Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

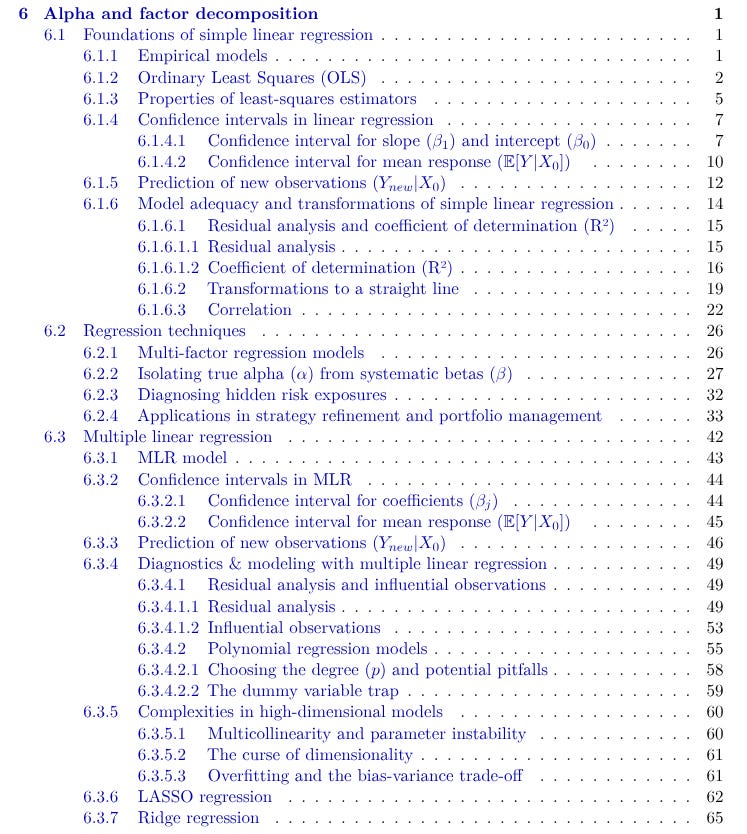

Alpha & Factor Decomposition

This chapter frames factor analysis as a decision tool: use regression to separate true edge (α) from systematic risk premia (β), diagnose hidden exposures, and turn findings into concrete hedges and portfolio rules. The workflow runs from simple/ multiple regression foundations to multi-factor models, statistical significance of α, rolling diagnostics, and implementation.

What’s inside:

Regression bedrock. Simple OLS, estimator properties, and how to form CIs for slope/intercept, mean response, and prediction intervals.

From one factor to many. Build multi-factor regressions to explain returns with partial betas.

Isolating true alpha. Regress excess returns on factors; the intercept (α) is the skill component.

Hidden risk exposures. Find “beta leaks,” factor crowding, sector concentration, liquidity sensitivity, and style drift via rolling betas and CIs.

Actionable applications. Neutralize unintended betas with minimum-variance hedges; construct factor-neutral, residual-Sharpe-oriented blends and keep betas in check over time.

Model adequacy & transforms. Residual checks, R2 and transformations (log/Box-Cox) to stabilize variance and linearize relations.

Multiple Linear Regression (MLR). Extend to many predictors; diagnostics for influential points, polynomial terms, and the dummy-variable trap.

Risk-aware inference. Use mean-response CIs vs. wider prediction intervals for trading decisions (stops/targets/position sizing) and report robust stats alongside fit.

Again, I have decided to devide this chapter in several parts because it’s pretty long.

Check a sample of what you will find inside: