Table of contents:

Introduction.

Asia-Pacific and strategic tensions.

U.S.-China relations.

U.S.-Russia dynamics.

Middle east energy risk.

Latin America’s alignments.

Debt and monetary shifts.

Portfolio strategy updates for Q1 2026.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

Markets don’t announce their turning points with volatility. More often, they drift—calm on the surface: alliances harden, supply routes get repriced, reserve assets get questioned, and policy tools lose degrees of freedom under debt. Early 2026 feels like one of those regimes. Risk isn’t higher in the headline sense; it’s more convex: fewer obvious warnings, but larger consequences when specific nodes break.

Think about that: a trade decision can move FX expectations; FX stress can alter reserve behavior; reserve behavior can reshape bond term premia; bond premia can tighten financial conditions; and tight conditions can force policy choices that echo back into geopolitics. The goal is to identify the handful of pressure points most likely to surprise portfolios in Q1 2026.

The structure follows a simple logic: start where momentum is strongest and mispricing is most tempting (Asia-Pacific), move through the two central strategic relationships that set the global risk budget (U.S.–China and U.S.–Russia), then into the corridor where energy volatility still has the cleanest transmission into inflation and rates (the Middle East). From there, it shifts to Latin America as the proving ground for spheres-of-influence dynamics, and finally to the macro plumbing—debt, reserves, and monetary credibility—where long-cycle risks are accumulating even in normal markets.

In regimes like this, the mistake is to look for a single catalyst. The real driver is coupling: more assets, policies, and institutions are linked through the same handful of constraints—financing, energy, security, and settlement. When coupling rises, diversification can fail quietly.

So the right question is less what happens next? and more where is the system least tolerant to surprise? Look for asymmetries: places where a small change forces a large adjustment; where hedges are expensive because everyone wants them; where policy is boxed in by debt; where supply is one incident away from being repriced; where credibility matters more than guidance. Early 2026 is full of those asymmetries.

Asia-Pacific and strategic tensions

In Japan, Prime Minister Sanae Takaichi’s ruling party clinched a landslide snap-election victory in January, securing a supermajority in the lower house. This historic mandate has paved the way for expansive fiscal stimulus (including promised tax cuts and AI/semiconductor investments) while pledging responsible budgeting to avoid exacerbating Japan’s heavy debt load. Markets responded with enthusiasm: the Nikkei 225 surged 3.9% to an all-time record high above 56,000, reflecting investor confidence in a stable, pro-growth government. Japanese equities rallied across exporters, cyclicals, financials, and even defense stocks as part of a Japan is Back narrative.

Super-long Japanese bond yields spiked on fears of massive new issuance, but leveled off as Takaichi emphasized fiscal prudence – calming bond markets wary of Japan’s debt (the highest in the developed world). The Bank of Japan remains on intervention watch: the yen initially weakened to multi-decade lows, then rebounded after officials warned of potential yen-buying intervention to curb excess volatility. Overall, Japan’s political reflationary policy mix have turned it from a contrarian play into a reform-driven growth story, improving regional investor sentiment.

Asia-Pacific markets have benefited from both regional developments and a rotation out of overvalued U.S. tech stocks. The MSCI Asia Pacific Index jumped about 2.5% to reach an all-time high in early February. Alongside Japan’s rally, South Korea’s Kospi – seen as a proxy for AI-related investments – surged over 4%. Additionally, a surprise conservative election win in Thailand helped anchor optimism, strengthening the Thai baht. The region’s outperformers have been bolstered by comparatively lower equity valuations and stronger growth prospects than U.S. markets. Capital flows into Asia are accelerating as global investors fade uncertainty – shifting funds from pricey U.S. technology shares into Asian equities and other undervalued opportunities. Bitcoin and other risk assets have also rebounded alongside Asian stocks, reflecting improved risk appetite as immediate volatility subsides.

Despite a veneer of market calm, the Asia-Pacific region faces underlying strategic tensions. Taiwan remains a central flashpoint in U.S.-China relations. In a January phone call, President Trump and President Xi Jinping acknowledged the importance of a good relationship, but Xi pointedly warned that Taiwan is the most important issue and urged Washington to handle arms sales to Taiwan with prudence. Any misstep on Taiwan could reignite regional volatility. Additionally, the U.S.-China trade and tech rivalry continues to simmer. Beijing has been assertively pursuing self-reliance in semiconductors and AI, while Washington maintains tariffs and export controls. In fact, uncertainty around trade policy briefly rattled markets when President Trump announced new tariffs on South Korean imports in late January – a move seen as a protectionist signal that could indirectly pressure China. So far, however, Asia-Pacific stability has held, aided by diplomatic engagement (e.g. Trump planning to visit China in April, per official statements) and by the region’s internal economic momentum.

Asia-Pacific’s outlook appears favorable in the current climate. With Japan’s pro-growth policies and political stability, Japanese equities have become attractive – in sectors like industrials, finance, and consumer staples which stand to benefit from domestic stimulus and a stronger yen. Broader Asian emerging markets may see increased inflows as investors diversify away from U.S. tech; select Asian equity funds or ETFs could outperform given lower valuations. However, any escalation around Taiwan or in U.S.-China frictions could reverse Asia’s rally. Keeping an eye on upcoming policy decisions (e.g. Bank of Japan shifts or trade negotiations) is crucial.

U.S.-China relations

A noteworthy development in early 2026 is China’s move to shield itself from U.S. financial risks, which has significant geopolitical undertones. In February, Chinese regulators urged banks to curb US Treasuries exposure, cautioning lenders to limit purchases of U.S. government bonds and gradually reduce existing holdings. This directive, confirmed by people familiar with the matter, was framed as a risk-management measure against concentration and market volatility – not a geopolitical maneuver.

Even so, markets reacted and U.S. Treasury yields ticked higher (10-year yield up ~3 basis points to ~4.24%) as prices fell, the U.S. dollar slipped on the news, and U.S. equity futures pared gains. Strategists note this signal from one of the world’s largest U.S. creditors is a challenge to the dollar, especially as it comes on the heels of concerns over Washington’s fiscal policy. Indeed, global investors are questioning U.S. governance: Trump’s commitment to a strong dollar and the Federal Reserve’s independence have come under doubt.

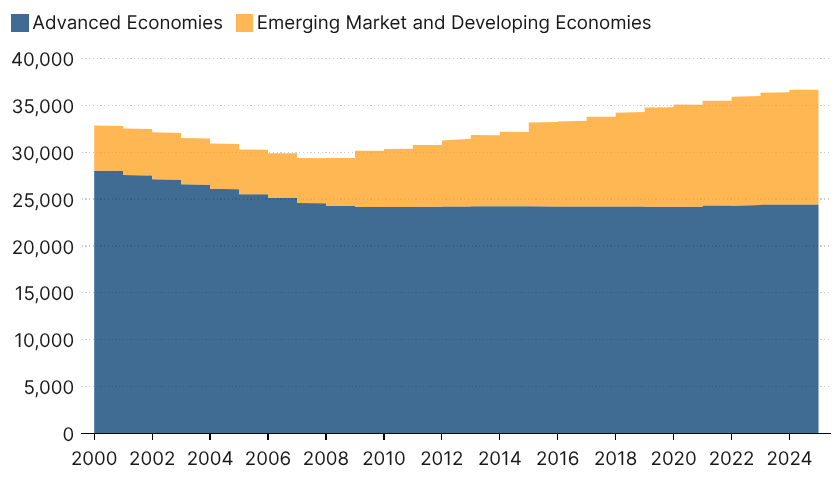

China’s cautious diversification away from U.S. debt aligns with a broader de-dollarization trend, wherein central banks (including China’s) are raising gold reserves and settling more trade in yuan. This trend has helped drive gold to record highs above $5,000. For now, Beijing’s Treasury curbs have been modest and state entities (like China’s central bank) reportedly remain major holders of U.S. debt. However, the move telegraphs a long-term intent to reduce reliance on U.S. assets, potentially as a hedge against future U.S. sanctions or financial conflict. U.S. policymakers are taking note: the Achilles heel of U.S. fiscal health has always been its external financing needs, and China’s actions underscore that vulnerability.

The Trump Administration’s return has been marked by a revival of hardline trade tactics, not only toward China but even traditional allies. In addition to new tariffs on South Korean goods, the U.S. continues to enforce high tariffs on Chinese imports (a legacy of the 2018–19 trade war) and restrict China’s access to advanced semiconductor technology. China, for its part, has invested in tech and AI capabilities, but the global AI race has introduced new complexities. One of the biggest market vulnerabilities stemming from AI is hitting U.S. software companies – a development that also impacts Chinese tech indirectly.

In January, Wall Street saw a selloff dubbed software-mageddon: U.S. software and data service stocks plunged in value as investors feared that fast-advancing AI tools (like Anthropic’s Claude 4.6) could disrupt these firms’ business models. The S&P 500 Software & Services index dropped over 15% in January, erasing about $1 trillion in market cap since its peak, as hedge funds slashed exposure and short interest spiked. Even industry giants were not spared – e.g. Microsoft fell ~5% in one day. A Goldman Sachs strategist warned that while near-term earnings might hold up, they are insufficient to disprove the long-term downside risk from AI. This mass repricing reflects an existential worry: could generative AI automate away large swathes of software jobs and services? Data vendors saw sharp declines on fears that AI-driven platforms could replicate their offerings. Some stability returned by early February – analysts noted the sector had reached deep oversold conditions reminiscent of 2022, and value buyers emerged. But the episode highlights a key point: the AI arms race is disruptive, and not only to the U.S. tech sector. China’s tech industry faces similar AI-related disruption risks (and also U.S. export controls on chips), meaning this is a shared vulnerability even amid U.S.-China competition.

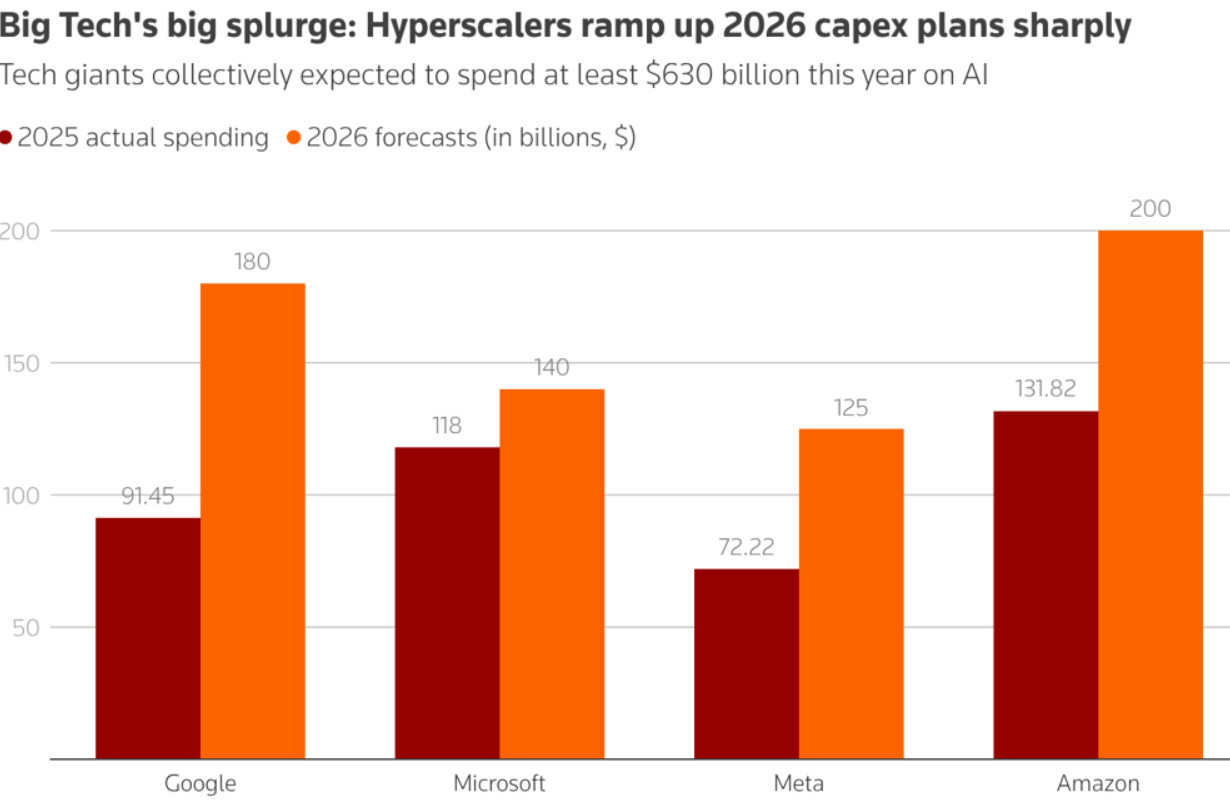

Major U.S. tech firms plan ~$630–650 billion in 2026 capital expenditures – to build AI data centers and infrastructure – a ~36% jump that is squeezing profits and alarming investors. This unprecedented AI arms race investment by Amazon, Alphabet, Meta, and others is shifting these companies from asset-light models to asset-intensive ones.

Despite economic tensions, Washington and Beijing have maintained cautious diplomatic engagement in early 2026. High-level communication lines are open – exemplified by the Trump-Xi phone call in January, where both leaders agreed on the importance of a stable relationship and discussed issues ranging from Iran to trade in U.S. soybeans and energy. This call resulted in plans for President Trump to visit China in April, signaling a willingness to manage differences through dialogue.

Nonetheless, core strategic disagreements persist. China’s latest Policy Paper on Latin America and the Caribbean (published December 2025) criticized U.S. hegemonism and pledged support for nations opposing unilateral bullying – rhetoric aimed at U.S. influence. Concurrently, the new U.S. National Security Strategy labels China a non-hemispheric competitor in the Americas. These documents underscore a widening ideological rift: China champions multipolarity and globalization in the right direction, whereas the U.S. is doubling down on its sphere-of-influence doctrine (as seen vividly in Latin America, discussed in a later section). In the Indo-Pacific, military posturing continues. The U.S. Navy maintains an increased presence in the South China Sea and Taiwan Strait, while China regularly conducts military drills around Taiwan. Both sides are wary of accidents or miscalculation – a Chatham House analysis warns that Trump’s initially ambiguous stance on Taiwan raised the risk of an accidental conflict, and calls for clearer U.S. policy to avoid escalation. So far, no direct crisis has erupted in 2026, but this is an ever-present tail risk.

If you want to know more about the US-National Defense Strategy check:

Heightened U.S.-China tensions argue for caution in sectors exposed to trade or regulatory crossfire. For instance, U.S. semiconductor and cloud computing firms face both export restrictions and rising competition from Chinese alternatives – any portfolio should limit over-concentration in these names. On the other hand, sectors like industrial machinery, infrastructure, and non-tech consumer goods in the U.S. and allied markets could be relative winners as governments channel investment into supply-chain resiliency (e.g. building chip plants domestically) and as consumers pivot spending patterns. On the Chinese side, equities continue to carry geopolitical risk discounts. Only risk-tolerant investors should consider partial exposure (for example, via broad emerging Asia funds) – and even then, allocations should be small and balanced against Western assets.

If de-dollarization efforts accelerate (e.g. more countries using yuan for trade), the dollar may face gradual depreciation pressure. Investors might diversify some currency exposure – holding a portion of assets in foreign currency funds or gold – as a hedge against any erosion in dollar dominance. Overall, portfolios should stay agile: U.S.-China developments can shift quickly with policy announcements or geopolitical events, so periodic rebalancing (quarterly or around key summits) is advisable.