[INTEL REPORT] Economic easing with China, economic warfare with Russia

Overweight U.S. defense/energy/critical tech

Table of contents:

Introduction.

Economic détente and military escalation.

Russia’s strategic challenge to the west.

The eastern front.

The sanctions regime.

Regional pivots and resource competition.

Argentina.

Europe’s Strategic dilemma.

Synthesis, outlook, and investor revision.

Market implications and forward-looking indicators.

Strategic updates.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

The primary driver of market sentiment in October 2025 has been the announcement of a preliminary trade truce framework between the US and China, established during the ASEAN summit in Kuala Lumpur. This development triggered an immediate and sharp rotation out of safe-haven assets and into riskier equities. Gold, a key barometer of geopolitical fear, experienced a significant sell-off, falling over 3% to below the $4,000 per ounce threshold. This market reaction, however, is tempered by the escalating military and economic pressure campaign being waged against Russia. The imposition of full blocking sanctions on Russia’s largest energy corporations and the EU’s commitment to phase out Russian LNG imports create a structural volatility in global energy markets and ensure that geopolitical risk premiums remain elevated across asset classes.

Based on a comprehensive review of available data, this report presents the following key intelligence judgments:

US-China relations: The Kuala Lumpur Consensus represents a tactical de-escalation, not a strategic rapprochement. It is a pragmatic move by the Trump administration to stabilize markets and address specific domestic economic concerns, such as agricultural exports. The foundational drivers of the rivalry—the contest for technological supremacy, control over critical mineral supply chains, and military primacy in the Indo-Pacific—remain fully intact and will continue to define the relationship long-term.

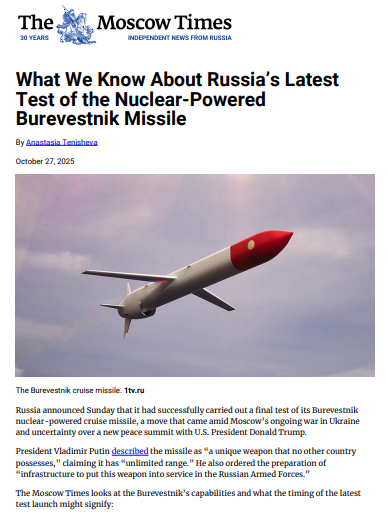

Russia-West relations: The relationship has entered a new and more dangerous phase of confrontation. Russia’s successful test of the Burevestnik nuclear-powered cruise missile is a direct strategic signal designed to negate the multi-trillion-dollar US investment in missile defense and re-establish the credibility of its nuclear deterrent. This military signaling is occurring in parallel with the most punitive US and EU sanctions to date, which for the first time directly target the core of Russia’s energy export revenues. This combination of strategic military posturing and all-out economic warfare indicates a low probability of de-escalation in the near term.

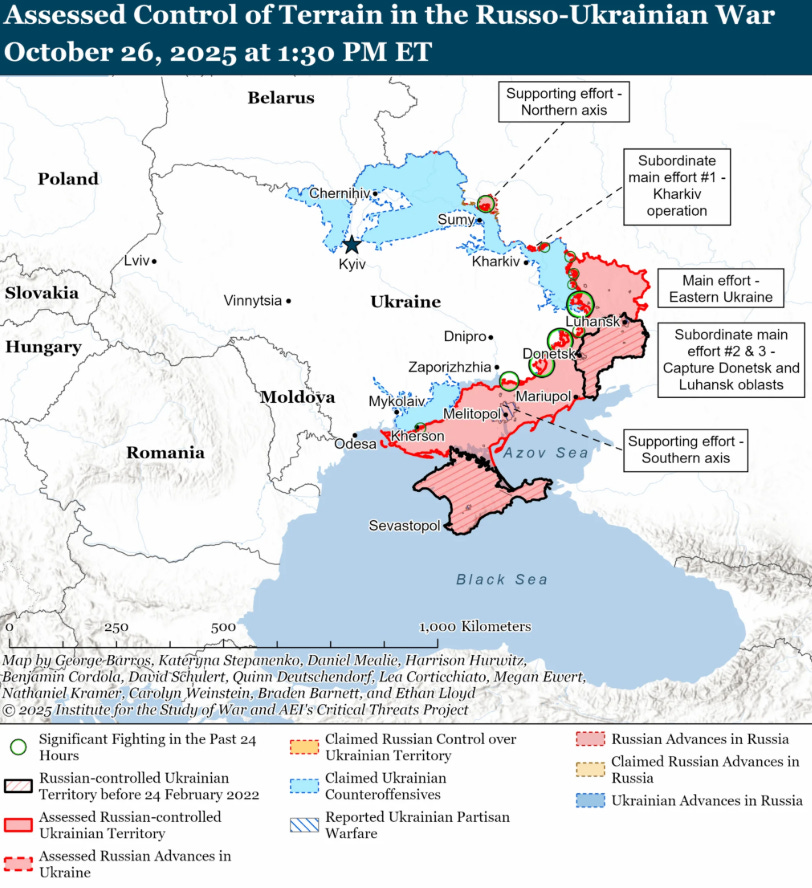

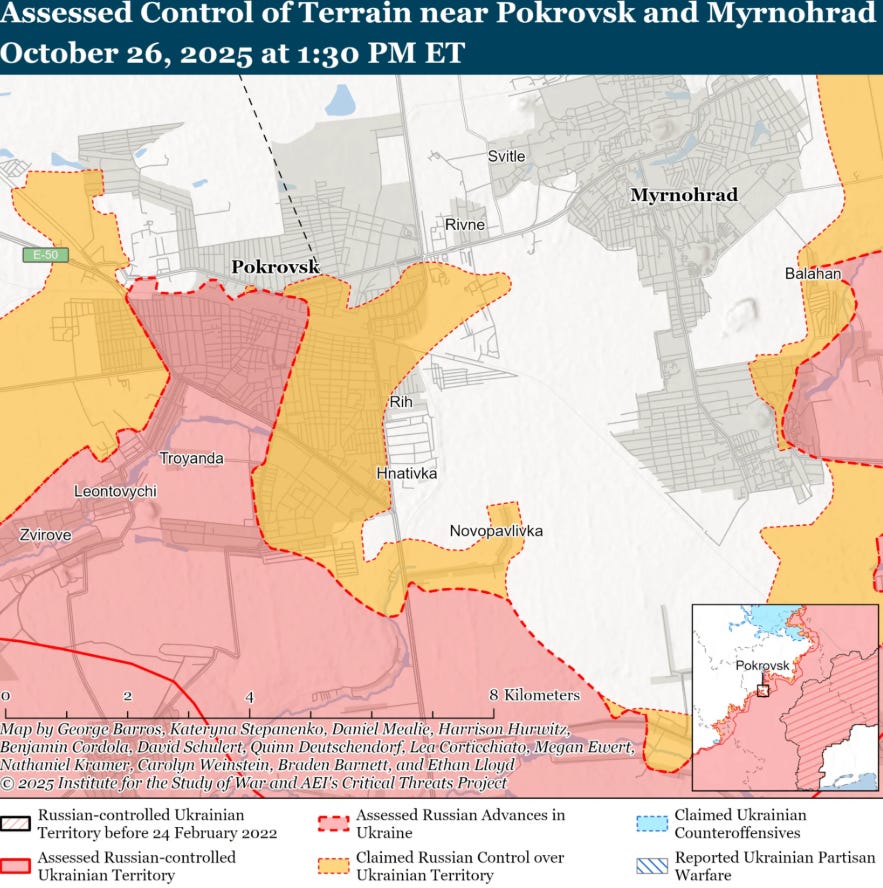

Ukraine war trajectory: The conflict on the eastern front has devolved into a brutal war of attrition. Russian forces are making grinding, high-cost advances in key urban centers like Pokrovsk. Claims from Moscow of major Ukrainian encirclements are part of a broader cognitive warfare campaign designed to project an image of inevitable victory and are not substantiated by available battlefield evidence. The operational reality is one of incremental Russian gains against determined, but severely strained, Ukrainian defenses.

Latin america realignment: The United States is actively and successfully reasserting its influence in the Western Hemisphere. The decisive midterm electoral victory of President Javier Milei in Argentina, directly enabled by a significant US financial support package, represents a major strategic win for Washington. It has effectively halted the BRICS bloc’s expansion into a key South American economy. Concurrently, the heightened US military posture towards Venezuela signals a low tolerance for hostile, resource-rich regimes in America’s traditional sphere of influence, underscoring a strategic prioritization of regional stability and resource security.

More on Russia’s war business:

Economic détente and military escalation

The final week of October 2025 was dominated by a significant, market-moving development in US-China relations. During the Association of Southeast Asian Nations summit in Kuala Lumpur, top economic officials from both nations forged a preliminary consensus on a framework to de-escalate their protracted trade war. This agreement, solidified over the weekend of October 25-26, sets the stage for a high-stakes meeting between US President Donald Trump and Chinese President Xi Jinping in South Korea on October 30.

The core terms of the framework represent a tactical pause in hostilities. The US has agreed to take the threat of imposing 100% tariffs on Chinese imports, scheduled for November 1, effectively off the table. In return, China has committed to deferring its restrictive rare earth export licensing regime for one year and to resume substantial purchases of US agricultural products, particularly soybeans. The framework also addresses ancillary issues such as fentanyl precursor trafficking and the final sale of TikTok’s US operations.

The market reaction to this news was immediate and overwhelmingly positive, confirming the hypersensitivity of investor sentiment to signs of global stability. Global equity markets surged, with futures for the S&P 500 indicating the index was poised to reach new all-time highs on Monday, October 27. This pronounced risk-on sentiment triggered a commensurate flight from safe-haven assets. Gold prices, which had reached a year-high above $4,380 per ounce just days earlier amid rising tensions, plunged precipitously. The precious metal fell over 3% on Monday, breaking decisively below the psychological $4,000 per ounce mark to trade at $3,978, and continued its slide to $3,963 by Tuesday. This rapid repricing of geopolitical risk directly validates the thesis that investors are quick to react to perceived improvements in global economic and political stability.

However, a deeper analysis of the context reveals that this truce is more of a tactical maneuver than a strategic realignment. While financial markets celebrate the pause in tariff escalation, the underlying structural competition between the two powers remains unabated. The language from analysts and official documents continues to emphasize the persistent drive for supply chain resilience and a long-term strategic decoupling in critical technology sectors. Indeed, at the very same ASEAN summit where the truce was announced, the Trump administration was simultaneously signing separate economic frameworks with Malaysia, Cambodia, and Thailand. These agreements are explicitly aimed at increasing trade and cooperation in the sourcing of critical minerals, a clear strategic effort to build alternative supply chains and reduce US reliance on China.

This dual-track approach—engaging in tactical de-escalation with a primary rival while simultaneously pursuing strategic partnerships with regional alternatives—indicates the truce is not an end state but a means to an end. It functions as a carefully calibrated pressure release valve. For the Trump administration, it delivers a short-term market boost and tangible benefits for key domestic constituencies like the agricultural sector. For Beijing, it provides a reprieve from escalating economic pressure. Critically, it buys time for the US to advance its longer-term, more arduous goal of re-orienting critical supply chains away from China. For investors, the key is to differentiate between the short-term market relief, which benefits sectors like consumer goods and global shipping, and the long-term structural risk, which continues to loom over sectors at the heart of the strategic competition, including semiconductors, rare earths, and artificial intelligence.

Russia’s strategic challenge to the west

While markets focused on the economic détente in Asia, a far more ominous strategic signal emanated from Russia. On October 21, Russia conducted a successful full-range test of its 9M730 Burevestnik (NATO designation: SSC-X-9 Skyfall) nuclear-powered cruise missile. According to Russian Chief of the General Staff Valery Gerasimov’s briefing to President Vladimir Putin, the missile flew approximately 14,000 kilometers over a period of 15 hours, validating its core design principles.

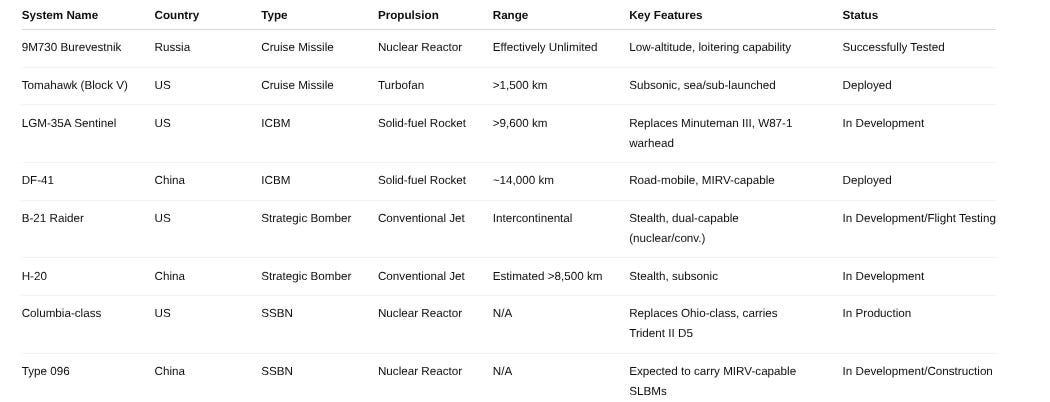

The Burevestnik, first announced by Putin in 2018 as one of Russia’s superweapons, is a strategic game-changer. Unlike conventional cruise missiles like the US Tomahawk, which are limited by fuel to a range of 1,500-2,500 km, the Burevestnik’s miniature nuclear reactor gives it a virtually unlimited range. This allows it to stay airborne for days or even months, loitering in unpredictable patrol patterns before being assigned a target. It is designed to fly at extremely low altitudes—as low as 50 meters—to evade radar detection. Its strategic purpose is unambiguous: it is designed to render the US anti-ballistic missile (ABM) shield, with key installations in Poland, Romania, and Spain, completely useless. The unlimited range allows for attack vectors that bypass traditional North American early-warning systems, such as approaching from the Pacific, the Arctic, or even from behind via the south. This capability is a direct and calculated response to the US withdrawal from the ABM Treaty in the early 2000s, an event Moscow viewed as a fundamental threat to strategic stability.

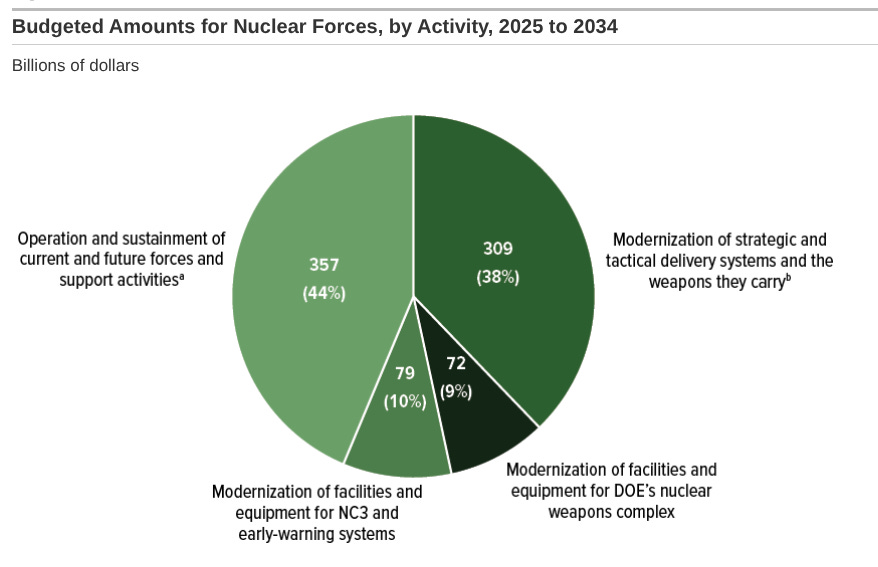

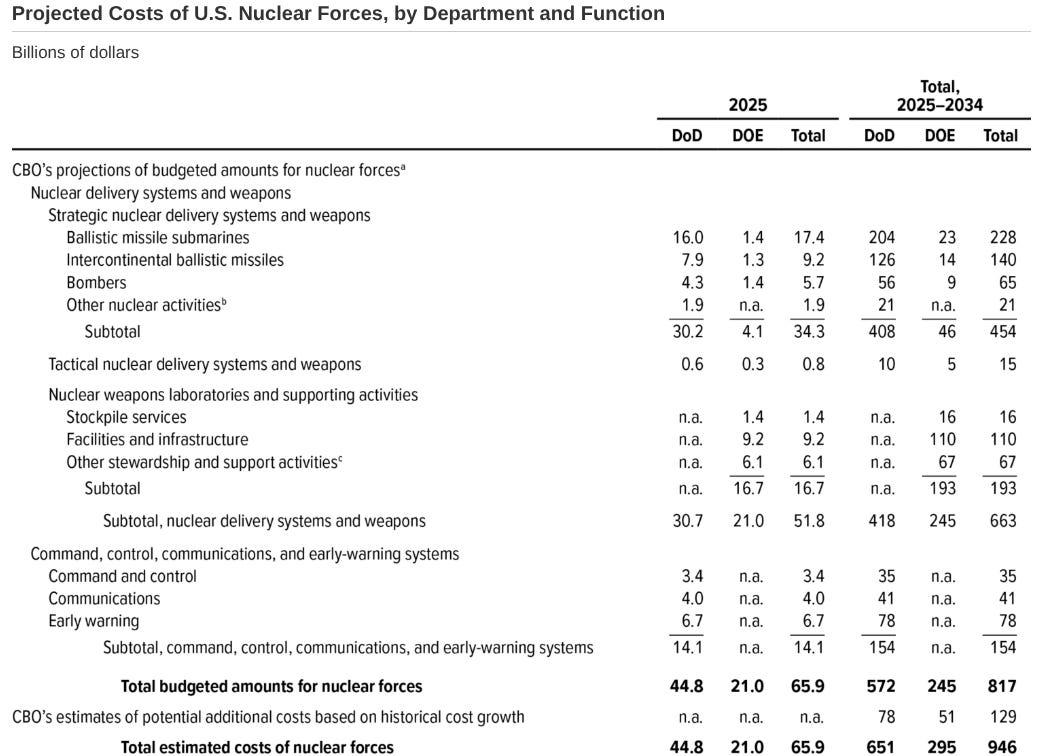

Some analysts have characterized this development, combined with Russia’s lead in hypersonic weapons, as giving Moscow an enormous, brutal technological disadvantage over the United States. This assessment, however, requires critical context. The US is in the midst of the most comprehensive and expensive modernization of its own nuclear triad in history. Programs include the new LGM-35A Sentinel ICBM, the B-21 Raider stealth bomber, and the Columbia-class ballistic missile submarine fleet. The Congressional Budget Office estimated in 2025 that the 10-year cost for operating and modernizing US nuclear forces would be $946 billion, with total lifetime costs projected to exceed $1.5 trillion.

The Burevestnik is therefore not evidence of absolute Russian technological superiority across the board, but rather a strategically brilliant asymmetric counter. It is a relatively cost-effective weapon system designed to surgically neutralize a multi-trillion-dollar US investment in conventional missile defense architecture. By creating a threat that is impossible to intercept with the current system, Russia forces the US to either accept the renewed reality of mutual vulnerability or embark on the prohibitively expensive task of building a 360-degree, low-altitude defense shield. This is a classic asymmetric warfare strategy applied at the highest level of nuclear deterrence, aimed not at out-spending the US, but at negating its primary strategic defense advantage.

The eastern front

The strategic signaling from Moscow is backdropped by a grim reality on the ground in eastern Ukraine. As of late October 2025, Russian forces are concentrating their main offensive effort on the city of Pokrovsk, a vital logistics hub in the Donetsk region. Small Russian infantry units have successfully infiltrated the city, leading to fierce and chaotic street-by-street battles as Ukrainian defenders attempt to locate and eliminate them. Ukrainian President Volodymyr Zelenskyy has described the situation as “difficult,” confirming that Russia has massed its most capable assault forces for this objective. The capture of Pokrovsk, a city with a pre-war population of over 60,000, would represent Russia’s most significant battlefield victory since the fall of Bakhmut in May 2023.

This tactical reality stands in stark contrast to the strategic narrative being projected by the Kremlin. On October 26, General Gerasimov officially reported to President Putin that Russian forces had fully encircled approximately 5,500 Ukrainian troops in the Pokrovsk area and another 5,000 near Kupyansk to the north. However, independent military analysis, including from the Institute for the Study of War, has found no evidence to support Gerasimov’s claims. The frontline is not a solid, contiguous line amenable to classic encirclements, but is instead described as highly porous, with intermingled positions and both sides conducting infiltration missions deep into the other’s rear areas.

The disconnect between Russian strategic messaging and the tactical reality on the ground is a key indicator of Moscow’s broader strategy. The Kremlin is engaged in a sophisticated cognitive warfare campaign designed to project an image of overwhelming success and inevitable victory. This narrative is aimed primarily at an international audience, particularly decision-makers in Western capitals. By creating the impression that the Ukrainian military is on the verge of collapse, Moscow seeks to weaken Western resolve, undermine political support for continued military aid, and create a favorable context for negotiations on its own terms. This information operation, which portrays the West’s only options as either negotiating a de facto surrender or facing a guaranteed losing escalation, is a tool of statecraft as crucial to Moscow’s war effort as the artillery shells being fired in the streets of Pokrovsk.

The sanctions regime

In a powerful demonstration of coordinated policy, the US and EU unleashed their most significant and punitive sanctions against Russia to date in late October 2025. The timing, coming just after the cancellation of a planned Trump-Putin summit in Budapest, lends credence to the thesis that much of the public diplomacy is theatrical representation designed to manage political optics. However, the substance of the sanctions is anything but theatrical.

On October 22, the Trump administration, in its first new Russia-related sanctions action, imposed full blocking sanctions on the country’s two largest oil companies, Rosneft and Lukoil. These measures effectively cut the firms off from the US financial system and, crucially, carry the threat of secondary sanctions against any foreign financial institution that facilitates significant transactions with them, dramatically increasing their global isolation.

A day later, on October 23, the European Union adopted its 19th sanctions package, the most severe yet. The centerpiece of this package is a phased-in but total ban on the import of Russian Liquefied Natural Gas (LNG), with a target completion date of January 1, 2027. This is a major structural blow, as Europe had become a primary market for Russian LNG following the cessation of pipeline gas flows. The package also intensifies the crackdown on Russia’s shadow fleet of oil tankers used to circumvent the G7 price cap, targets Russia’s MIR payment system, and, for the first time, sanctions cryptocurrency platforms and stablecoin developers in third countries (like Paraguay and Kyrgyzstan) that are being used for sanctions evasion.

Check them here: