Table of contents:

Introduction.

Deconstructing the November 2025 stimulus.

Why Bitcoin and US tech crashed.

A strategic pivot to industrial sovereignty.

Sector Analysis.

Japan premium and the geopolitical overlay.

Portfolio analysis and updates for 2026.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

The global financial architecture is currently undergoing a stress test, centered not in New York or London, but in Tokyo. As of late November 2025, markets are grappling with a seismic shift in Japanese economic policy that threatens to upend decades of assumptions regarding global liquidity. Check more about this here:

The synchronized arrival of the Sanaenomics fiscal stimulus package—unprecedented in the post-pandemic era—and the steepening of Japanese Government Bond yields has triggered a liquidity shock reverberating across asset classes, from the speculative fringes of cryptocurrency to the bedrock of US Treasuries. The era of the Japanese Yen serving as the world’s passive funding currency appears to be terminating, replaced by a new regime characterized by volatility, capital repatriation, and aggressive state intervention aimed at economic security.

Investors are witnessing what economic historians may later classify as a classic Minsky Moment in the Japanese sovereign debt market. A prolonged period of artificial stability, maintained through Yield Curve Control and negative interest rates, has bred an inherent instability that is now unwinding with ferocity. The catalyst for this dislocation is the announcement of a ¥21.3 trillion stimulus package by Prime Minister Sanae Takaichi. This maneuver has terrified bond vigilantes, who fear that Japan’s fiscal discipline has effectively collapsed precisely when inflationary pressures are forcing the Bank of Japan toward normalization. The immediate market reaction—a violent flash crash in Bitcoin and a sharp sell-off in US equities—underscores the deep, often underappreciated interconnectedness of Tokyo’s policy decisions with the global cost of capital.

However, it would be a strategic error to view this solely as a crisis. Within this volatility lies a generational rebalancing opportunity. While the broad carry trade unwinds, punishing assets dependent on cheap leverage, specific sectors within the Japanese economy are being aggressively capitalized by the state. The Takaichi administration is not engaging in indiscriminate spending; it is directing capital with surgical precision into National Crisis Management sectors:

Semiconductors (specifically the Rapidus ecosystem).

Shipbuilding.

Defense.

For the discerning institutional investor, the strategy for 2026 must pivot from passive index exposure to targeted allocation in Japanese value, banking, and industrial resilience, while aggressively reducing exposure to assets dependent on excess global liquidity, such as speculative US Tech and unhedged cryptocurrencies.

IN today’s report we detail the structural mechanics of the current crisis, analyzes the specific beneficiaries of the new fiscal regime, and provides a guideline for portfolio rebalancing in the face of the November 2025 market shock.

Deconstructing the November 2025 stimulus

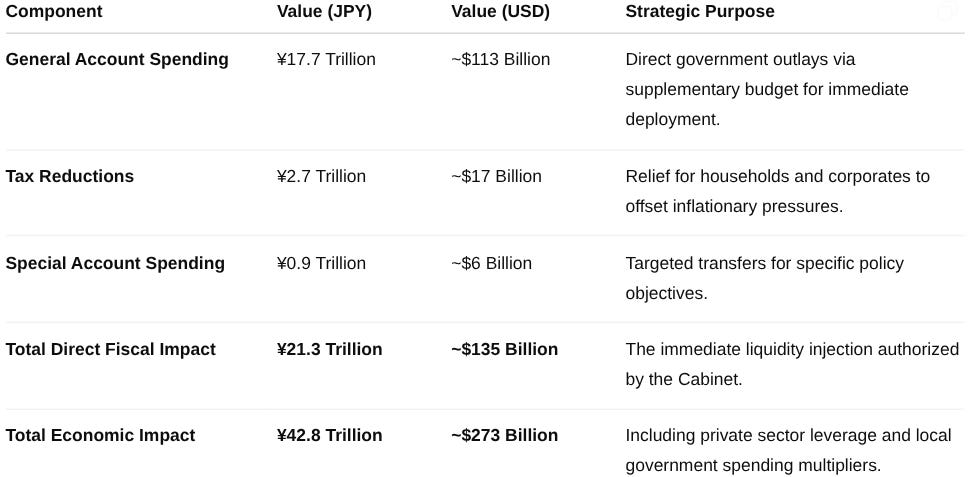

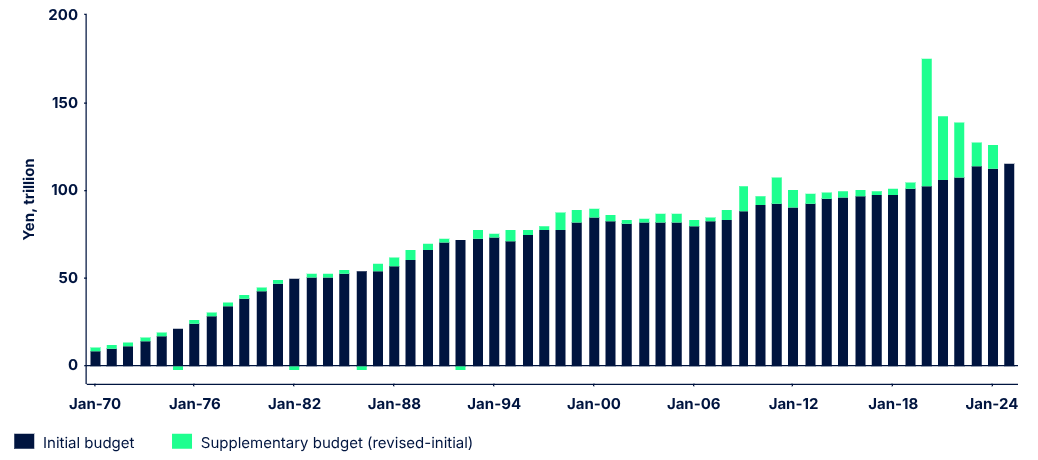

In a move that stunned fiscal conservatives and bond markets alike, the Cabinet of Prime Minister Sanae Takaichi approved a massive economic stimulus package on November 21, 2025. The sheer scale of this intervention indicates a government operating under a psychological wartime economic mentality, prioritizing social stability and industrial sovereignty over near-term balance sheet health. The approved package, totaling ¥21.3 trillion ($135 billion), represents the largest fiscal injection since the height of the pandemic, signaling a definitive departure from the incrementalism of previous administrations.

The package is significantly larger than the ¥13.9 trillion supplementary budget of the previous year and exceeds the ¥39 trillion total package of 2024, illustrating the escalating cost of maintaining economic momentum in a stagflationary environment. This expansionary stance, quickly dubbed “Sanaenomics,” mimics the aggressive fiscal dominance of the early Abenomics era (2012-2020). However, there is a critical distinction: Abenomics was deployed to fight deflation. Sanaenomics is being deployed into an environment of sticky 3% inflation, creating a dangerous pro-cyclical dynamic that risks unanchoring inflation expectations.

The funding mechanism for this package is the primary source of market anxiety. Takaichi confirmed that while the government will tap higher-than-expected tax revenue, any shortfall will be covered by additional Japanese Government Bond issuance. The prospect of increased supply, just as the Bank of Japan reduces its purchases, has created a supply-demand imbalance that is driving yields higher.

Investors must look beyond the headline numbers to the granular details of the stimulus to understand the true state of the Japanese economy. A critical inclusion in the package is the provision of rice vouchers and energy subsidies. The government is issuing supports of roughly ¥20,000 per child and subsidizing electricity and gas bills to the tune of ¥7,000 per household.

The necessity of such subsidies, particularly regarding staple foods like rice—prices of which have doubled in a year due to input costs and supply constraints—signals deep structural stress within the Japanese consumer economy. In a developed G7 nation, the resort to food coupons is a red flag indicating that the virtuous cycle of wage growth outpacing inflation has failed to materialize for the median household. The real wage growth remains negative despite nominal hikes, necessitating perpetual fiscal transfers that degrade the yen’s purchasing power. This suggests that the cost-push inflation is deeply entrenched, and the government feels compelled to subsidize the cost of living to prevent social unrest, a dynamic that creates a floor for inflation rather than resolving it.

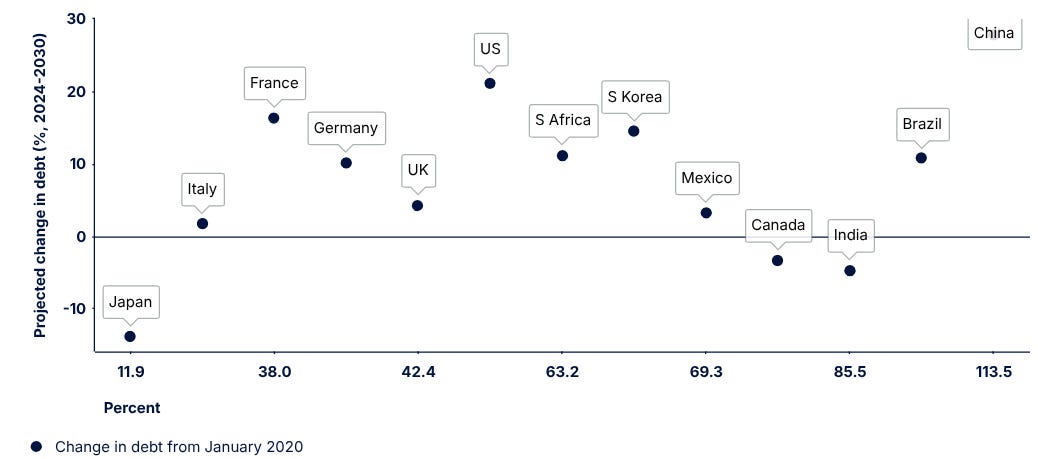

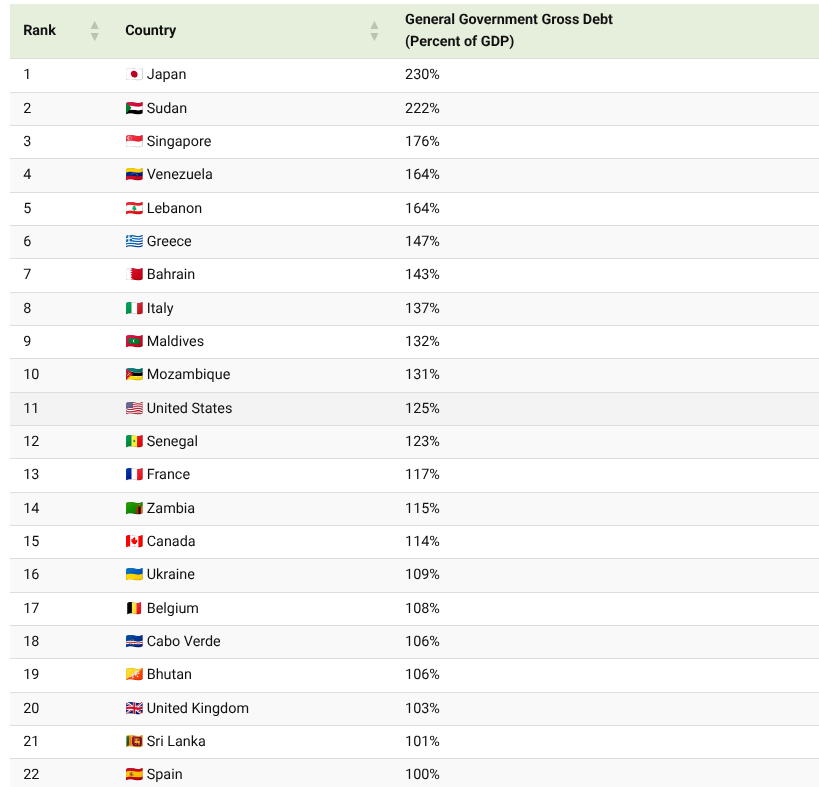

The market’s adverse reaction stems fundamentally from the funding mechanism. With Japan’s general government gross debt already projected at 229.6% of GDP for 2025, the issuance of new JGBs to fund this package is testing the market’s absorption capacity. While net debt figures are often cited as more manageable (around 140%), the gross issuance requirement determines the daily liquidity dynamics of the bond market.

The Bond Watchers—investors who punish fiscal profligacy by selling bonds and driving up yields—have returned to Tokyo. The fear is that Japan is following the trajectory of the UK’s mini-budget crisis of 2022, where unfunded spending caused a sovereign debt spiral. If the market refuses to absorb this debt at current yields, the Bank of Japan will be forced into a binary choice: intervene to monetize the debt (causing a collapse in the yen) or allow yields to rise unchecked (crushing domestic solvency).

This fiscal anxiety is compounded by political fragility. Takaichi leads a minority government coalition after the LDP lost its majority, necessitating cooperation with opposition parties like the DPP, who are demanding even larger tax cuts (raising the tax-free income threshold). This political dynamic suggests that fiscal discipline is unlikely to return soon, as every legislative victory will be bought with more spending.