Table of contents:

Introduction.

De-dollarization and the fiat currency crisis.

Dollar’s waning hegemony.

The sovereign pivot to gold.

The ascent of hard and digital assets.

Gold at $4,000.

Bitcoin at $126,000.

Silver nears generational breakout.

Systemic cracks.

Commercial real sstate implosion.

Subprime auto loan.

Household debt and consumer fragility.

Geopolitical and regional instability.

France.

Argentina.

Investment strategy for Q4 2025.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

October 2025 is defined by a sharp divergence. At the surface, a handful of AI-centric giants keep headline indices aloft. Beneath that veneer, capital is leaking out of fiat claims and into scarce collateral as credit strains turn structural: offices impaired by durable demand shifts and higher cap rates, subprime autos repeating the old securitization script, and households squeezed by reset debt service and bruised real incomes. What looks like strength is, in truth, a mispricing of risk.

Geopolitics has become a financial input. The payment and reserve system is no longer neutral plumbing; sanctions and seizure risk have nudged reserve managers toward diversification. This is not an abrupt “end of the dollar,” but a slow erosion of singular hegemony—a transition toward multipolar reserves and balance sheets re-anchored to what cannot be printed, censored, or frozen. The most conservative players—central banks—have already moved first.

We are early in a hybrid monetary regime that pairs physical scarcity with algorithmic scarcity. Gold and Bitcoin are complements, and their concurrent strength should be read as an institutional signal about trusted collateral, not a speculative coincidence. Equities will remain bifurcated—true productivity compounders can keep compounding—but the next shock transmits through credit: doubts about collateral quality meeting refinancing walls at unhelpful spreads. Policy is constrained by debt and politics; it can smooth losses, not erase them.

More about global debt here:

For Q4 2025 the job is simple, not easy: preserve real purchasing power, avoid credit traps, and keep selective exposure to genuine cash-flow productivity. That argues for a barbell—structural allocations to hard collateral (gold, Bitcoin, with silver as torque) paired with a narrow sleeve of AI-linked cash generators—while keeping duration short, complexity low, and transparency high. We will revise this stance if we see credible fiscal consolidation without growth collapse, a durable and organic decline in term premia, early and transparent loss recognition in CRE/ABS, and a broadening of equity leadership alongside tighter spreads without official backstops. Until then, treat the AI-era euphoria as the surface, the re-collateralization of the system as the substance, and position accordingly.

De-dollarization and the fiat currency crisis

The foundational pillar of the post-war global financial system—the hegemony of the US dollar—is undergoing a structural erosion. This is not a cyclical fluctuation but a secular trend driven by a confluence of geopolitical strategy and a fundamental loss of confidence in the stewardship of fiat currencies. The world’s central banks, the ultimate insiders, are leading a quiet revolution, re-architecting their balance sheets in preparation for a new monetary era.

Dollar’s waning hegemony

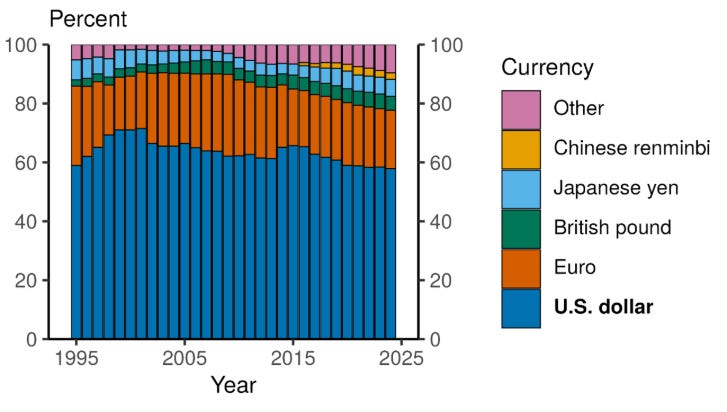

The quantitative evidence of the dollar’s declining role is unambiguous. According to market analysis from October 2025, the US dollar’s share of allocated global foreign exchange reserves has fallen to 56.3%, the lowest level recorded since 1994. This data point is consistent with broader research indicating the dollar’s share stood at 58% at the end of 2024, a significant drop from 65% a decade prior and its peak of 72% in 2001. Projections now suggest this share could fall below the critical 50% threshold within the next five years, marking a definitive end to its unrivaled dominance.

This trend is propelled by two primary factors:

Geopolitical weaponization: The strategic use of the dollar-based financial system to impose sanctions on nations like Russia and China has had the paradoxical effect of accelerating de-dollarization. What was intended as a tool of US foreign policy has been perceived globally as a strategic vulnerability, compelling nations to actively seek non-dollar alternatives for trade settlement and reserve accumulation to ensure their financial sovereignty. The freezing of Russia’s foreign currency reserves served as a watershed moment, demonstrating to reserve managers worldwide that dollar-denominated assets carry significant political risk. Due to this reason, central banks are holding gold as an alternative to foreign exchange reserves.

Gold reserves Erosion of trust and value: The credibility of the dollar as a stable store of value has been severely undermined by domestic policy. Governments in the US and Europe have employed inflationary monetary and fiscal policies to manage immense sovereign debt loads, effectively using inflation as a machine to print poverty. This has resulted in a significant loss of purchasing power for holders of fiat currency, estimated at approximately 30% since 2022. This debasement has forced both foreign central banks and domestic savers to question the long-term viability of holding wealth in a depreciating asset. The decade of US exceptionalism from 2014-2024, which propped up the dollar with strong asset returns, has concluded. Morgan Stanley research confirms the end of a 15-year bull cycle for the dollar in 2024 and forecasts a further 10% depreciation by the end of 2026, driven by slowing US growth and narrowing interest rate differentials with the rest of the world.

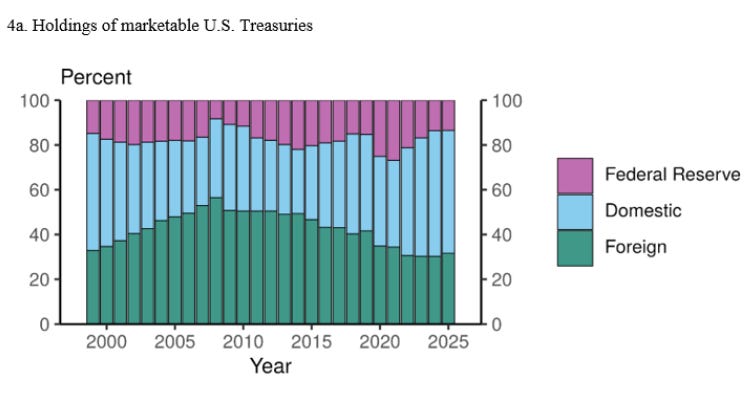

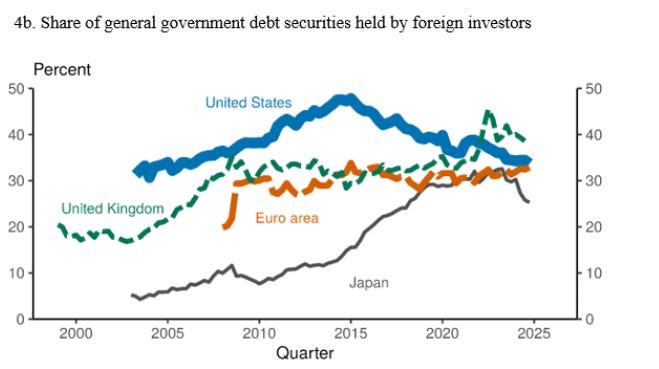

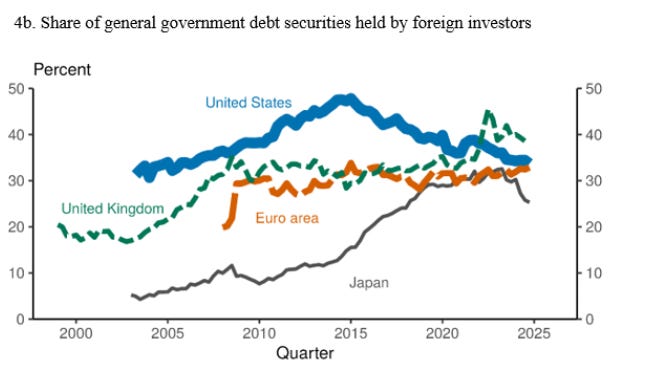

Foreign holdings of government debt

Foreign holdings of government debt

The sovereign pivot to gold

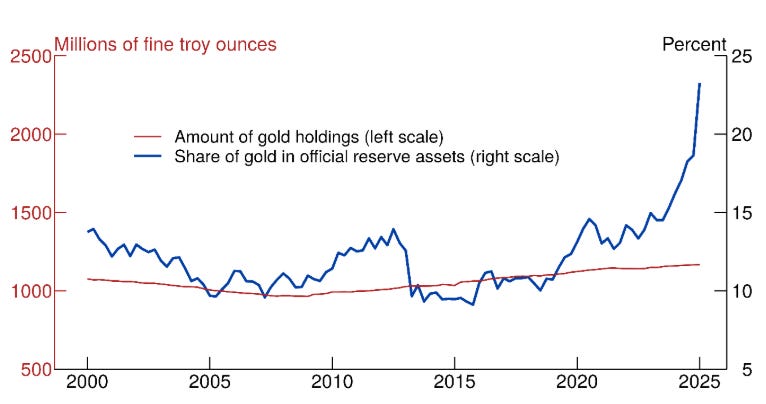

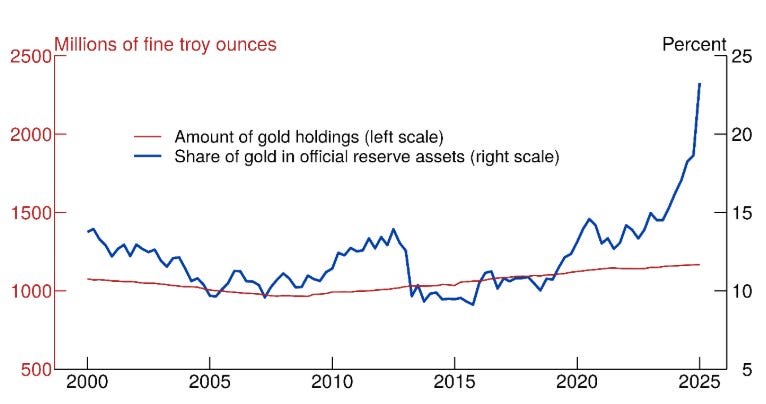

In response to the waning appeal of the dollar, the world’s central banks have initiated a historic pivot toward gold. This is not a short-term tactical allocation but a long-term, secular regime shift in reserve management philosophy. JP Morgan data reveals that gold’s share of global reserves has reached a record 24%, a clear signal of this strategic re-anchoring.

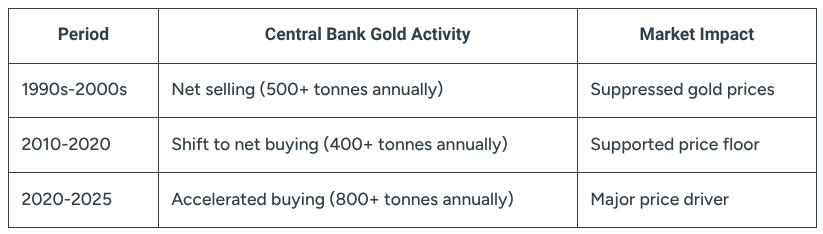

The scale of this accumulation is unprecedented. After decades of being net sellers, central banks have reversed course dramatically. According to the World Gold Council, annual net purchases averaged over 800 tonnes between 2020 and 2024. This intense demand has continued into 2025, with JP Morgan forecasting 900 tonnes of central bank buying for the year. As a result, global official gold reserves have surpassed 36,700 tonnes. The primary actors in this movement are nations seeking to de-risk from the dollar system, with the central banks of China, Poland, and Turkey being among the most aggressive purchasers.

This behavior reveals a critical truth about the current moment. Central banks are not merely diversifying their portfolios; they are actively front-running a looming crisis of confidence in the very fiat system they are tasked with managing. Their actions represent a collective vote of no confidence in the future of unbacked paper currencies, including their own. By systematically swapping depreciating paper assets for a neutral, tangible reserve asset that cannot be devalued or sanctioned by a foreign power, they are sending the most powerful institutional signal an investor can receive: the foundation of the global monetary system is unstable, and a fundamental change is underway.