[INTEL REPORT] Rates, barrels, borders

Energy balances, supply-chain constraints, and geopolitical event risk

Table of contents:

Introduction.

Global macro outlook.

Regional breakdown.

Major geopolitical flashpoints.

Commodity markets and supply chains.

Financial markets and capital flows.

Policy and regulatory trends.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

Growth can print while the distribution of outcomes widens, because the drivers that move expectations arrive as policy decisions sanction packages, court rulings, or any other events. Markets price that distribution every day through curves, basis, dispersion, and volatility surfaces, often faster than macro releases can confirm the regime shift.

Large refinancing calendars and ongoing portfolio runoff change who absorbs duration and at what price, which means the term premium becomes more active. In that setting, the same growth print can produce different outcomes depending on auction demand, collateral conditions, and the willingness of balance sheets to intermediate. This is why the discussion of central banks sits alongside issuance and liquidity: the reaction function only matters if the market can clear the supply without repricing risk.

Trade policy and regulation matter in the same way: they are rule changes that modify cash-flow boundaries and execution constraints. Tariff schedules alter landed costs, sourcing, and inventory timing. Legal pathways and exemption design shape how durable the tariff environment is, which in turn shapes how firms time capex and how markets price margins. Sanctions and enforcement innovations act through shipping, insurance, classification, and payments, changing the set of compliant routes and the economics of delivery. These are microstructure channels with macro consequences, and they move faster than quarterly accounts. If you trade cross-asset, you already know the pattern: the first clean signal often appears in basis, time spreads, freight, and vol before it reaches earnings or CPI.

But there are much more, indeed, if you want to go deeper don’t miss this:

Financial markets and capital flows tie the regime together by showing who finances whom and under what conditions. Fund flows reveal risk appetite and breadth, while cross-border data anchors the foreign bid that matters for rate clearing and dollar dynamics. In 2026, these flow signals interact with policy stability, issuance pressure, and market depth in a way that can flip the sign of traditional relationships.

Global macro outlook

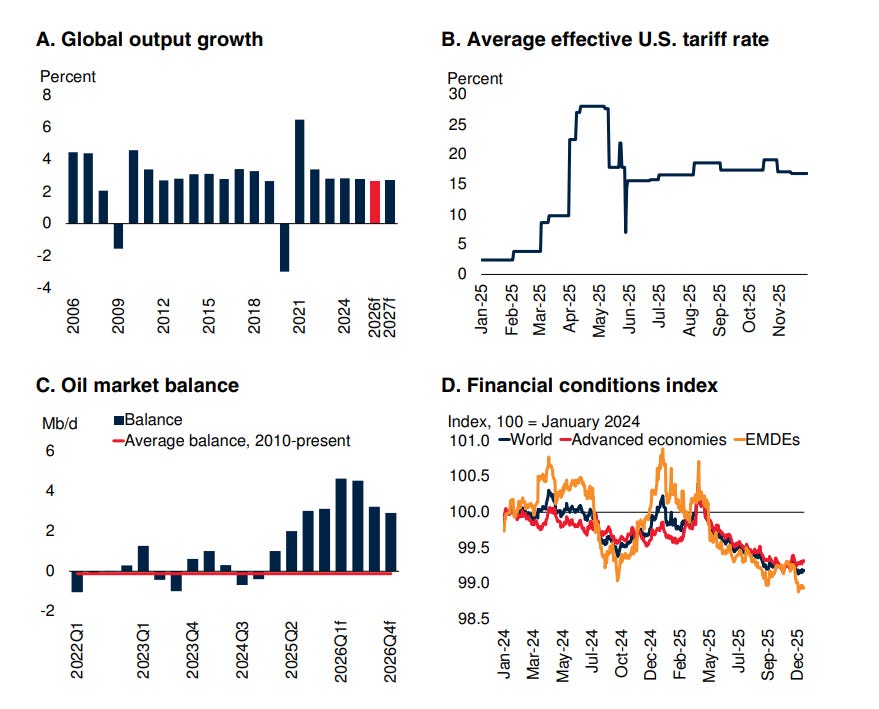

The World Bank describes resilience amid persistent trade tensions and uncertainty, and it points to a mild step-down in growth as demand for traded goods cools after a tariff-related pull-forward in 2025. The UN’s 2026 outlook reinforces this texture by forecasting subdued global growth relative to the pre-pandemic average and by linking trade tensions and fiscal strains to the outlook. The IMF’s update frames the offsetting forces that keep growth steady, with technology investment and private-sector adaptability acting as counterweights to trade policy headwinds. In that IMF framing, technology-linked capex, including investment tied to artificial intelligence, plays a role in sustaining activity even when goods trade momentum softens.

A services-led expansion favors domestic demand signals, labor income dynamics, and pricing power inside non-tradable segments. A cooling goods cycle shifts the focus toward inventories, freight rates, and margin compression in trade-exposed firms. Policy uncertainty adds a layer of option-like convexity to macro outcomes: tariff announcements, legal rulings, and negotiated carve-outs create discrete jumps in expectations that propagate through FX basis, forward points, and equity dispersion. Reporting on tariff policy illustrates this channel by showing how legal constraints and policy substitutions sustain uncertainty even when headline measures change.

The front-loading mechanism matters because it alters the timing of realized activity. When firms advance imports ahead of higher tariff schedules, measured trade volumes and goods output pull demand from future quarters into the present. World Bank communication around Global Economic Prospects links this pattern to the 2025 trade impulse and expects that tailwind to fade, leaving a softer goods backdrop in 2026. The key step involves separating genuine final-demand strength from calendar-shifted flows. A model that treats the 2025 goods surge as durable can overstate cyclical beta and underweight defensive carry. A model that recognizes the inventory-and-tariff cycle can frame 2026 as a transition from goods momentum toward services endurance, with factor leadership that rotates across value chains and across regions in different phases.

Trade policy shifts influence external balances and currency pressures through re-routing of goods flows. When tariff schedules change, exporters redirect volume toward markets with lower barriers, and importers shift sourcing toward jurisdictions that preserve margin. Reporting on tariff developments highlights a setting where tariff policy remains a durable feature of the landscape, and it points to diversion of Chinese exports toward Europe and other regions as part of the adjustment. ECB analysis of China’s widening goods trade surplus since the pandemic provides a complementary lens on how global goods trade patterns evolve amid geopolitical tension and shifts in trade policy. These forces matter for quant strategies because external balances drive medium-horizon FX drift, while trade shocks drive short-horizon FX volatility, and the interaction between the two shapes carry-to-trend transitions in currency markets.

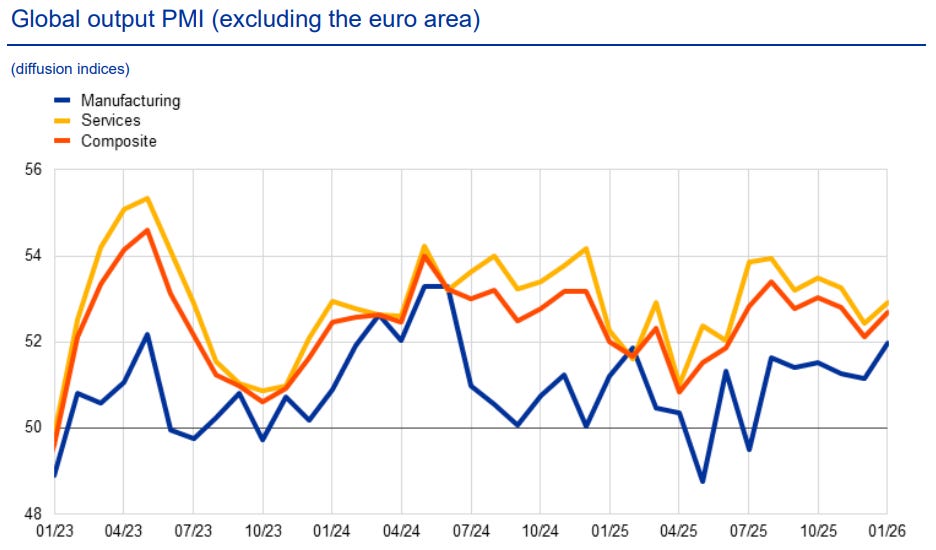

ECB analysis describes services activity that continues to expand while industry remains muted, using PMI measures as a signal of a recovery that runs through services first. This pattern appears in survey releases that show services readings holding above the expansion threshold while manufacturing moves toward stabilization. PMIs in Germany and France captures cross-country dispersion inside the euro area, with services carrying the composite in Germany and weaker demand weighing on French activity. These survey dynamics matter for trading research because PMI surprises map into short-horizon moves in rates, cyclicals, and currencies, while the level and composition of the PMI can guide medium-horizon positioning in curve steepeners, credit carry, and sector rotation.

PMI data provides a bridge between growth narrative and microstructure. A services-led composite often coincides with sticky wage dynamics, steadier cash-flow expectations in domestic-oriented sectors, and a tighter link between labor-market prints and rate pricing. A manufacturing stabilization phase tends to lift sensitivity to new orders, inventories, and global demand proxies. In systematic research, this implies that the same headline PMI level can support different trade decisions depending on whether services or manufacturing drives the move. It implies that signal design benefits from separating diffusion indexes by sector and by subcomponents such as new orders and employment, then aligning those readings with the asset classes that transmit the information with the least delay. The ECB’s characterization of a dual-speed recovery gives a qualitative anchor for this decomposition.

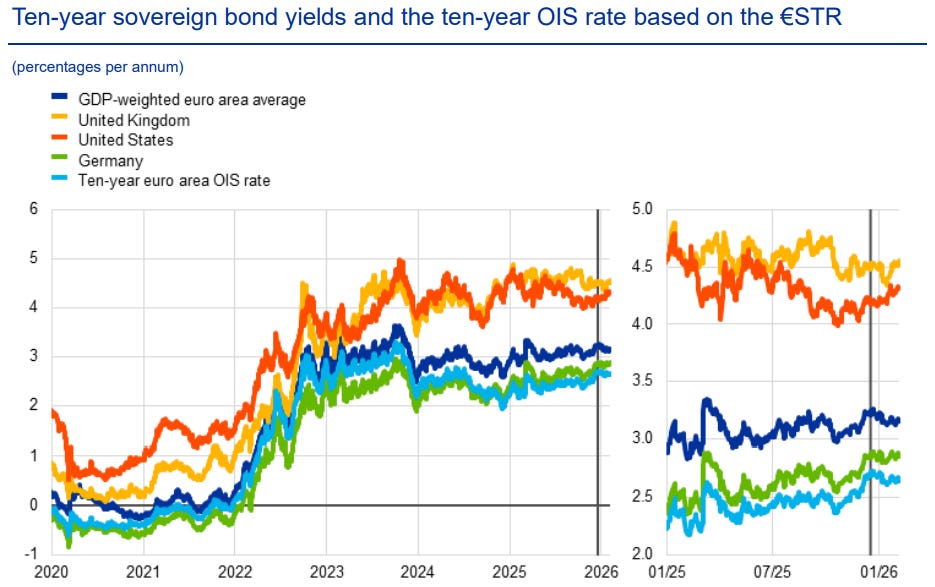

Central-bank decisions in the opening months of 2026 translate these macro signals into a policy-rate path that markets price each day. The Federal Reserve’s statement kept the target range unchanged and emphasized assessment of incoming data and the balance of risks. The ECB’s decision kept key rates unchanged and pointed to resilience supported by labor-market conditions and the rollout of public spending on defense and infrastructure. The Bank of England’s minutes show an internal split, with a narrow majority favoring an unchanged policy rate and a sizable minority favoring a cut. These decisions describe a global reaction function that prices a wide corridor for cuts, with emphasis on inflation evidence, services pricing, and the durability of disinflation.

Policy communication matters alongside the decision itself because it governs how markets map the same data to different paths for rates. A steady policy rate with language that emphasizes confidence in convergence to target supports carry regimes, where realized volatility remains low relative to the level of yields. A steady policy rate with language that emphasizes uncertainty around inflation drivers supports volatility regimes, where rates option markets price a wider distribution of paths. The ECB’s communication points to medium-term stabilization of inflation at target while describing a challenging global environment that includes policy uncertainty. This combination encourages a research posture that treats rate cuts as a function of inflation composition and of the persistence of growth in services, rather than as a function of headline growth alone.

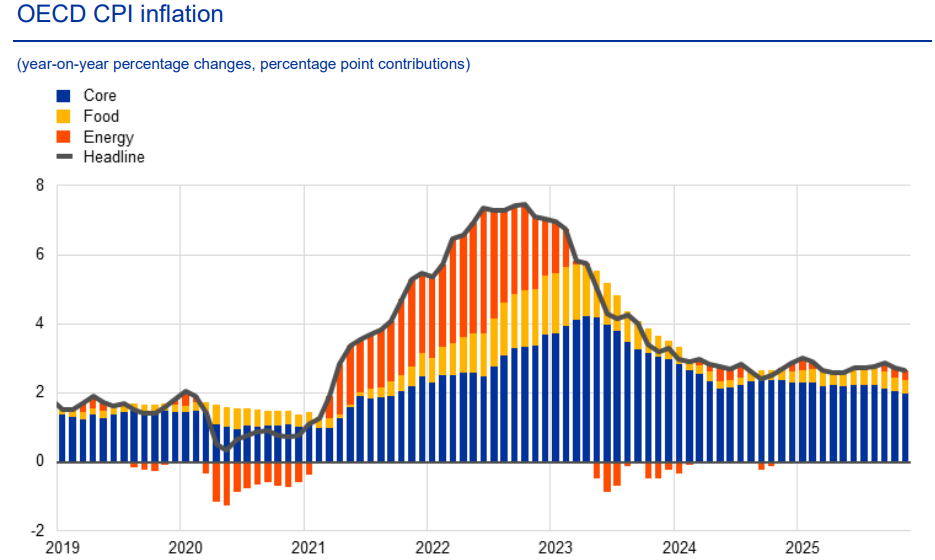

Inflation dynamics form the hinge between macro and policy caution, and energy sits at the center of that hinge at the start of 2026. ECB analysis attributes the expected decline in headline inflation to base effects linked to energy prices, and separate ECB reporting shows a large negative reading for energy inflation alongside softer underlying inflation measures. Oil markets move in a direction that reduces the disinflation impulse that came from earlier price declines. As crude prices rise and year-over-year declines narrow, which pushes oil’s impact toward inflation pressure and raises the hurdle for policy easing. World Bank commodity data shows a rise in the energy price index driven by moves in natural gas and crude oil, reinforcing the picture of an energy complex that feeds into near-term inflation prints through transport and input costs. IEA market reporting adds a supply-side layer, with a large supply response projected that interacts with geopolitics and weather to drive volatility around the inflation path.

Energy-driven inflation pressure interacts with tariffs through pass-through channels that vary across economies and across consumption baskets. When tariff schedules rise, tradable-goods prices can reflect a combination of higher landed cost and of shifts in sourcing. When energy prices rise, freight and input costs amplify that pass-through. The World Bank’s emphasis on trade policy shifts and uncertainty outlook highlights the macro setting where these channels matter for inflation forecasts and for policy paths. The practical implication involves treating inflation as a composite of distinct drivers rather than as a single series. Energy, goods import prices, and services inflation each respond to different shocks and each maps into different parts of the curve and different equity sectors.

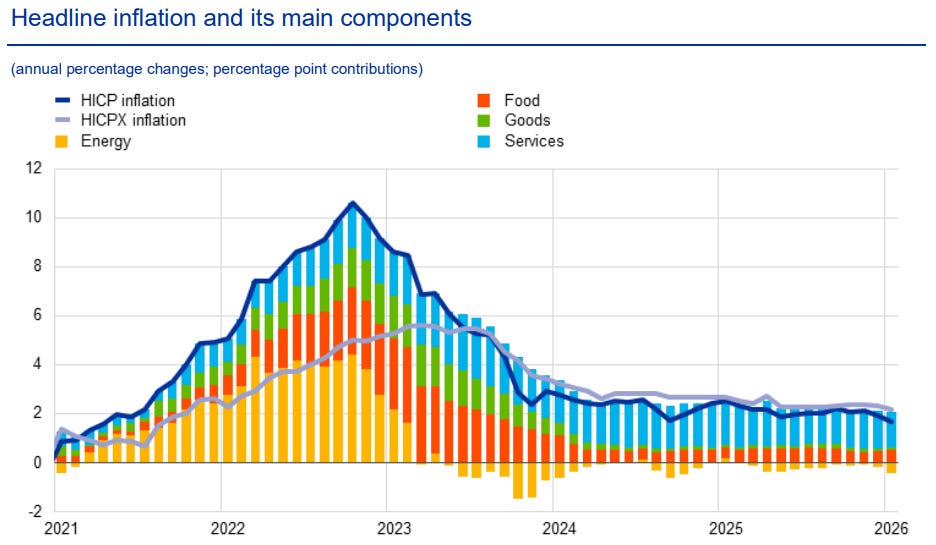

The euro-area inflation channel adds a second force that pulls in the opposite direction through goods prices. The ECB policymaker Fabio Panetta on the role of Chinese imports in the sharper-than-forecast drop in euro area inflation, linking disinflation in exposed goods categories to price and volume dynamics in import competition. An ECB Economic Bulletin focus box provides context by describing the rise in Chinese competitive pressure across export markets and its implications for European firms. This combination produces a cross-category split where goods disinflation can coexist with services stickiness, which keeps the inflation profile two-sided even when headline prints move below target for a time. This split carries direct implications for quant models that use inflation surprises as a single factor, since the market response can differ when the surprise comes from tradable goods versus domestic services.

Energy uncertainty and supply disruptions remain the second half of the euro-area inflation story. ECB communication frames geopolitical tensions as a source of two-sided inflation risks through energy markets, confidence, and business investment. Panetta’s comments point to energy instability and supply-chain disruptions as upside risks alongside the disinflationary pressure from import competition. This configuration supports an inflation process that behaves like a mixture of mean reversion in goods and jump risk in energy-sensitive components. That structure supports stress testing portfolios against energy spikes and supply-chain events, while mapping the influence of import prices on goods-sensitive sectors and on inflation-linked instruments.

Fiscal capacity shapes the medium-horizon risk premium landscape because it governs sovereign issuance, refinancing calendars, and the credibility of backstops. As refinancing needs rise and central bank balance sheets shrink through runoff, the marginal buyer of duration shifts toward price-sensitive private investors, which places emphasis on term premia as a driver of long yields. An ECB speech on safe asset abundance argues that large fiscal deficits and balance-sheet normalization reduce the safety and liquidity premia embedded in government bonds, compressing the convenience yield that investors pay for scarce safe assets and changing the forces that shaped real long-term rates during the prior decade.

This fiscal and balance-sheet backdrop matters for pricing in a way that reaches beyond government bonds. A rise in term premia raises discount rates that feed into equity valuations, increases the hurdle for private credit origination, and shifts the relative appeal of carry strategies versus volatility strategies. It places a premium on liquidity, since price-sensitive investors demand compensation for balance-sheet use during periods of heavy issuance. This argues for explicit monitoring of issuance calendars, auction tails, and measures of market depth in core sovereign futures, because those observables act as the proximate mechanism through which a fiscal narrative becomes a PnL driver. The IMF emphasis on public debt dynamics and the ECB focus on convenience yield provide the macro foundation for building those monitors.

Financial stability adds another layer because valuation and liquidity conditions shape the transmission mechanism from macro shocks into asset prices. The IMF’s October 2025 Global Financial Stability Report frames financial stability risks as elevated amid stretched asset valuations, sovereign bond market pressures, and the rising influence of nonbank financial institutions, and it highlights structural shifts in foreign exchange and emerging market bond markets that reshape both risk and resilience. This matters for systematic strategies that lean on historical diversification patterns, since structural market plumbing determines the speed and shape of drawdowns and the path of margin dynamics. The IMF’s discussion of stock-bond diversification complements this framing by linking bond-market dynamics to the absorption of supply by price-sensitive investors under balance-sheet runoff.