[INTEL REPORT] Remapping of global dynamics

Global macroeconomic updates for the third quarter of 2025

Table of contents:

Introduction.

Conflict, commodities, and contagion risk.

A. Russia-Ukraine.

B. Israel-Gaza.

"America First" and the remapping of global trade.

The new doctrine.

The bilateral deal as the new model.

Political pressure and divergent policy paths.

The U.S. Federal Reserve under siege.

Stagflation in the UK, fiscal crisis in France.

Identifying structural winners and losers.

U.S. technology & AI.

European automotive sector.

Strategic asset allocation.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

The global investment landscape is entering a decisive inflection point. What was once an era of stable globalization and policy coordination has given way to a fragmented regime marked by geopolitical rivalry, transactional trade, and heightened domestic political risk. For investors, this is less a passing disruption than a structural shift toward persistent volatility—one that demands a rethinking of both asset allocation and risk management.

In this report we analyze the forces reshaping the investment environment:

Escalating geopolitical conflicts.

The redrawing of global trade relationships.

The divergent monetary frameworks across major economies.

The goal is to identify where resilience, policy tailwinds, and structural growth opportunities converge, and where legacy sectors face accelerating decline.

The central findings indicate that the conflicts in Ukraine and Gaza are not isolated events but catalysts for persistent stagflationary pressures, particularly in Europe. They are accelerating a global realignment away from U.S.-centric security and trade frameworks, a trend actively encouraged by the America First trade doctrine of the United States. This doctrine is forcing nations to choose between making substantial domestic investments in the U.S. to secure favorable trade terms or pivoting towards alternative economic blocs, such as a revitalized BRICS.

Concurrently, political interference is threatening the institutional credibility of the U.S. Federal Reserve, introducing a new layer of systemic risk into global financial markets. Check more about this here:

This contrasts with acute, but distinct, crises in Europe, where the United Kingdom grapples with stagflation and France faces a political meltdown with the potential for Eurozone-wide contagion.

These macro-level shifts are creating clear sectoral winners and losers. U.S. technology and domestic energy sectors are poised to benefit from powerful onshoring trends and supportive national policies. Conversely, the European automotive sector faces a structural decline, caught between punitive U.S. tariffs and overwhelming competition from Chinese electric vehicle manufacturers.

In this environment, a strategic shift in asset allocation is required. The analysis points toward a preference for hard assets and strategic commodities, such as gold and oil, which serve as hedges against geopolitical shocks and the potential for currency debasement. Furthermore, as regulatory frameworks for digital assets mature in both the U.S. and Europe, the underlying blockchain infrastructure is emerging as a compelling long-term investment theme. The investment paradigm has shifted from one of seeking broad emerging market growth to one that prioritizes resilience, technological sovereignty, and exposure to strategic, domestically-focused economies.

Conflict, commodities, and contagion risk.

The current investment environment is fundamentally shaped by geopolitical risk. The protracted conflict in Ukraine and the escalating crisis in the Middle East are not merely regional disputes; they are engines of global economic disruption. These conflicts act as catalysts, accelerating the fragmentation of the global order and generating persistent volatility that disproportionately impacts Europe while creating distinct risks and opportunities across asset classes.

A. Russia-Ukraine

The military conflict between Russia and Ukraine has settled into a grinding war of attrition. Russia maintains control over significant Ukrainian territory and, backed by a formidable nuclear arsenal that precludes direct NATO intervention, is unlikely to retreat. Ukraine's continued existence as a sovereign state is now critically dependent on sustained financial and military support from the United States and its NATO allies, positioning the conflict as a long-term strategic and economic drain on Western resources.

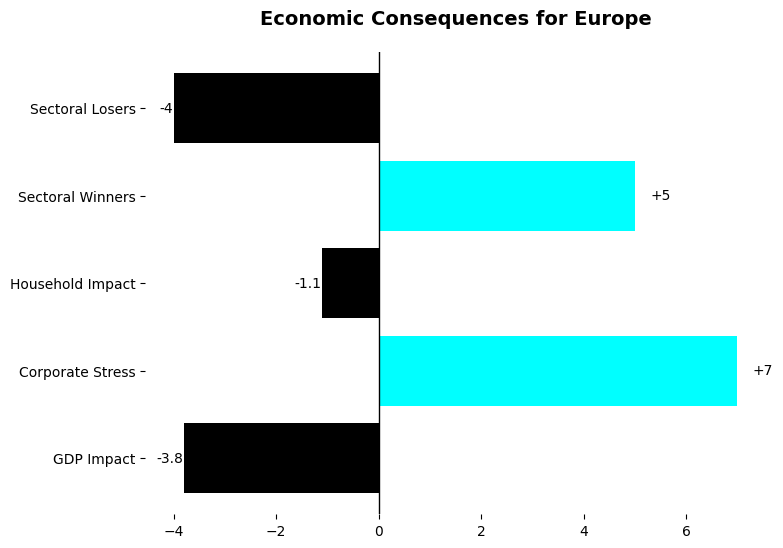

The economic consequences for Europe have been severe. The war triggered a massive commodity market shock, disrupting the supply of energy, food, metals, and fertilizers from a critical global breadbasket and industrial supplier. This disruption has been a primary driver of persistent inflation across the continent. The European Commission's forecasts starkly illustrate this impact: projected EU GDP growth for 2023 was revised down from 4.3% before the war to a mere 0.5%.

This macroeconomic shock has translated directly into corporate and household distress. A European Investment Bank analysis revealed that the surge in energy prices and the suspension of regional trade caused the share of EU firms at risk of default to climb from 10% to 17%. Sectors with high energy intensity, such as transport, chemicals, and agriculture, have been hit hardest. For consumers, the stagflationary environment has been punishing. Rising food and energy prices are estimated to have reduced real private consumption across the EU by 1.1%, pushing a greater share of the population toward the risk of poverty.

The persistence of this conflict creates a clear, long-term investment case for the defense and cybersecurity sectors. European nations, confronted with the reality of a major land war on their borders, are compelled to undertake a generational re-armament cycle, boosting order books for defense contractors. Conversely, the conflict represents a structural headwind for Europe's energy-intensive industries and consumer-facing businesses, which will continue to grapple with high input costs and weakened consumer demand.

B. Israel-Gaza

The conflict in the Middle East remains exceptionally volatile. The prospect of a full-scale Israeli occupation of the Gaza Strip presents a scenario fraught with humanitarian and geopolitical complexities that could further destabilize the region and damage Israel's international standing. Recent events, such as the Israeli strikes on the Al-Nasser Hospital that drew condemnation from Russia, China, and the European Union, underscore the escalating diplomatic risks and the potential for wider contagion.

Historically, geopolitical shocks originating in the Middle East trigger a predictable and sharp risk-off reaction in global markets. This pattern includes a flight to safety, benefiting safe-haven assets like the U.S. dollar and U.S. Treasury bonds, alongside a sell-off in global equities. The most significant economic threat stems from the potential for the conflict to escalate and draw in Iran, a major oil producer with the capacity to disrupt maritime traffic through the critical Strait of Hormuz. Such a scenario would trigger a severe oil supply shock, injecting a powerful stagflationary impulse into a global economy already struggling with persistent inflation.

A crucial development emerging from this conflict is the increasing weaponization of Environmental, Social, and Governance (ESG) criteria as a tool of foreign policy. The decision by Norway's $2-trillion sovereign wealth fund to divest its entire $2.1 billion stake in Caterpillar Inc. is a landmark event. The fund's Council on Ethics justified the move by citing the unacceptable risk that the company's equipment was being used in the widespread unlawful destruction of Palestinian property, constituting extensive and systematic violations of international humanitarian law. This marks one of the first instances of a major Western fund divesting from a non-Israeli company due to its role in the conflict, establishing a new precedent for complicity risk. The fund also divested a combined $661 million from five major Israeli banks for their role in financing the construction of settlements deemed illegal under international law.

The investment implications are twofold. First, the conflict reinforces the strategic value of holding energy assets as a hedge against supply shocks and U.S. defense contractors, whose stock performance has shown a positive correlation with rising conflict intensity in the region. Second, the Caterpillar divestment establishes a new, quantifiable ESG risk factor. Investors must now conduct deeper due diligence on the end-use of products and services for any company operating in or supplying to conflict zones, as the risk of divestment by major institutional funds on ethical grounds is no longer theoretical.

"America First" and the remapping of global trade

The global trade architecture is being fundamentally reshaped. The U.S. administration's America First policy represents not a cyclical shift but a structural break from the post-Cold War era of multilateralism. This new paradigm is explicitly transactional, viewing international commerce through a lens of national power and strategic competition. It is forcing a worldwide realignment, creating a bifurcated system of clear winners who align with U.S. interests and losers who face significant economic pressure.

A. The new doctrine

The foundational principle of the current U.S. trade policy is the end of the previous era of globalization, a shift that has caught traditional allies, particularly the European Union, off guard. The approach is explicitly transactional and nationalistic, re-framing persistent trade deficits not as a benign outcome of comparative advantage but as a direct threat to U.S. economic and national security. This ideological shift provides the justification for the aggressive use of tariffs as the primary instrument for rebalancing global trade flows and coercing trading partners.