[INTEL REPORT] The Gulf war’s economic front

How a regional conflict moved into oil flows, inflation, trade routes, and sovereign risk across the world economy

Table of contents:

Introduction.

Escalation of war in the Gulf.

Hormuz as the strategic hinge.

Kharg island is the energy chokepoint.

Energy shock and the macro transmission channel.

Second-order economic effect of war.

Egypt external war pressure.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

The Gulf war now sits at the center of the global economic system. What once looked like a regional military confrontation now shapes the price of oil, the cost of maritime insurance, the movement of LNG, the availability of fertilizers, the outlook for inflation, and the fiscal stability of import-dependent states. The conflict has crossed the boundary between battlefield dynamics and macroeconomic reality. Every strike on infrastructure, every disruption in transit, and every shift in force posture now feeds directly into trade flows, industrial costs, sovereign risk, and household pressure across regions far from the Gulf.

At the center of that system stands the Strait of Hormuz. This narrow maritime corridor connects armed confrontation with global energy supply in a direct and immediate way. It is the hinge between missiles and inflation, between naval pressure and industrial costs, between regional violence and worldwide repricing across oil, gas, freight, food, and sovereign debt. Around it, Kharg Island emerges as a second critical node, a concentrated export point whose strategic value lies in its ability to convert Iranian production into global market pressure and fiscal survival.

What follows traces that chain with a clear line of sight. It begins with the expansion of war across the Gulf export system and then moves through Hormuz as the decisive chokepoint where military risk becomes macroeconomic shock. From there, the focus shifts to Kharg Island and the wider energy channel, where the conflict enters inflation, trade, growth, and monetary policy. The later sections turn to the deeper economic consequences of prolonged confrontation, including alliance strain, defence spending, fiscal burdens, and the exposure of vulnerable import-dependent economies such as Egypt.

You can go deeper by checking this report:

This moment also carries a strategic message for markets and states alike. The most important risks sit in the infrastructure that keeps economies supplied, in the narrow corridors that keep trade alive and domestic stability. Once those channels come under pressure, the effects spread with speed from ports to prices, from commodities to currencies, and from regional confrontation to global adjustment.

Escalation of war in the Gulf

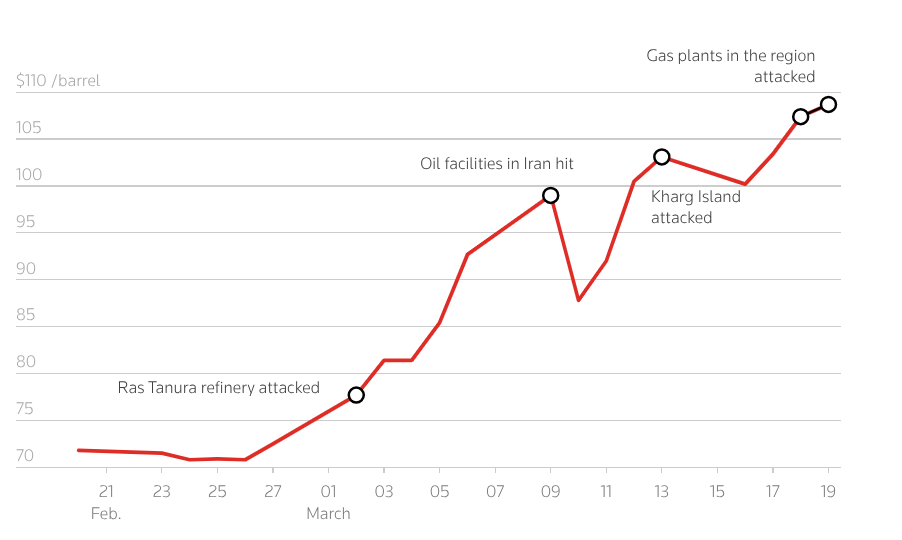

The war now sits inside the core of the global economy. The opening phase concentrated on Iranian leadership nodes, missile capacity, nuclear assets, and military infrastructure. The present phase covers the Gulf export system, maritime transit, shipping insurance, alliance bargaining, and market pricing across oil, gas, freight, food, and sovereign risk. Attacks hit major oil and gas sites across Iran, Saudi Arabia, Kuwait, Qatar, the United Arab Emirates, Bahrain, and Iraq. Bahrain declared force majeure after damage at the Sitra refinery, Iraq cut output as Hormuz disruption blocked crude flows, and Qatar reported the loss of around one-sixth of LNG capacity after damage to Ras Laffan. That sequence transformed the conflict into a regional energy and trade shock with global reach.

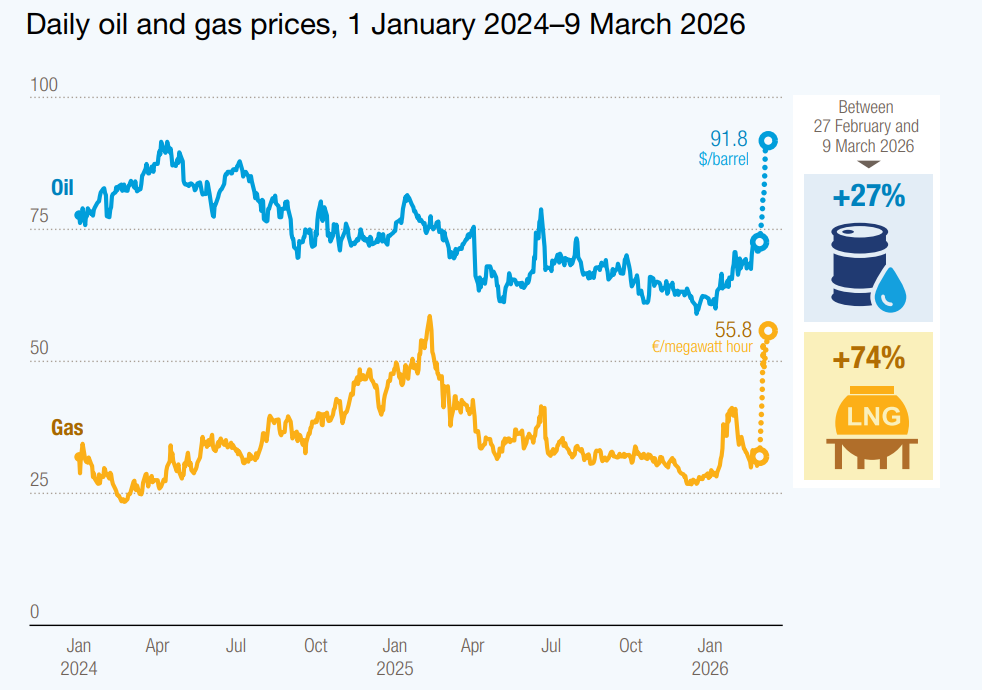

Persian Gulf oil shipments has lifted energy prices. Its adjusted high-energy scenario lowers 2026 world merchandise trade volume growth to 1.4% from 1.9% and trims global GDP growth to 2.5% from 2.8%. The IMF added that a persistent 10% increase in oil prices can raise global headline inflation by around 40 basis points and reduce global output by 0.1 to 0.2 percentage points. Together, those estimates show that the conflict now acts through the central channels of inflation, trade, and growth rather than through a narrow regional risk premium.

The Strait of Hormuz sits at the center of this transmission mechanism. UNCTAD estimated that the strait carries around one quarter of global seaborne oil trade along with major LNG and fertilizer flows. Its briefing shows ship transits through the strait falling by 97% from the February average, while oil and gas prices surged between 27 February and 9 March. In that setting, Hormuz becomes the hinge that connects military escalation with industrial input costs, European gas pricing, Asian energy security, fertilizer markets, freight rates, bunker fuel, and food pressure across import-dependent economies.

Washington is sending thousands of additional Marines and sailors to the region, adding to an existing U.S. military presence of about 50,000 personnel. At the same time, the White House has pressed allies to help secure passage through Hormuz, while European partners have adopted a posture centered on safe passage, inflation control, and de-escalation. This combination places deterrence, burden sharing, maritime security, and macro stabilization inside the same strategic field.

Outside powers have entered the same equation. China warned that the war threatens global energy supplies, trade routes, and economic stability. Russia declared political support for Tehran through a Kremlin message that described Russia as a loyal friend and reliable partner. These positions matter because they influence shipping expectations, sanctions politics, commodity diplomacy, and the pricing of geopolitical persistence across global markets.

Financial transmission has also accelerated. A U.S.-backed maritime reinsurance plan led by Chubb seeks to restore commercial shipping through Hormuz, which shows how finance and logistics now function as strategic infrastructure alongside naval and air power. UNCTAD’s assessment also tracks sharp rises in tanker costs, bunker fuel, and bond yields across exposed Gulf economies, confirming that the shock now moves through transport costs, refinancing conditions, and imported inflation as well as through crude and LNG benchmarks.

The confrontation therefore belongs to the category of wider-system conflict. Geography, energy, trade, shipping, insurance, alliance politics, inflation, and growth forecasts now move inside one connected field. Each strike on infrastructure or transit routes now feeds into industrial costs, consumer prices, sovereign funding conditions, and policy choices across regions far from the battlefield.

By the way, before we move to next section, a new TACO just happned today because of:

Hormuz as the strategic hinge

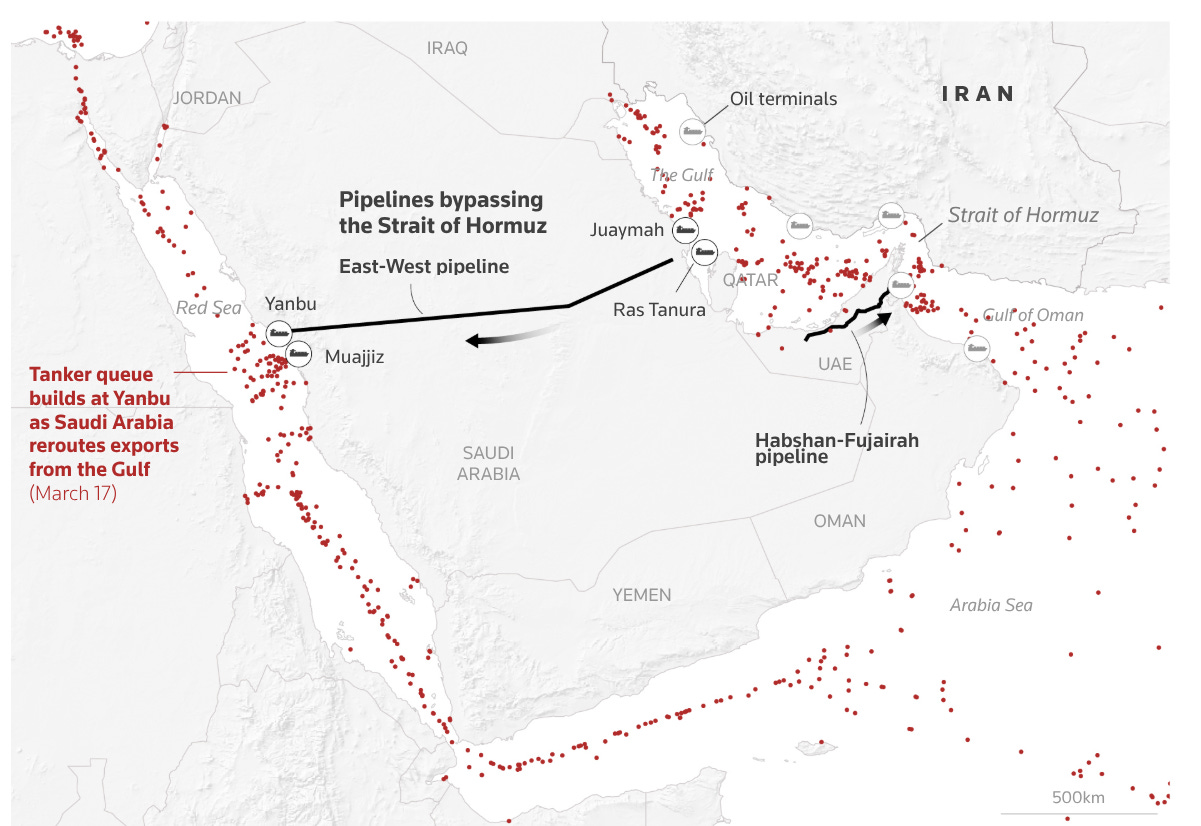

The closure of the strait has stopped the passage of about 20% of the world’s oil and liquefied natural gas since 28 February. The International Maritime Organization said around 20,000 seafarers on nearly 2,000 ships west of the strait are caught in the disruption, and Iraq has already declared force majeure because Hormuz disruption halted most crude exports and cut Basra output from 3.3 million barrels per day to 900,000. The narrow channel now links missile risk and naval pressure with global energy supply, shipping capacity, and state revenue.

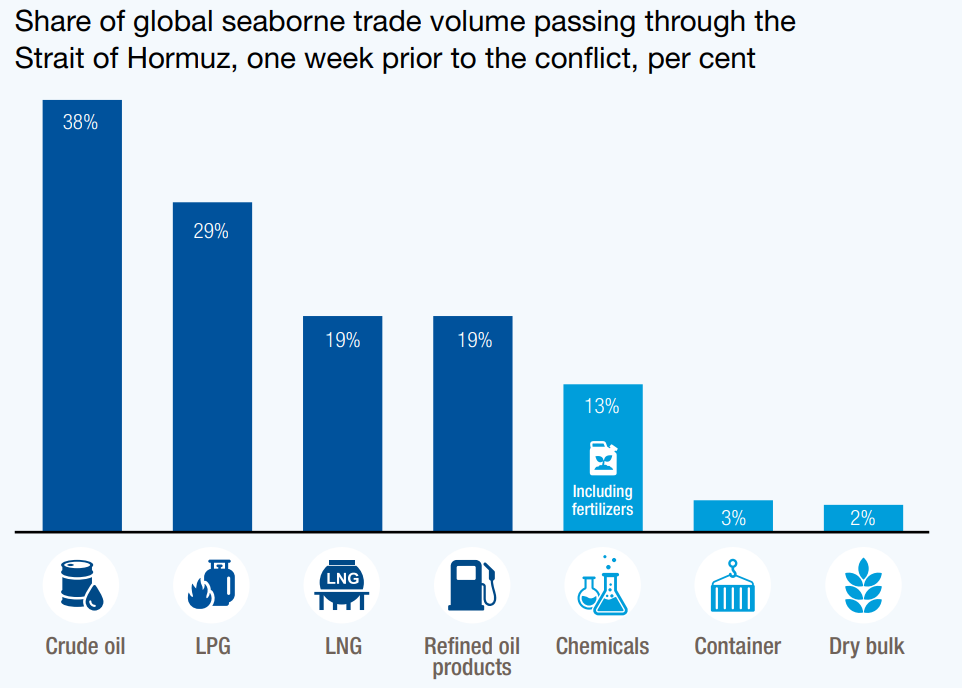

The U.S. Energy Information Administration reported that Hormuz carried about 20 million barrels per day in 2024, equal to about 20% of global petroleum liquids consumption and more than one-quarter of seaborne oil trade. Around one-fifth of global LNG trade also moved through the strait. EIA estimated bypass capacity in Saudi and Emirati pipelines at about 2.6 million barrels per day, so rerouting covers only a small share of the volume at risk. UNCTAD’s adds that, one week before the conflict, crude oil represented 38% of the relevant seaborne trade categories moving through Hormuz, LPG 29%, LNG 19%, refined oil products 19%, and chemicals, including fertilizers, 13%. Asia receives 84% of Hormuz crude and 83% of Hormuz LNG, which gives the chokepoint immediate reach across the main import centers of the global economy.

Traffic data show how fast military pressure becomes market shock. UNCTAD recorded an average of 141 daily ship transits during 1–27 February, followed by a 97% collapse. Brent had risen 27% and Dutch TTF gas 74% from then. Chubb joined a $20 billion maritime reinsurance plan because shipowners, cargo interests, and financiers need war-risk cover before normal commercial flows can return. Passage through Hormuz therefore sets the marginal cost of energy movement, insurance, and cargo finance for economies far beyond the Gulf.

The macroeconomic spillover now reaches trade volumes, food costs, inflation expectations, and sovereign financing. Severe curtailment of Persian Gulf oil shipments could cut world merchandise trade volume growth in 2026 to 1.4% from 1.9% and lower world GDP growth to 2.5% from 2.8% under its high-energy-price scenario. This connects higher Gulf energy prices with fertilizer stress and broader food-system pressure. Besides, government bond yields in the United States and Europe jumped as investors priced a more persistent inflation shock, with the UK 10-year yield rising above 5% and markets shifting from rate-cut expectations toward rate-hike expectations. Hormuz therefore acts through central-bank reaction functions and sovereign borrowing costs as well as through the oil curve.

Kharg island is the energy chokepoint

Kharg Island now stands as one of the clearest points where battlefield logic and macroeconomic leverage meet. Kharg handles 90% of Iran’s oil exports, and some reports showed that Iran continued to ship between 1.1 million and 1.5 million barrels per day during the war. Iran exported about 1.7 million barrels per day so far in 2026, with about 1.55 million barrels per day moving through Kharg, after exports had reached about 2.17 million barrels per day in February. That concentration gives the island a dual role. It functions as Iran’s main export valve and as a target whose condition shapes global expectations for supply, escalation, and endurance.

The strategic value of Kharg comes from concentration of flow, storage, and loading capacity in a single hub. The island holds storage capacity of roughly 30 million barrels and held about 18 million barrels of crude. Its offshore position also matters. Kharg as sitting 16 miles from Iran’s coast in waters deep enough for very large tankers that cannot approach the shallow mainland coast. That gives Kharg a special role in converting upstream production into export revenue at scale. A strike, blockade, or sustained interdiction at that one node would reach revenue, shipping schedules, tanker availability, buyer confidence, and physical balances at the same time. Market analysis are pointing to a potential loss of around 2 million barrels per day from the market if Kharg infrastructure were taken out.

Kharg also carries the fiscal weight of Iran’s external energy system. The U.S. Energy Information Administration’s 2025 SHIP Act report estimated Iran’s crude oil and condensate export revenue at $43 billion in 2024, with exports at 1.483 million barrels per day. The same report estimated exports to China at 1.444 million barrels per day in 2024, which shows how strongly Iran’s export realization depends on a narrow buyer corridor linked to Asian demand. Iranian oil accounted for 11.6% of China’s seaborne imports so far in 2026. Kharg therefore sits at the intersection of Iranian fiscal resilience and Chinese energy procurement. The island matters because it converts production into cash flow, and it does so through a commercial route that remains central to a major importing power.

U.S. forces struck more than 90 Iranian military targets on Kharg while preserving the oil infrastructure. That decision revealed the hierarchy of escalation inside the war. Military assets on the island formed the first target set, while the export system itself remained the larger coercive lever. Trump administration was considering plans to occupy or blockade Kharg in order to pressure Iran to reopen the Strait of Hormuz. Kharg thus moved from vulnerable infrastructure into active strategic bargaining space. In this setting, the island serves as a pressure point whose control, impairment, or threatened seizure can alter both the battlefield and the oil market.