Table of contents:

Introduction.

The architecture of escalation.

Motif 1: Ultimatum + army + readiness.

Motif 2: Airspace denial as the real constraint.

Motif 3: Europe is choosing a sanctions path.

Motif 4: U.S. governance becomes a market input again.

Motif 5: Energy scarcity as leverage in the Americas.

Motif 6: War remains industrial: drones, grids, heating.

Motif 7: Asia is about patrol tempo + treaty signaling.

What is confirmed in late January 2026.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

Here’s the uncomfortable truth: you can’t read it headline by headline anymore. The signal is in the way events fit together. In geopolitics, the market-relevant details are often boring on purpose: a routing constraint, a sanctions trajectory, an enforcement memo, a posture shift, a logistics denial. They read like bureaucracy, but each one changes the friction in the system.

The real danger is the accumulation of constraints that make miscalculation more likely. Constraints reshape risk. They can make deliberate escalation harder while making accidents more likely, simply because actors operate with less slack. Detours add steps. Steps add failure points. Failure points increase the chance of misreads, probing, brinkmanship, and asymmetric responses that sit below the threshold of war but above the threshold of irrelevant. That’s how you get the defining pattern of a constraint regime: spot markets can look orderly while hedges stay expensive.

Sanctions work the same way. The market impact isn’t limited to the sanctioned party’s direct exposure. It spreads through the plumbing—documentation, payment rails, due diligence, shipping paperwork, correspondent banking behavior, insurer risk appetite. Even before every rule is enforced, the direction of travel changes private behavior. Firms and intermediaries start pricing the risk of being on the wrong side of tomorrow’s interpretation.

When several constraints tighten in the same window, the effects compound. Multiple theaters begin to hit the same transmission channels—shipping, insurance, enforcement, fiscal sequencing—so correlation rises for reasons that have nothing to do with fundamentals.

The architecture of escalation

Escalation is usually narrated as a sequence of events: a statement, a strike, a retaliation. But it is a engineered shape of decision-making: what can move, what cannot, what must route around a constraint, and what becomes legible enough to model. That legibility is the key transmission mechanism where each motif is a repeatable building block. Taken alone, each looks local; together, they describe a scenario rotating toward constraint-driven pricing.

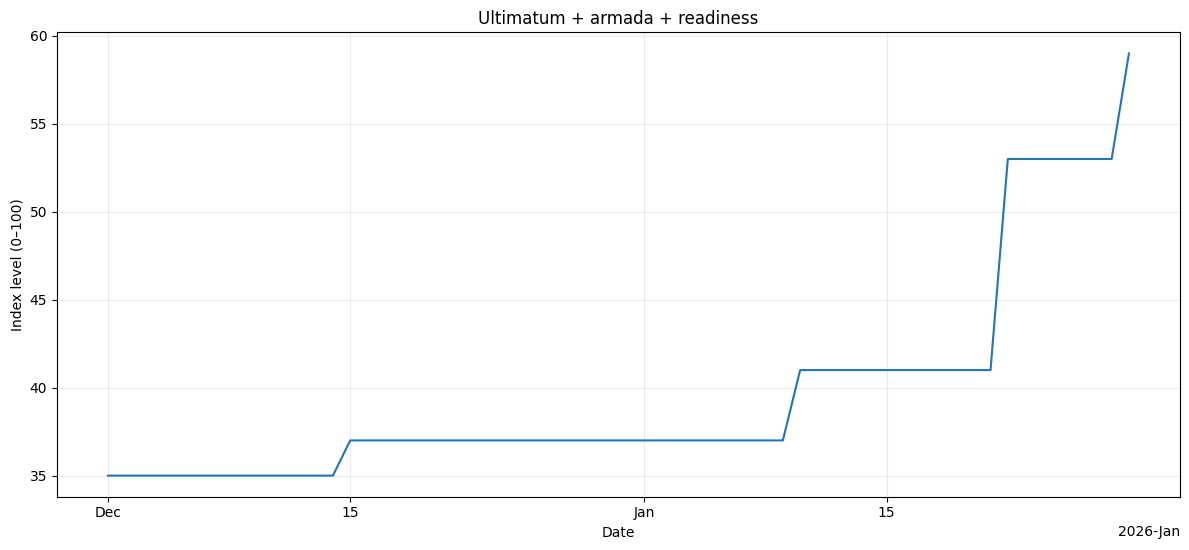

Motif 1: Ultimatum + army + readiness

Iran’s posture of immediate readiness to respond by land, air, and sea presents the American posture as a naval force prepared for speed and violence, with the aircraft carrier USS Abraham Lincoln elevated to a symbol rather than a mere asset. This detail is important because markets don’t value symbols as they value inventories. Symbols compress time. They turn maybe later into could be soon, which is what increases the cost of being wrong.

Multiple reports described President Trump using the language of war and explicitly linking the posture to the USS Abraham Lincoln and accompanying destroyers moving into the region. The central move is to fuse that war language with Iran’s readiness claim into a single decision-loop: action, response, and the promise of a larger follow-through if the first strike is limited.

For investors, the immediate trade is often misunderstood. The largest early repricing does not require missiles landing. Iters and shippers to believe the probability of disruption has changed. Indeed, insurance is a probability business. When political signaling becomes operationally legible the market channel that moves first tends to be risk transfer: war-risk premia, marine insurance riders, freight spreads, and the volatility surface of energy and transportation equities. A carrier is a mechanism that makes tail risk financeable, because it gives counterparties something concrete to model.

Notice that all of this does not stay on Iran. It pivots into other theatres. That pivot is the tell. The story is not Iran as a one-off. The story is the world is back to pricing corridor disruption as a generalized condition.

We’re going to show you a sequence of plots that, after seeing a couple of them, will help you understand the whole picture.

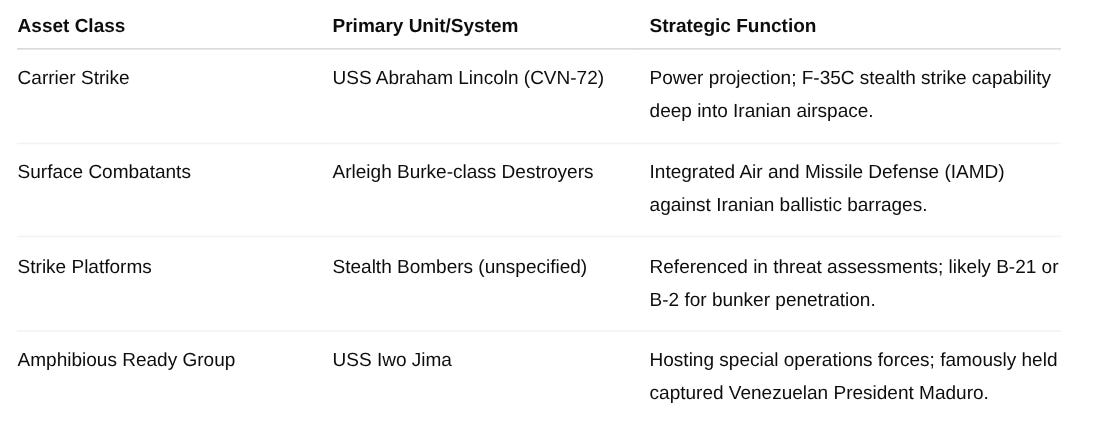

The deployment is centered on the USS Abraham Lincoln Carrier Strike Group:

The presence of the USS Iwo Jima is symbolic and operationally significant. Having served as the holding facility for Nicolás Maduro following his capture earlier in the month, its deployment to the Gulf signals that the Venezuela Model—decapitation strikes against leadership—is on the table for Iran. Trump explicitly compared the two, noting the armada facing Iran is Bigger than Venezuela.

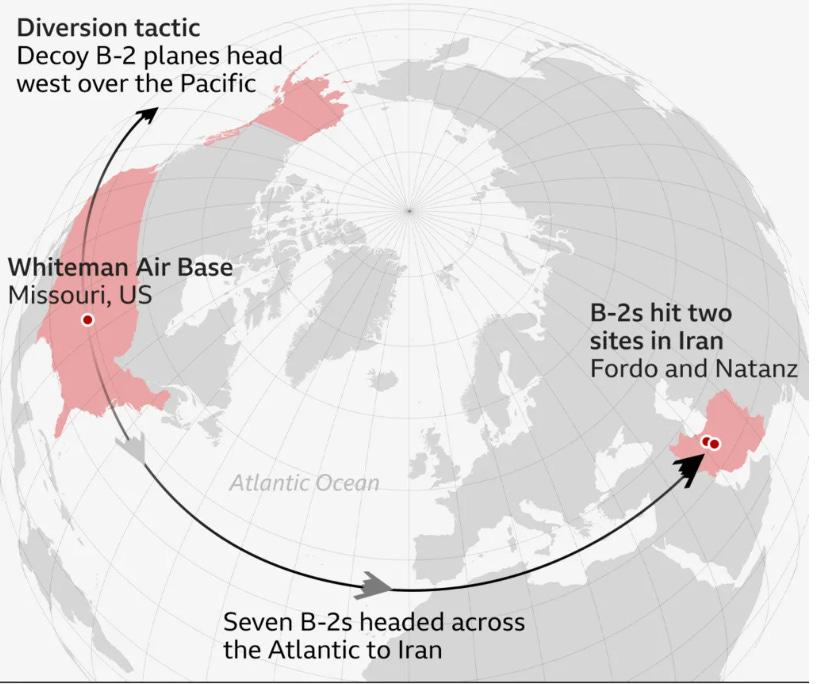

The credibility of this force is underpinned by Operation Midnight Hammer, a recent military action described by the President as a warning shot. While specific operational details remain classified, the invocation of this operation suggests that the threshold for kinetic engagement has already been crossed. The administration is signaling that it has moved beyond red lines to active measures.

Despite the martial posturing, a diplomatic track remains open, albeit narrow. Iranian Foreign Minister Abbas Araghchi is scheduled to hold talks in Turkiye. The U.S. administration has defined a strict two-week decision window to observe the Iranian response to the ultimatum. This timeline creates a period of volatility; any miscalculation by Iranian naval forces or proxy groups during this window could trigger the US army to fulfill its missions with speed and violence.

The Iranian regime faces a dilemma: capitulation on nuclear enrichment would be a humiliating retreat for Supreme Leader Ali Khamenei, endangering the regime’s domestic legitimacy amidst ongoing protests. Conversely, rebuffing the demand risks a strike that could destabilize the government entirely. The U.S. bet is that the regime’s survival instinct will force it to the table, but the rigid timeline increases the risk of accidental war.

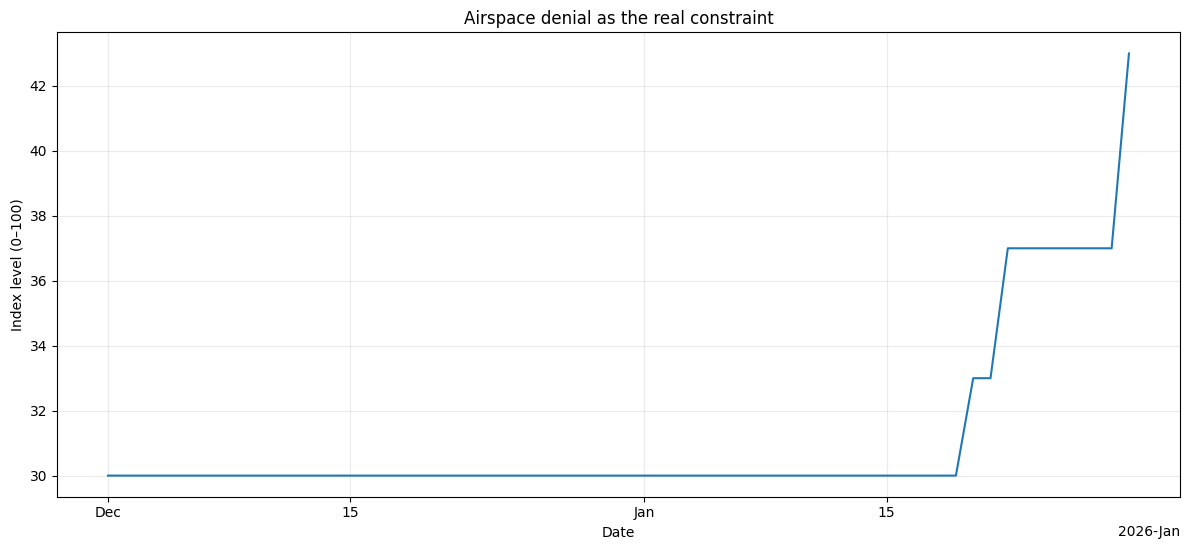

Motif 2: Airspace denial as the real constraint

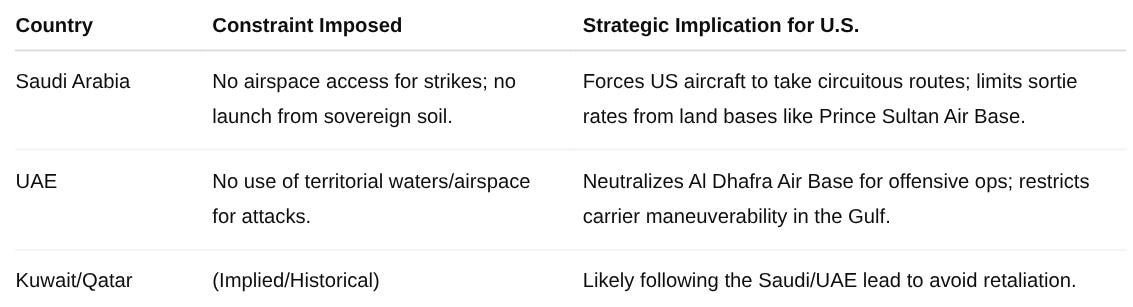

Saudi Crown Prince Mohammed bin Salman told Iran’s president that Saudi Arabia will not allow its airspace or territory to be used for military action against Iran. This is the kind of detail that sounds diplomatic, but trades like logistics.

Airspace is the hidden scaffolding of escalatial state signals denial, it changes routing, refueling geometry, the set of feasible strike paths, and the number of steps required to execute a plan. Operational complexity is not a moral category; it is a probability category. More steps means more chances to abort, miscalculate, leak, or be deterred.

This denial is driven by a rational calculation of vulnerability. Saudi Arabia and the UAE are the glass houses of the region—their economies rely on vulnerable oil infrastructure and futuristic cities (Neom, Dubai) that are within minutes of Iranian missile flight times. The detente initiated between Riyadh and Tehran (brokered by China) has prioritized regional stability over U.S. security objectives. MBS’s affirmation of support for dialogue indicates that the Gulf states are choosing to manage Iran rather than defeat it.

The denial of airspace fundamentally alters the operational perspective of any U.S. strike.

Maritime dependence: The U.S. must rely almost exclusively on carrier-based aviation launching from international waters in the Gulf of Oman or the Arabian Sea, rather than land-based tactical air.

Routing complexity: To reach targets in northern or central Iran without crossing Saudi or Emirati airspace, U.S. assets must fly through Iraq (politically sensitive) or rely on long-range standoff munitions (Tomahawks) that do not require overflight permissions for pilots.

Diplomatic isolation: The U.S. is isolated operationally. By refusing to participate, the Gulf states strip any potential conflict of regional coalition legitimacy, framing it strictly as a U.S.-Iran bilateral war.

The sovereign constraints on U.S. power projection can be summarized as:

From an investment point of view, airspace denial is one of the clearest examples of how politics translates into convexity. Constraints can lower the probability of deliberate escalation while simultaneously increasing the probability of incidents (misreads, brinkmanship, probing flights, asymmetric responses) because actors operate in tighter corridors with less slack. That is why this signal can support a regime where spot markets look calm, while option markets remain bid: uncertainty is not eliminated but reshaped.

In practical portfolio terms, this motif matters most for exposures that depend on routing: air freight, certain energy-linked shipping lanes, and any supply chain whose cost base is sensitive to detours and insurance terms. Even if you are not trading these directly, they feed into headline inflation volatility and therefore into rate volatility.

This motif underscores that while the U.S. retains overwhelming global power, its local power is subject to the veto of its partners. The real constraint on the architecture of escalation is Arab neutrality.

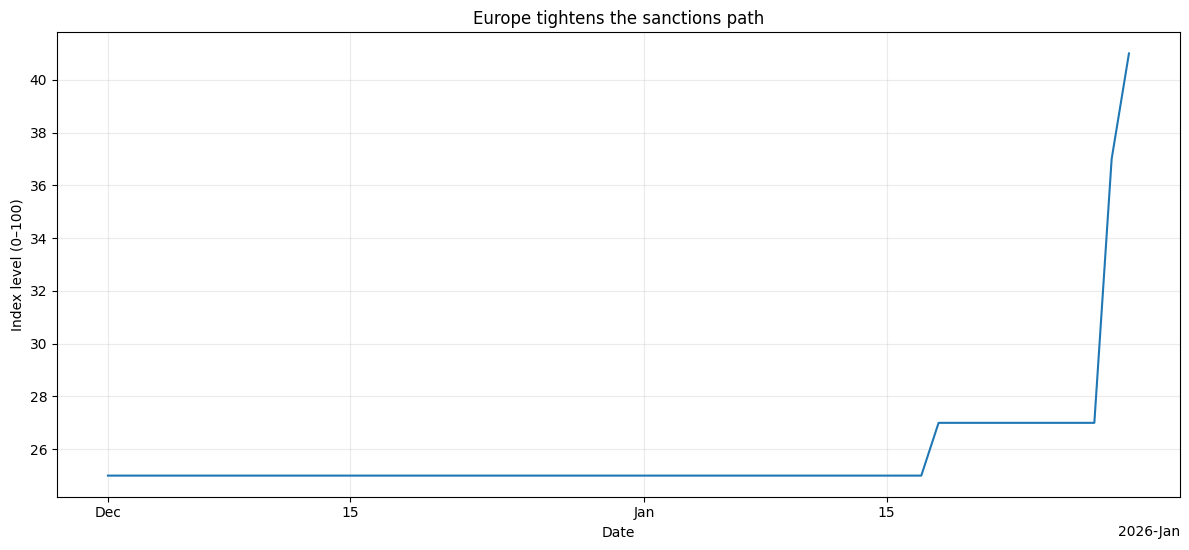

Motif 3: Europe is choosing a sanctions path.

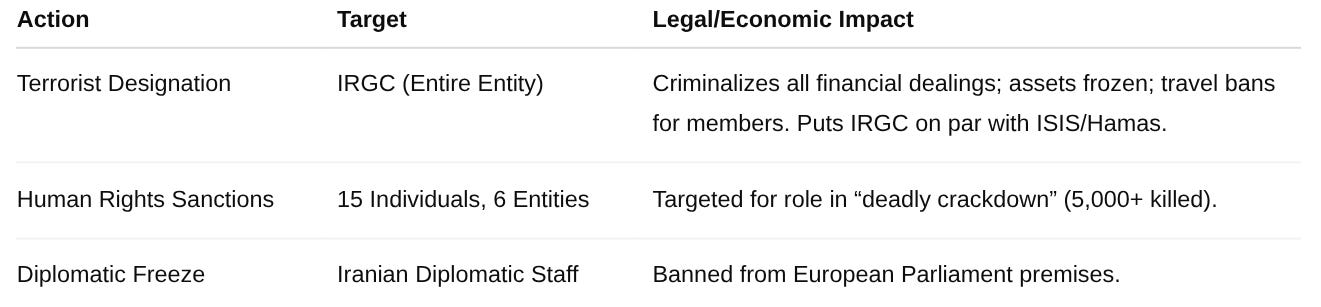

France and European leaders are moving toward sanctions related to Iranian repression and intensifying pressure on the IRGC. The EU moved toward designating Iran’s Revolutionary Guard as a terrorist organizn France’s position, alongside approval of new sanctions targeting individuals and entities linked to protest suppression and support to Russia.

For positioning, the critical insight is that sanctions regimes do not reprice markets only through the sanctioned entity’s direct exposure. They reprice through: documentation, payment rails, due diligence, shipping paperwork, correspondent banking behavior, and the risk appetite of insurers and freight forwarders. Even if the sanction list is not yet operationalized in every legal sense, the trajectory itself shifts behavior, because private actors price the risk of being caught on the wrong side of tomorrow’s rule.

That is why you can see a sanctions tightening as a kind of tax on frictionless globalization. It just needs to make trade slower, more expensive, and more legally conditional. For investors, that tends to express through wider dispersion within Europe—firms with clean supply chains and robust compliance cultures gain relative advantage—and through higher premia for EM assets that depend on cross-border capital confidence.

This matters because it places Europe’s sanctions momentum alongside Middle East escalation risk. That pairing is not accidental. Sanctions are a second channel of escalation. When military geometry is constrained, policy geometry often tightens instead. Markets price that as a regime shift toward persistent friction, which is a different macro environment than 2010s smooth trade assumptions.

The sanctions path complements the U.S. strategy by closing the economic escape valves for Tehran.

Economic strangulation: The IRGC controls vast swathes of the Iranian economy (construction, energy, telecommunications). Designating it as a terrorist organization makes it legally perilous for any European bank or corporation to engage in any significant commerce with Iran, creating a de facto total embargo.

Transatlantic unity: This moves Europe into alignment with the U.S. maximum pressure campaign. While Europe is not sending ships, it is weaponizing its financial system.

Diplomatic rupture: The designation likely ends any hope of reviving the nuclear deal. Iran has consistently stated that the IRGC designation is a red line. By crossing it, Europe is accepting that the diplomatic era is over and the containment era has begun.

The EU’s sanctions architecture:

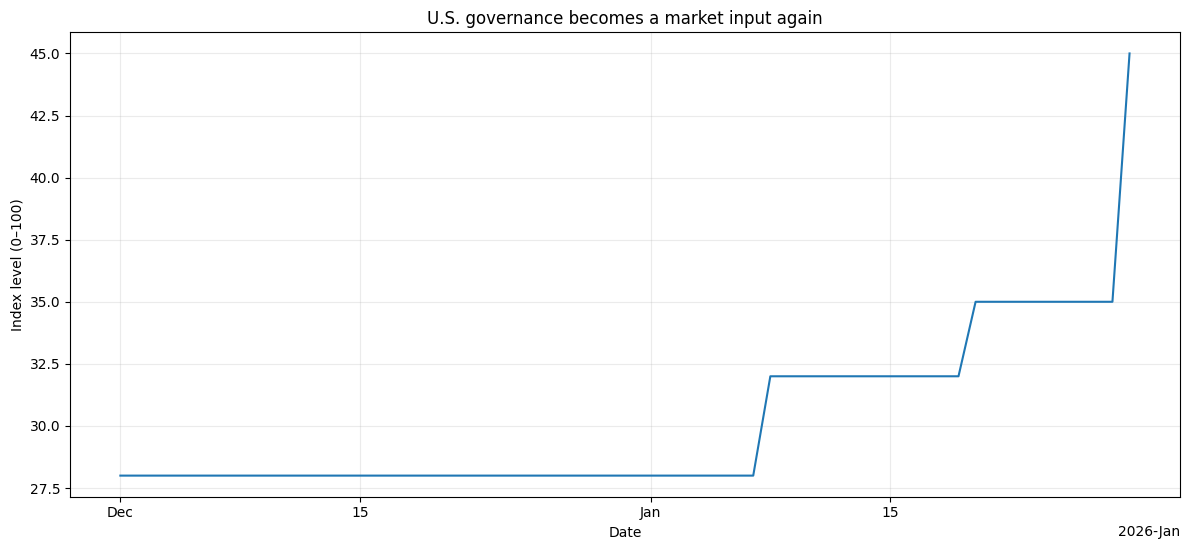

Motif 4: U.S. governance becomes a market input again.

A potential partial U.S. government shutdown tied to DHS funding, politically amplified by the Minnesota shooting case and subsequent operational guidance to ICE about avoiding agitators. Now there are new orders instructing ICE officers in Minnesota not to interact with agitators, reflecting operational shifts amid public tension. At the same time, the renewed shutdown risk around a January 30 funding deadline and the political dynamics that could push the U.S. toward a partial shutdown:

The killing of Alex Pretti, a 37-year-old VA nurse, by Border Patrol agents on January 24 became a national symbol of excessive force.

Minneapolis saw protests of 50,000 people, creating a domestic security crisis that mirrored the international tensions.

The funding lapse affects key agencies including DHS, Transportation, and Labor. This creates operational friction; the very agencies needed to secure the homeland during a potential war with Iran are operating without funding.

Besides, the governance crisis was compounded by a contentious Federal Reserve meeting on January 28, 2026. The Fed chose to hold interest rates steady, marking a strategic pause in its easing cycle.

The dissent by Governors Miran and Waller highlights a central bank unsure of the terrain. The sticky inflation combined with social unrest creates a stagflationary risk profile. Markets reacted with a focus on governance risk—the idea that the U.S. political system is becoming too dysfunctional to manage its economic policy effectively.

The shutdown and the Fed pause create a feedback loop that weakens the U.S. global posture.

It is difficult to project competence abroad (e.g., in the South China Sea) when the federal government is closed and citizens are being shot by agents at home.

The shutdown complicates the logistics of military funding and aid distribution.

Rivals like Iran and Russia may calculate that a U.S. president facing domestic turmoil is either distracted (opportunity) or desperate (danger), adding volatility to their decision-making.

The investment meaning is that the United States remains both the world’s anchor for risk-free discounting and one of the world’s largest sources of policy impulses. When governance volatility rises, global term premia tend to rise—not necessarily because investors fear default tomorrow, but because investors price the possibility of policy discontinuity across immigration enforcement, trade, defense posture, sanctions enforcement, and fiscal sequencing.

This is especially effective in how it frames this: it treats U.S. politics as local, a variable that interacts with every other motif. If you are pricing Middle East escalation, sanctions enforcement, energy corridor coercion, and China-adjacent trade policy, then U.S. governance volatility becomes correlation fuel. In that regime, diversification can fail: assets that are normally uncorrelated begin reacting to the same policy headlines because the marginal buyer’s constraint becomes political uncertainty rather than fundamentals.

Motif 5: Energy scarcity as leverage in the Americas.