[INTEL REPORT] US vs. Europe

Divergent growth, politics, and policy: who compounds, who stagnates

Table of contents:

Introduction.

Three fronts of global instability.

Europe’s rearmament and the new iron curtain.

2. US-China relations.

Middle east crossroads.

The bubble and the first domino.

Anatomy of a systemic crisis.

The twilight of the Dollar.

US vs. Europe.

Updates on capital allocation for 2026-2027.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

We’re in the middle of a Great Divergence. In Europe, a new era of state-driven conflict and rearmament is setting up what looks like a long defense investment cycle. At the same time, US–China relations and parts of the Middle East show flashes of pragmatic cooperation, creating short-term openings even within a more fractured geopolitical order.

On the economic side, headline numbers in the US look strong, but beneath the surface the structure is weak: productivity growth is stalling, fiscal imbalances are widening, and household balance sheets are stretched. Years of central bank liquidity have also created a historic, cross-asset bubble. That bubble is now under visible stress, with the biggest fragility concentrated in private credit, where opacity and liquidity mismatches are hardest to price.

Check this report for more data:

The primary geopolitical dynamic is the “Europeanization” of the Ukraine conflict. Driven by a strategic pivot from the United States, this shift is forcing a fundamental reallocation of European capital away from social welfare and toward military hardware. This is not a temporary fiscal measure but a generational transformation, epitomized by Germany’s security policy revolution, the Zeitenwende.

The central macroeconomic paradox presents investors with a dangerous contradiction. US stock market valuations are at or above the peaks seen before the 1929 and 1999 crashes, while the underlying financial plumbing is showing signs of critical failure. The recent, sudden collapse of First Brands Group, a company with potential liabilities of up to $50 billion, serves as a stark warning of hidden leverage and contagion risk emanating from the private credit sector. Concurrently, the US dollar appears poised for a secular decline, a development that threatens its global reserve status and signals a major regime change for global asset allocation.

This environment necessitates a decisive shift in investment strategy. The highest-conviction theses for the coming period are:

Long european defense.

Long hard assets.

Selective emerging markets & commodities.

The key imperatives are:

Systemic credit contagion.

European capital flight.

Market bubble collapse.

Three fronts of global instability

Europe’s rearmament and the new iron curtain

The war in Ukraine has transitioned from an acute crisis to be resolved into a long-term, structural condition to be managed. This shift is fundamentally reshaping European security, defense policy, and fiscal priorities. Recent events have shattered any residual illusions of a near-term diplomatic solution. Over the last week of September 2025, Russia launched one of the most intense bombardments of the war, firing nearly 600 drones and over 40 cruise missiles at Kyiv and other major Ukrainian cities over a 12-hour period. This massive assault, which killed civilians and struck a cardiology institute, underscores Moscow’s commitment to a protracted conflict and has been met with widespread international condemnation.

This escalation coincides with a dramatic strategic pivot by the Trump administration. After previously calling for concessions, President Trump has reversed course, now publicly stating his belief that Ukraine can win back all territory lost to Russia. This rhetorical shift, however, masks a deeply transactional policy. The new US strategy is not to underwrite Ukraine’s defense directly, but to facilitate a massive transfer of American weaponry to Ukraine, funded entirely by European allies. Dutch Prime Minister Mark Rutte confirmed this dynamic, describing a forthcoming “voracious, brutal” flow of US arms to Ukraine that will be paid for by Europe. This approach effectively transforms the NATO alliance into a captive market for the US military-industrial complex. The strategic consequence is that the United States is engineering a long-term European dependency, containing Russia at Europe’s expense while simultaneously bolstering its own defense industry and weakening Europe as a long-term economic competitor through higher energy and defense costs. European leaders are acutely aware of this shift, with Polish Prime Minister Donald Tusk voicing fears that the US is positioning itself to blame Europe for any future failures in Ukraine.

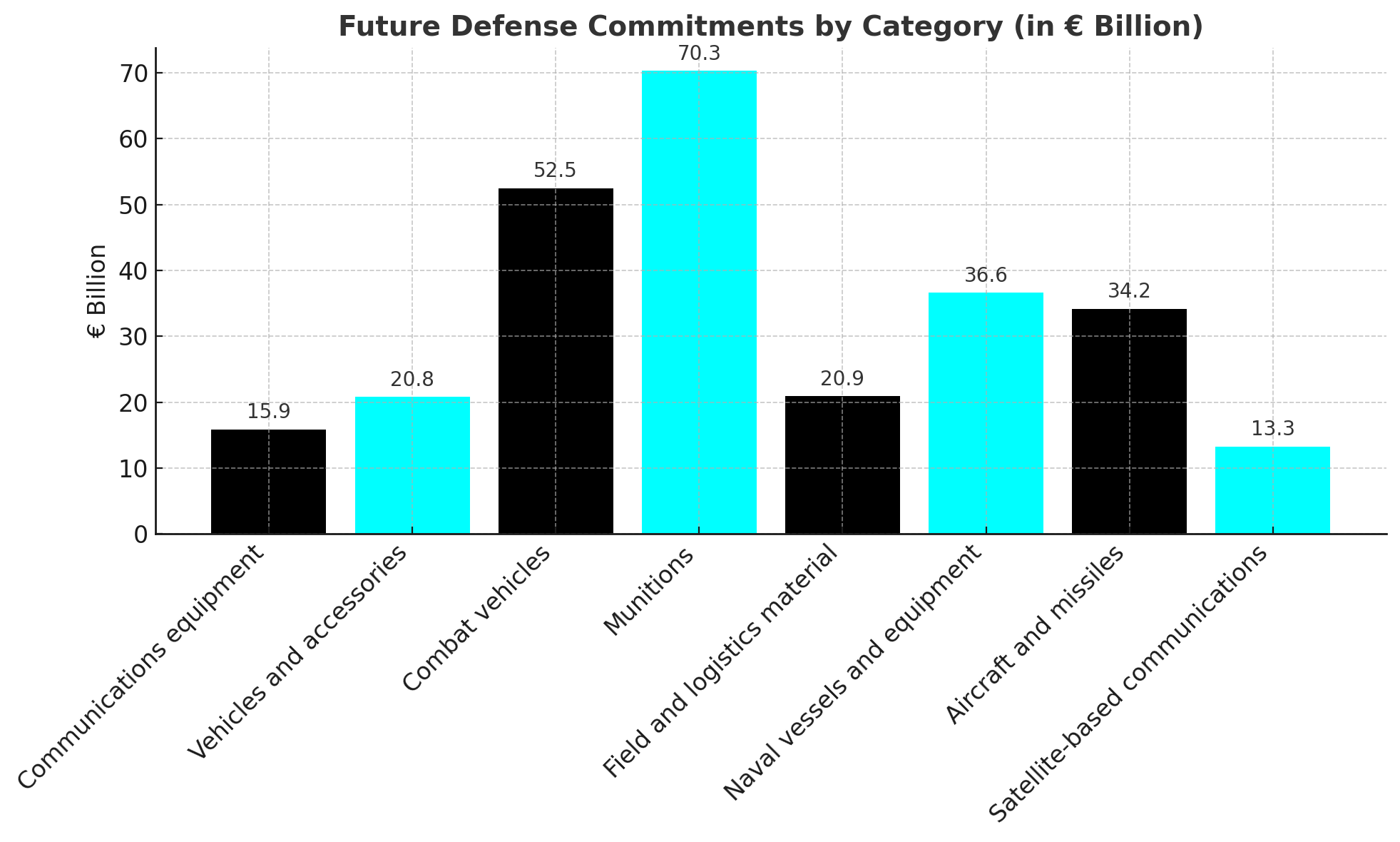

The engine of this new European reality is Germany. The nation is undergoing a historic strategic pivot known as the Zeitenwende (turning point), a complete reversal of its post-World War II pacifist doctrine. This is not mere political rhetoric; it is a societal transformation backed by immense and legally binding financial commitments. A €100 billion special defense fund (Sondervermögen) has been established to overhaul the chronically underfunded German armed forces, the Bundeswehr. Berlin has committed to spending at least 2% of its GDP on defense and, according to a recent announcement, plans to double its current military spending to hit a target of 3.5% of GDP. The planned defense budget is set to rise from €86 billion in 2025 to €108.2 billion in 2026.

A newly revealed procurement plan details the scale of this effort, outlining nearly €83 billion in contracts to be approved between September 2025 and December 2026 alone. This is part of a multi-decade framework totaling over €350 billion ($409 billion) through 2041, with long-term commitment authorizations designed to lock in spending for future governments. Underscoring the societal depth of this change, Germany is reintroducing military service in 2025. The plan begins with mandatory registration for all 18-year-old men and aims to build a combined force of 460,000 active soldiers and reservists by 2030. This is a clear signal that Germany’s rearmament is a generational project, underwritten by a perception of existential threat. The spending is non-discretionary and insulated from normal political and economic cycles, creating one of the most reliable, long-term investment themes in the global economy.

The conflict is also exposing new technological and tactical realities, creating urgent new markets. The proliferation of cheap Russian drones has revealed a critical vulnerability in NATO’s air defenses. With drones costing as little as $2,000 to produce, NATO is being forced to expend advanced air defense missiles costing between $500,000 and $1 million each to intercept them—a cost-exchange ratio that NATO Secretary General Mark Rutte has publicly admitted is not sustainable. This unsustainable asymmetry is creating an immediate and massive demand for cost-effective counter-drone technologies, from electronic warfare systems to directed energy weapons and specialized gun systems.

