Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

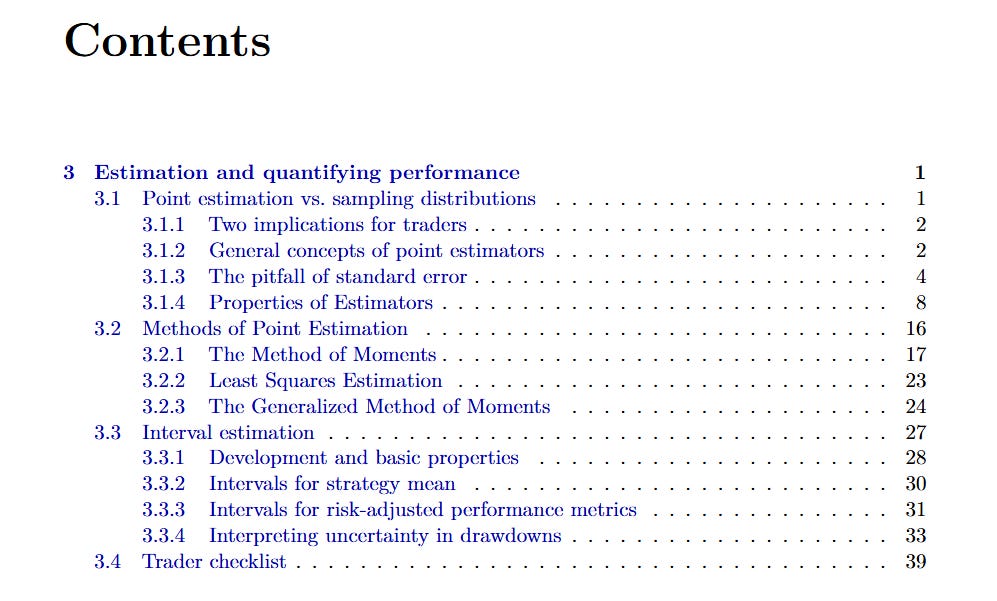

Estimation and Quantifying Performance

This chapter shifts from describing data to extracting knowledge from it. The focus is on estimation—building point values, intervals, and diagnostics that quantify the strength of a trading edge while accounting for noise, dependence, and structural breaks. Rather than treating a backtest as deterministic, we reframe it as one draw from an uncertain process. The tools covered here help separate true skill from random variation, ensure reported metrics are statistically defensible.

What’s inside:

From backtest to inference: Why a single equity curve is just one draw from a process, and how sampling distributions let you separate edge from luck. Learn the two trader takeaways: quantify uncertainty and do it correctly for time-series data.

Uncertainty that respects dependence: Practical fixes for serial correlation and heteroskedasticity—effective sample size intuition, Newey–West (HAC) standard errors, and block bootstrap resampling for robust standard errors and CIs.

Point-estimation toolbox: Method of Moments (with a scaled-Beta daily-range example), Least Squares (factor exposure, hedge ratios, alpha testing), and GMM moment-condition thinking used across empirical asset pricing.

Interval estimation that matters to traders: Build intervals for the strategy mean, risk-adjusted metrics (e.g., Sharpe with Lo’s autocorrelation-aware annualization), and interpret uncertainty in drawdowns.

Estimator properties under market stress: Move beyond textbook bias/variance—contrast MSE vs. MAE for outlier-heavy data, use asymmetric (quantile/pinball) loss when under- vs over-prediction costs differ.

Robust distributional characterization: L-moments (location, scale, skew, kurtosis) as outlier-resistant summaries of returns, with clear Python to compute them from scratch.

Operational diagnostics & governance: Rolling and EW error monitoring, simple CUSUM break detection, and bootstrap CIs for Lo-corrected Sharpe—turning statistics into live risk controls and de-risking triggers.

Check a sample of what you will find inside: