Table of contents:

Introduction.

December 2025 FOMC.

The hawkish cut.

The dovish dissent.

Flying blind into Q1 2026.

Tariffs, growth, and inflation.

Structural inflationary shift.

The fiscal offset.

The AI productivity paradox and the “jobless expansion”.

The 2026 outlook.

Investment strategy & asset allocation.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

As the global financial system pivots from the turbulent final quarter of 2025 into 2026, investors face a landscape defined by a profound “bifurcation”—a divergence in monetary policy views, economic data signals, and sectoral performance that has not been seen in decades. The Federal Reserve’s December 2025 meeting served as the inflection point for this new regime. While the Federal Open Market Committee (FOMC) delivered a widely anticipated 25 basis point reduction in the federal funds rate to a range of 3.50%–3.75%, the decision was accompanied by an unprecedented 9-3 split vote and a “hawkish cut” narrative that has fundamentally recalibrated market expectations.

The immediate economic backdrop is uniquely complex. The United States economy is emerging from a historic 43-day government shutdown—the longest in history—that created a significant “data void,” obscuring the true state of labor and inflation dynamics at a critical policy juncture. Simultaneously, the imposition of a 10% universal tariff, alongside significantly higher reciprocal levies on specific trading partners, is creating powerful cross-currents of inflationary pressure and growth drag that models are struggling to quantify. Despite these headwinds, the “animal spirits” of the market remain buoyed by the structural tailwind of Artificial Intelligence (AI) investment and a quiet but massive liquidity injection via the Fed’s new “Reserve Management Purchases” program—a mechanism effectively restarting balance sheet expansion under a new, less politically charged guise.

For investors, 2026 will not be a year of passive beta accumulation. The “easy money” trade of 2024-2025 is evolving into a market of extreme dispersion. The looming transition of the Fed Chairmanship in May 2026, with Kevin Hassett emerging as the distinct frontrunner, introduces a new vector of political and policy risk that threatens to upend the central bank’s reaction function. Consequently, our strategic outlook prioritizes active sector selection—favoring AI infrastructure and domestic producers over tariff-exposed importers—aggressive yield curve positioning in anticipation of a steepening curve, and hard asset diversification to hedge against the dual risks of sticky inflation and fiscal dominance.

This report provides a comprehensive analysis of these dynamics, synthesizing data from the December 2025 Fed meeting, post-shutdown economic indicators, and trade policy developments to offer a roadmap for portfolio allocation in the first half of 2026.

December 2025 FOMC

The December 10, 2025, FOMC meeting will likely be studied by financial historians as the moment the consensus era of the Powell Fed fractured. The meeting’s outcomes revealed deep fissures within the central bank’s leadership, reflecting the broader uncertainty plaguing the U.S. economy.

The hawkish cut

The decision to lower the benchmark rate by 25 basis points was, on the surface, aligned with market consensus. However, the internal dynamics of the vote revealed a central bank at a crossroads. For the first time since 2019, three members dissented, marking the highest level of discord in years. This tripartite division signals that the Fed’s reaction function is no longer unified, complicating the forward guidance that markets rely upon.

Check this to see the whole conference:

Kansas City Fed President Jeffrey Schmid and Chicago Fed President Austan Goolsbee voted to hold rates steady. Their rationale, articulated in post-meeting statements, hinged on the view that inflation remains too hot and the labor market, while cooling, remains historically robust. Schmid explicitly stated that with inflation still above target and the economy showing momentum, policy was not overly restrictive, arguing that a pause was the prudent course to assess the durability of price pressures. Goolsbee, traditionally viewed as a dove, surprised markets by joining the hawkish camp, noting that waiting for post-shutdown data clarity would have been prudent before easing further. This shift from a key dove underscores the anxiety within the Fed regarding the potential re-acceleration of inflation driven by tariffs and fiscal stimulus.

Read more about it here:

The dovish dissent

On the other side of the spectrum, Governor Stephen Miran, a recent Trump appointee, dissented in favor of a larger 50 basis point cut. Miran argued that the labor market is softening faster than headline metrics suggest, citing low hiring rates and potential downward revisions to payrolls as evidence that real rates remain too restrictive for an economy facing headwinds. His dissent serves as a proxy for the incoming administration’s preference for aggressive easing, foreshadowing the potential policy battles to come in 2026.

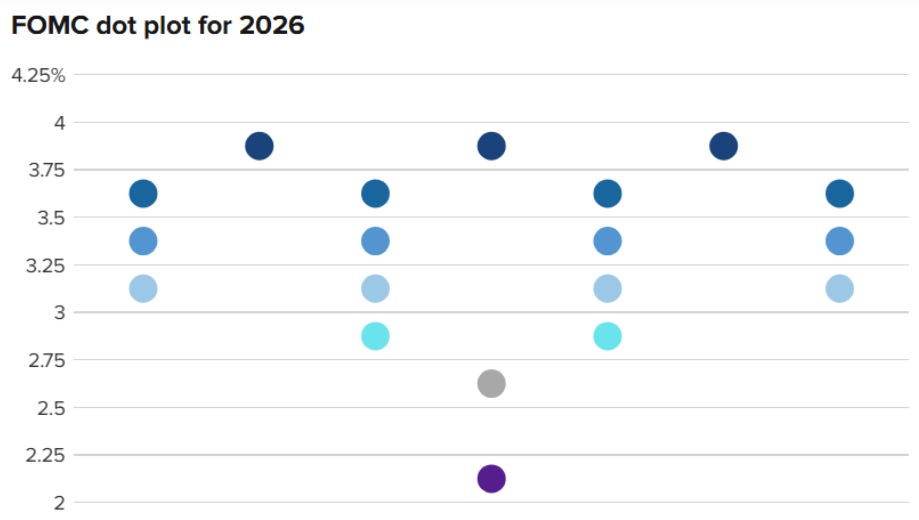

This split—hold, cut 25bps, cut 50bps—indicates that the committee is struggling to interpret conflicting signals. The dot plot reinforced this uncertainty: while the median projection pencils in only one rate cut for the entirety of 2026, seven members projected no further cuts next year. This distribution suggests a significantly higher bar for future easing than the market is currently pricing, creating a setup for volatility if data does not deteriorate rapidly.

While the headline rate cut garnered the majority of media attention, the most consequential policy shift was technical: the announcement of Reserve Management Purchases (RMP). The New York Fed announced it would begin purchasing approximately $40 billion per month in Treasury bills starting December 12, 2025.

Officially, the Fed distinguishes this from Quantitative Easing (QE), framing it as a technical adjustment to maintain ample reserves following the drain of the Reverse Repo Facility and to accommodate trend growth in currency demand. However, market participants recognize the functional equivalence: the Fed is injecting liquidity into the financial system at a rate of roughly $480 billion annualized.

The mechanism of this operation is distinct but the outcome is familiar. By purchasing short-term bills, the Fed suppresses front-end yields and forces private capital that would have held these safe assets to move further out the risk curve or into other asset classes. This action directly addresses the liquidity strain that had begun to appear in repo markets, evidenced by the ticking up of the Secured Overnight Financing Rate. For investors, this liquidity floor puts an implicit put option under risk assets, particularly high-beta technology stocks and cryptocurrencies, even as official rhetoric regarding interest rates remains cautious. It explicitly targets financial stability over strict inflation adherence, a sign that fiscal dominance—where the central bank accommodates government issuance to maintain market function—is beginning to take hold.

Flying blind into Q1 2026

Compounding the difficulty of the Fed’s task is the fact that the U.S. economy enters 2026 in a unique epistemological crisis. The 43-day government shutdown (Oct 1–Nov 12, 2025) surpassed the 2018–2019 record, causing a complete cessation of data collection by the Bureau of Labor Statistics and Bureau of Economic Analysis.

The impact of this data void is structural and lingering. The October jobs report was canceled outright. October CPI data was not collected via standard surveys. November data will be delayed and potentially unreliable due to historically low response rates during the shutdown period. Powell admitted during the press conference that upcoming data releases would be distorted and difficult to interpret, stating, “We will get data but have to be a bit skeptical”.

This forces the Fed into a reactive stance, unable to preemptively manage risks because the dashboard is effectively frozen. The Congressional Budget Office estimates the shutdown shaved ~1.5%-2.0% off Q4 2025 GDP. However, Q1 2026 is expected to see a mechanical snapback of +2.0% to +3.0% as backpay is distributed and spending resumes. This artificial volatility makes distinguishing organic growth from shutdown noise nearly impossible until the second quarter of 2026. For investors, this means the signal-to-noise ratio of economic data will be exceptionally low in Q1, increasing the likelihood of policy errors and market whipsaws.

Tariffs, growth, and inflation

As global financial markets pivot into 2026, the macroeconomic environment is being defined not by a single dominant trend, but by the collision of three tectonic forces that are pulling the United States economy in contradictory directions. Investors are currently at “tug-of-war” economy where the stagflationary impulse of a historic protectionist trade regime is battling against the artificial demand shock of massive fiscal stimulus and the deflationary, yet capital-intensive, productivity boom driven by Artificial Intelligence.

Structural inflationary shift

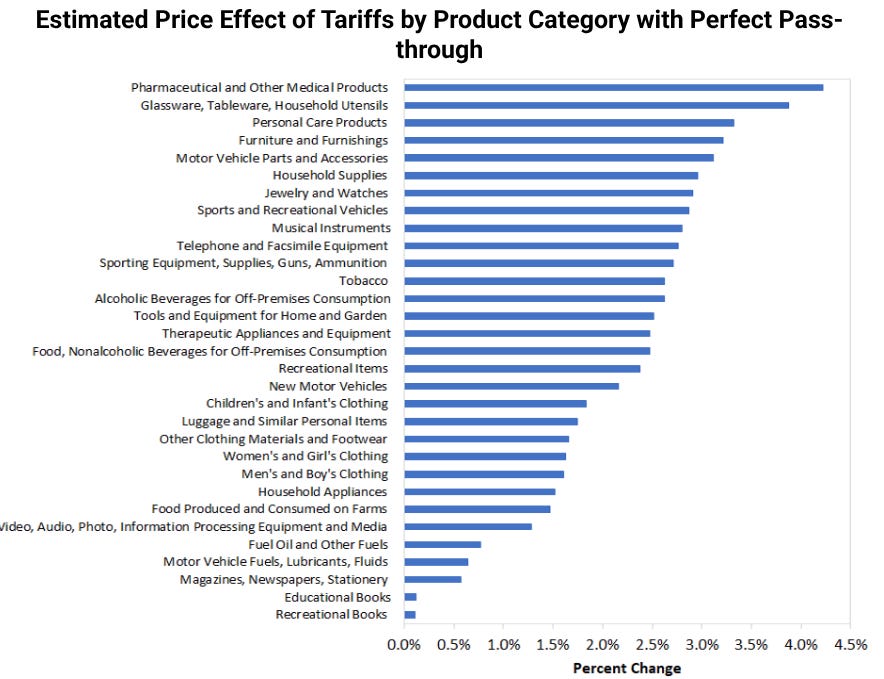

The transformation of United States trade policy from a framework of open global commerce to one of managed reciprocity represents the most significant structural alteration to the global economic order since the 1930s. The implementation of a ten percent universal baseline tariff on all imports, compounded by punitive reciprocal rates on China reaching sixty percent and targeted levies on Mexico and Canada, has moved beyond theoretical risk to become the dominant pricing mechanism in the real economy. Unlike the trade tensions of 2018 and 2019, which were targeted and porous, the universality of the 2025 tariff regime eliminates the ability of importers to substitute goods from non-tariffed jurisdictions, ensuring that the costs are transmitted directly into the domestic price level.

Economic models from the Federal Reserve and private institutions indicate that these measures are exerting an inflationary pressure, estimated to add between fifty and eighty basis points to core inflation throughout 2026. This transmission mechanism is already visible in the reversal of durable goods prices, which have flipped from a deflationary trend in 2024 to a source of renewed inflationary pressure in late 2025. Federal Reserve Chair Jerome Powell explicitly acknowledged this reality in December, noting that goods inflation driven by these trade barriers has become the primary factor keeping aggregate inflation above the central bank’s two percent target. While the Federal Reserve officially characterizes this as a one-time level shift—a temporary adjustment in relative prices rather than a persistent spiral—the risk of second-round effects remains acute. If the increased cost of imported consumption goods, such as electronics, apparel, and automobiles, bleeds into wage demands, this temporary shift could metastasize into a persistent wage-price spiral, particularly given the structural constraints on labor supply due to stricter immigration enforcement.

The corporate response to this new regime has further distorted the economic cycle. Businesses have largely abandoned the efficiency of just-in-time inventory management in favor of just-in-case hoarding, front-running tariff implementation by stockpiling goods. While this activity artificially boosted Gross Domestic Product figures in the third quarter of 2025, it sets the stage for a potential inventory overhang and a subsequent manufacturing slowdown in the first half of 2026 as these stockpiles are drawn down. Furthermore, the specter of asymmetric retaliation from major trading partners remains a looming threat to multinational earnings, creating a fragile equilibrium where U.S. growth is purchased at the cost of global trade friction.

The fiscal offset

Counteracting the drag from trade restrictions is the massive fiscal injection provided by the One Big Beautiful Bill Act (OBBBA), signed into law in July 2025. This legislation acts as a potent fiscal stimulant that complicates the monetary policy outlook. By permanently extending the tax cuts from the 2017 Tax Cuts and Jobs Act and introducing novel deductions—specifically the elimination of federal taxes on tips and overtime pay, as well as the deductibility of auto loan interest for domestically produced vehicles—the OBBBA essentially pumps liquidity directly into the pockets of consumers.

This fiscal expansion creates a unique and dangerous policy conflict where the federal government is simultaneously stepping on the fiscal accelerator via tax cuts while slamming on the trade brake via tariffs. This divergence suggests that nominal GDP growth will likely remain robust even as real GDP growth faces headwinds, a classic symptom of stagflation lite where economic activity is fueled by government deficits rather than organic efficiency. The specific provisions regarding overtime and tips are likely to increase the disposable income of service sector workers, a demographic with a high marginal propensity to consume, thereby supporting demand in the very sectors where inflation has been stickiest. Simultaneously, the auto loan interest deduction serves as a targeted bailout for the domestic auto industry, shielding it partially from the input cost shock of steel and aluminum tariffs, but doing so at the cost of higher structural deficits and interest rates.

The AI productivity paradox and the “jobless expansion”