US-China relations

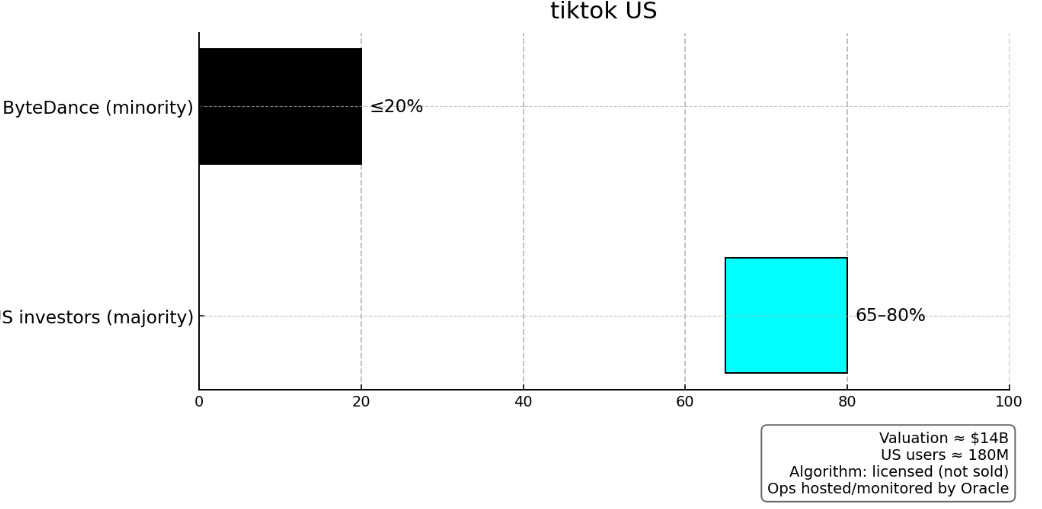

While military tensions escalate in Europe, the relationship between the US and China is evolving towards a form of managed competition, characterized by pragmatic deal-making in some areas and continued friction in others. The most significant development is the resolution of the multi-year standoff over the social media platform TikTok. The Trump administration has brokered and approved a deal to divest TikTok’s US operations to a consortium of American investors, including Oracle, and prominent figures such as Rupert Murdoch and Michael Dell. Chinese President Xi Jinping has reportedly given his go-ahead for the deal, signaling a mutual desire to de-escalate this particular conflict.

The structure of the deal is a landmark event in global technology policy. The new US-based entity is valued at approximately $14 billion. American investors are expected to hold a majority stake of around 65% to 80%, while TikTok’s Chinese parent company, ByteDance, will retain a minority interest of less than 20%. The most critical and sensitive component—the content recommendation algorithm—will not be sold outright. Instead, it will be licensed to the new US entity and retrained using only US user data, with all operations hosted and monitored by Oracle to ensure a firewall from Chinese influence.

This arrangement establishes a new template for technological decoupling. It allows the US to neutralize a perceived national security threat—the potential for data harvesting and propaganda by Beijing—without resorting to an outright ban, which would be politically unpopular with TikTok’s 180 million American users and economically disruptive. For China, it represents a pragmatic compromise that preserves a significant financial interest in a valuable global asset. However, the deal’s opacity raises significant long-term questions about what concessions the US may have offered Beijing on other, more critical national security issues, such as Taiwan, to secure its approval.

Despite this tactical détente, Taiwan remains the core friction point in the strategic rivalry. According to a Wall Street Journal report, Xi Jinping’s primary objective in his broader negotiations with President Trump is to secure a formal US commitment opposing Taiwanese independence. In response to continued US arms sales to Taipei, Beijing has escalated its use of sanctions. Last week, China sanctioned six US companies. Three firms—unmanned vehicle maker Saronic Technologies, satellite technology company Aerkomm, and subsea engineering firm Oceaneering International—were added to China’s unreliable entity list, effectively banning them from all trade with and investment in China. Three other companies—military shipbuilder Huntington Ingalls Industries, Planate Management Group, and Global Dimensions—were placed on an export control list, preventing them from receiving Chinese shipments of dual-use items.

For most US defense contractors, which are prohibited by US law from selling to China, the direct financial impact of these sanctions is negligible. The move is largely symbolic, intended to signal Beijing’s unwavering resolve on Taiwan. However, for a company like Oceaneering International, which has extensive global commercial operations, including in Asia, the ban could prove more disruptive to its non-defense business lines. The sanctions should therefore be interpreted not as a direct economic threat to the US defense sector, but as a clear indicator of Beijing’s rising political risk tolerance regarding Taiwan. The danger is not that a defense firm loses non-existent business in China, but that this escalating cycle of tit-for-tat actions could lead to a strategic miscalculation and a military confrontation in the Taiwan Strait.

For more about Oceaneering: