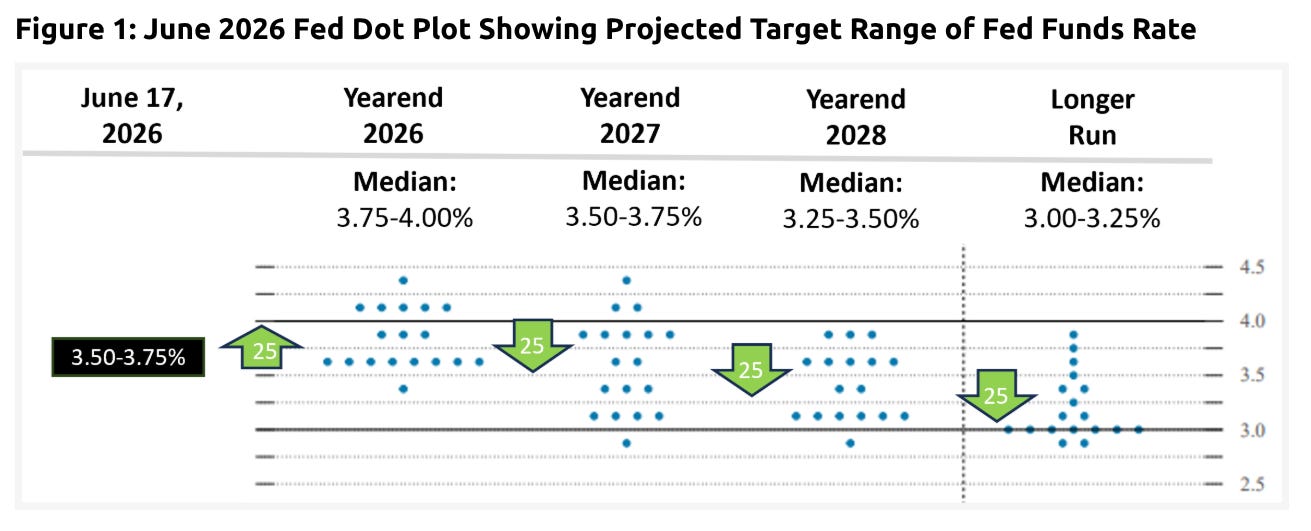

In a symbolic protest against the forward-guidance utility of the Summary of Economic Projections, Chairman Warsh declined to submit his own interest rate projection for the Dot Plot. Warsh argued that the Dot Plot creates a false sense of certainty and encourages herd behavior among governors. By leaving his “dot” missing, he signaled that the Chairman of the Federal Reserve is not bound by a pre-committed path, thereby maximizing his tactical flexibility in upcoming meetings. Despite the Chairman’s absent dot, the remaining 17 participating officials revealed a deeply fractured committee struggling to find consensus. Nine of the eighteen participating officials now project a minimum of one 25 basis point rate hike before the end of the year, bringing the median year-end target to 3.75% - 4.00%. This is a sharp hawkish shift from the March 2026 projections, which had anticipated a median of 25 basis points of rate cuts by December. The remaining members are split between keeping rates unchanged and advocating for immediate cuts to protect the labor market from the compounding effects of high energy costs.

To reshape both the operational mechanics and the theoretical foundation of the Federal Reserve, Warsh announced the creation of five specialized internal task forces. Each group, which includes independent outside experts alongside Fed insiders to ensure better cognitive diversity, is mandated to deliver concrete, actionable policy proposals by December 2026:

Communications Reform Task Force: This group is tasked with formalizing the reduction of post-meeting press conferences from eight per year to four, limiting the volume of public speeches delivered by regional Fed presidents, and designing a framework to phase out the Dot Plot. The objective is to quiet the “noise” of public central bank commentary, allowing the markets to focus exclusively on formal policy decisions and get central bankers off the front page.

Balance Sheet Management (Quantitative Tightening) Task Force: This task force is exploring an acceleration of the Fed’s asset runoff program. The Federal Reserve’s balance sheet has declined from its pandemic-era peak of nearly 9 trillion to approximately 6.7 trillion (roughly 21% of GDP) by mid-2026. Warsh is an advocate of a “lean” balance sheet, arguing that the massive footprint of central bank holdings distorts market pricing, crowds out private capital, and disproportionately benefits owners of financial assets at the expense of broader society. The task force is evaluating plans to sell agency mortgage-backed securities outright to hasten the return to an all-Treasury portfolio.

Data Quality Metrics Task Force: Charged with evaluating the “data-dependent” framework of the Powell era, this group seeks to transition the Fed away from backward-looking, lagging indicators (such as the monthly establishment survey for employment) and toward real-time market signals. This includes the integration of high-frequency transactional data, corporate credit spreads, and market-implied inflation expectations into the Fed’s forecasting models.

AI and Productivity Dynamics Task Force: This task force is studying the supply-side impact of artificial intelligence integration across the economy. Warsh holds a structurally bullish outlook on technology, arguing that AI-driven productivity gains can increase the non-inflationary capacity of the economy. Under this theory, an elevated growth rate does not necessarily require a restrictive interest rate stance, as productivity gains naturally suppress unit labor costs. Understanding this dynamic is central to Warsh’s long-term plan to lower rates safely without triggering wage-price spirals.

Inflation Framework Review Task Force: This group is reviewing alternative inflation metrics to replace or supplement standard core PCE, which Warsh argues has been distorted by housing models and transient geopolitical spikes. The task force is focused on “trimmed mean” metrics, such as the Dallas Fed Trimmed Mean PCE and the Cleveland Fed 16% Trimmed Mean CPI. Because these metrics strip out extreme price outliers on both sides, they currently track below standard core PCE, providing what Warsh argues is a more stable measure of baseline inflation.

The introduction of “strategic ambiguity,” combined with the hawkish shift in the June Summary of Economic Projections, triggered immediate repricing across global financial markets. Following Warsh’s June press conference—during which he referenced the central bank’s commitment to “price stability” 12 times—investors adjusted their expectations for the interest rate path. The 2-year Treasury yield surged by 13 basis points, reflecting immediate expectations of a more restrictive short-term policy path and a potential rate hike by November. Meanwhile, the 10-year Treasury yield rose by just 3 basis points. This classic bear-flattening move indicates that while markets expect higher policy rates in the near term, they also expect these rates to successfully cool long-term growth and inflation. The US Dollar Index appreciated by 0.75%, reversing its losses from the prior week, while the S&P 500 retracted by 0.5%. The bond futures market now prices in an 85% probability of a rate hike by the close of 2026.

This hawkish pivot has created a direct conflict with the executive branch. President Donald Trump, who nominated Warsh with the explicit expectation that he would deliver lower interest rates to support his tariff and tax-cutting economic agenda, has expressed strong dissatisfaction with the Fed’s restrictive stance. This friction represents a critical test of central bank independence. In the 1970s, political pressure from the Nixon administration coerced Fed Chair Arthur Burns into maintaining artificially low interest rates, triggering a decade of stagflation. Academic economists and former Fed officials, including those represented by organizations like the Washington Center for Equitable Growth, have pointed to this period as a warning.

Some market commentators and progressive critics have proposed a more cynical interpretation of Warsh’s strategic shift. They suggest that the elimination of forward guidance and the heavy reliance on “strategic ambiguity” serve as a personal and political shield for the new Chairman. By refusing to commit to an explicit interest rate path, Warsh avoids direct, early confrontations. The Trump administration is permitted to believe he is a structural dove who is simply nudging a reluctant committee, while Wall Street can interpret his silence as orthodox, hawkish commitment to price stability. So long as he preserves this ambiguity, Warsh insulates himself from immediate political fallout while solidifying his control over the FOMC. However, this approach risks injecting significant term premiums and volatility into the fixed-income markets as investors lose their traditional policy guideposts and are forced to discover prices entirely on their own.