Table of contents:

Introduction.

From venture capital to sovereign debt.

The chinese threat.

Europe: The Draghi report, regulations, the impact of the AI and capital flight.

The physics of scaling: 106 GW by 2035.

Copper, uranium, and critical minerals.

Portfolio strategy 2026.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

For two decades, the dominant narrative was simple: software ate the world, and in doing so, freed itself from the constraints of the physical one. Asset-light business models, zero marginal cost, infinite scalability—these were not just buzzwords, they were the justification for paying 20–30x sales for anything with a login screen and an acronym in the name. That era is ending. The arrival of frontier AI has snapped the tether between tech and light. Training and deploying AGI is not a SaaS problem but an industrial policy problem. To know more about this take a look of:

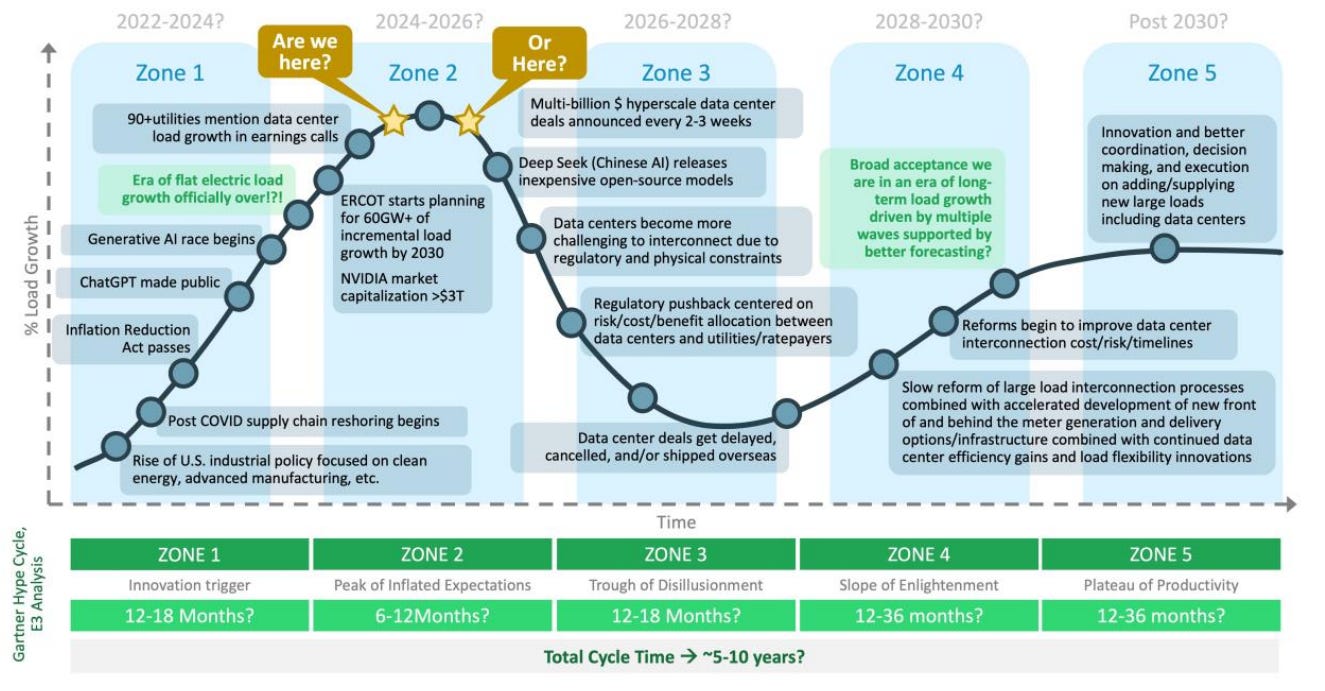

The data-center hype cycle suggests we are at the late stages of Zone 2—the peak of inflated expectations—just before AI load growth runs into grid bottlenecks, regulatory pushback, and cancelled projects. The portfolio strategy that follows assumes that the next phase is not cheaper compute, but a long, capital-intensive slog through those constraints.

OpenAI’s trillion-dollar infrastructure ask is the template. AI at scale demands gigawatts of baseload power, hundreds of billions in data-center capex, and secure access to copper, uranium, and critical minerals. The unit of competition is no longer monthly active users, but megawatts and tonnes. As the cost and risk of this buildout exceed what private markets can rationally bear, states are stepping in as the only balance sheets large enough to keep the experiment running.

At the same time, the geopolitical map is being redrawn around energy and regulation. China has quietly shifted the game from chip efficiency to energy abundance, subsidizing electricity to neutralize US export controls. Europe, lacking scale champions, has defaulted to a model of regulatory extraction that actively repels growth capital. The US, caught between its AI ambitions and an overstretched grid, is being forced into a messy blend of nuclear revival, extended fossil lifelines, and emergency grid spending just to keep data centers online.

From venture capital to sovereign debt

For twenty years, the prevailing wisdom in global markets was that technology companies were asset-light. They scaled infinitely with minimal marginal cost, delivering gross margins that justified stratospheric valuations. In December 2025, that era is demonstrably over. The financial architecture of Silicon Valley has buckled under the weight of the physical requirements of AGI.

Recent disclosures indicate that OpenAI, the vanguard of the generative AI revolution, has formally petitioned the United States government for loan guarantees to support an infrastructure buildout estimated at over $1.15 trillion. This figure represents a capital expenditure requirement roughly equivalent to the GDP of Indonesia. The request for a federal backstop is a tacit admission that the unit economics of AI, in its current training phase, do not function under traditional private equity models.

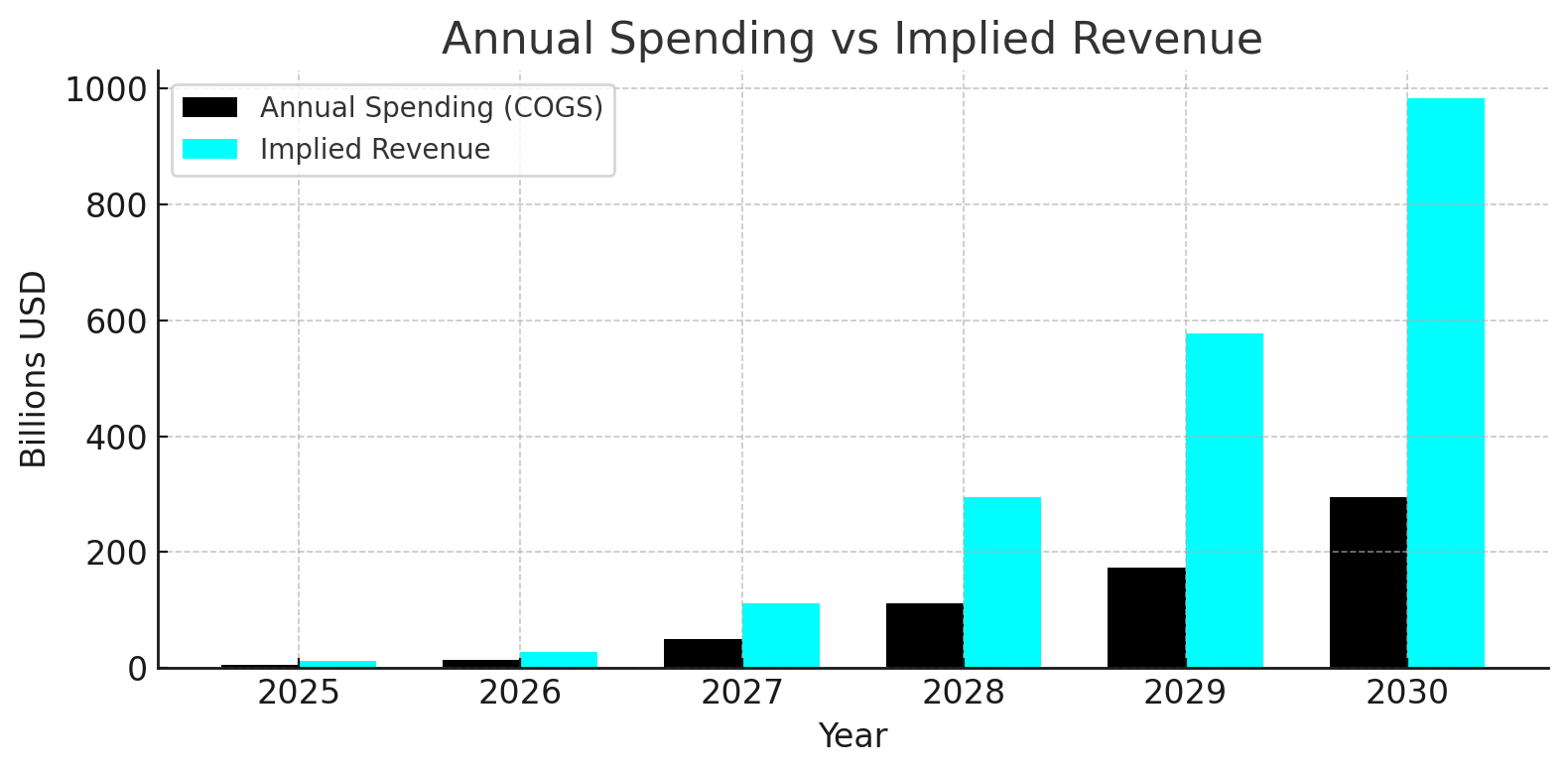

OpenAI projects a 48% gross profit margin in 2025, improving to 70% by 2029. If we assume all infrastructure spending flows through cost of goods sold, we can calculate the implied revenue needed to support these spending levels at OpenAI’s target margins.

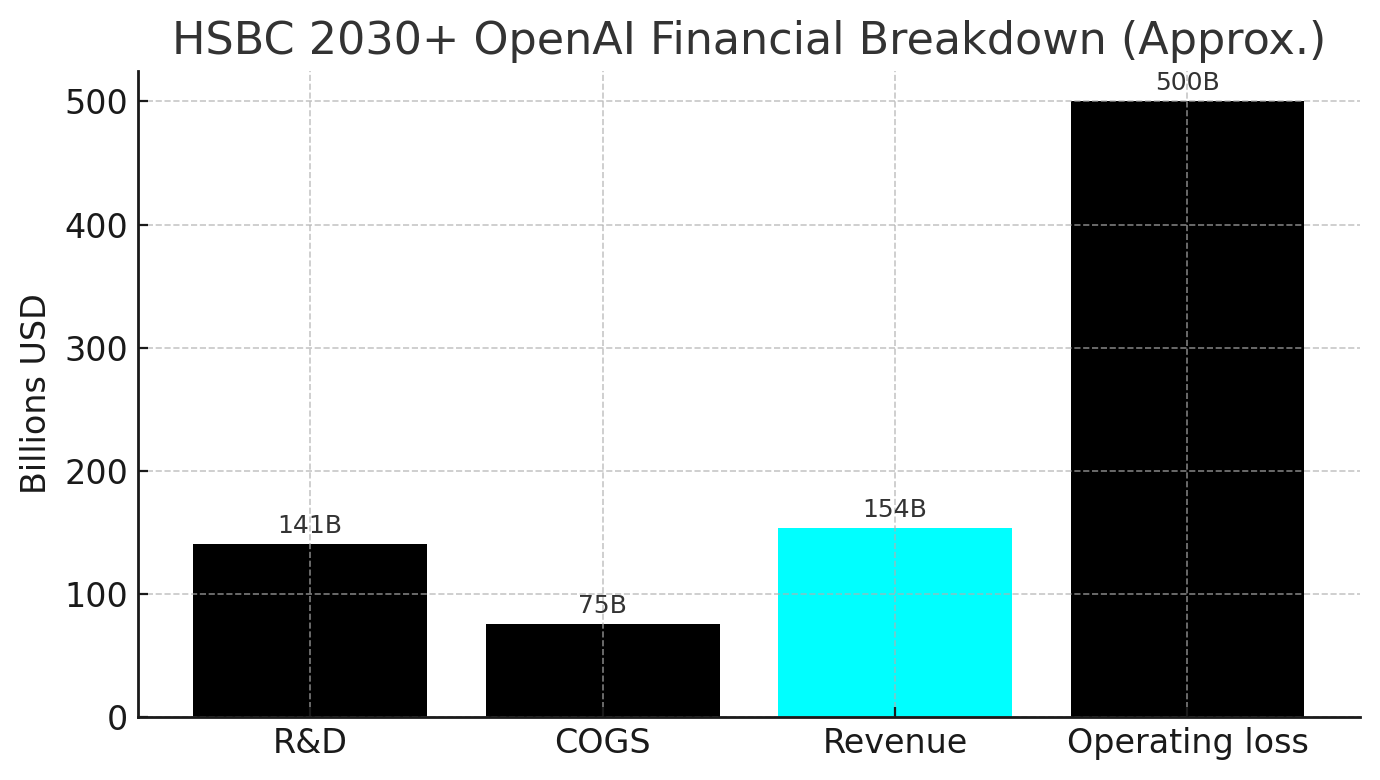

Financial modeling by HSBC suggests that without this sovereign intervention, OpenAI faces operating losses approaching $500 billion by 2030. The costs associated with training frontier models—specifically the energy consumption and hardware depreciation—have scaled faster than revenue monetization. The children of Silicon Valley, a term now used by market analysts to describe the entitlement of tech founders who assumed capital would always be free, are finding that the next phase of growth requires the balance sheet of the US Treasury rather than the risk appetite of Sand Hill Road.

This marks the transition of AI from a product to strategic infrastructure. Just as the transcontinental railroad or the nuclear power fleet could not have been built solely by unassisted private enterprise, the gigawatt-scale data centers required for the next leap in model performance—clusters consuming 5 GW or more—are effectively public works projects. Investors must recognize that companies relying solely on private funding for foundational model training face a high probability of insolvency. Value is shifting from the entities that design the models to the entities that build the state-backed infrastructure that hosts them.

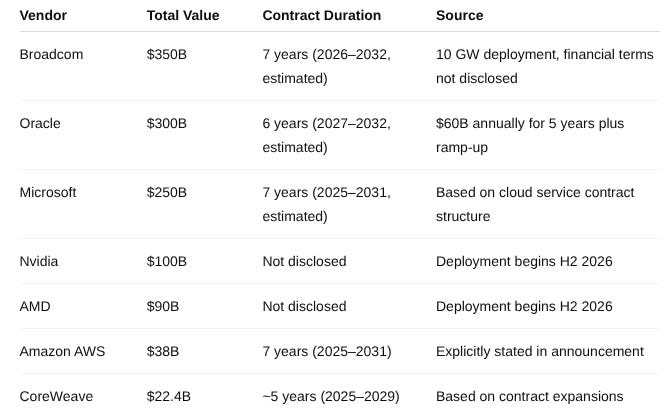

The scale of the proposed infrastructure buildout, often referred to under the codename Stargate, redefines industrial demand. Analysis of supply chain commitments reveals a spending plan allocated across seven major vendors, with Broadcom ($350 billion), Oracle ($300 billion), and Microsoft ($250 billion) absorbing the lion’s share of the capital flow between 2025 and 2035.

This infrastructure campaign is not merely about buying chips; it is about terraforming the American energy landscape. The Stargate project envisions a network of data centers that will consume vast quantities of power, necessitating a dedicated supply chain for energy generation and transmission. The document released by OpenAI in late 2025 outlines a requirement for 36 gigawatts of compute capacity by 2030. To put this in perspective, 36 GW is roughly equivalent to the total electrical generation capacity of the entire country of Argentina.

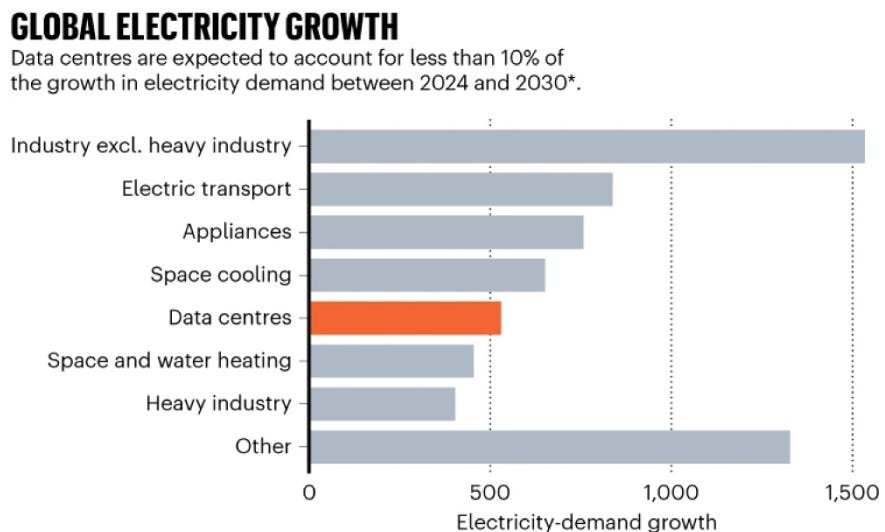

The implications for the US power grid are staggering. The Department of Energy has warned that data centers could consume up to 9% of total US electricity generation by 2030, a figure that necessitates the rapid construction of new baseload power. The Stargate initiative essentially forces the US government to become the guarantor of the energy transition, underwriting the risks of new nuclear builds and transmission lines that commercial utilities would otherwise deem too risky.

The chinese threat

The primary external driver of this US pivot to state-backed AI is the unexpected resilience and acceleration of Chinese capability. Despite the comprehensive export controls imposed by the US Department of Commerce on advanced GPUs (specifically the Nvidia H100 and Blackwell series), China has not capitulated. Instead, Beijing has changed the rules of the game from silicon efficiency to energy abundance.

Intelligence surfacing in November and December 2025 confirms that the Chinese central government has initiated a massive subsidy program for its data center sector. Local governments in energy-rich provinces—specifically Gansu, Inner Mongolia, and Guizhou—have introduced policy directives slashing electricity costs by up to 50% for data centers that utilize domestic Chinese chips, such as those manufactured by Huawei (Ascend series) and Cambricon.

By subsidizing the energy input, the Chinese state renders the technical inefficiency of its domestic chips economically irrelevant. An analyst report from The Financial Times noted that while generating a token on Chinese hardware requires 30-50% more electricity than on Nvidia hardware, the 50% subsidy effectively neutralizes the US cost advantage.

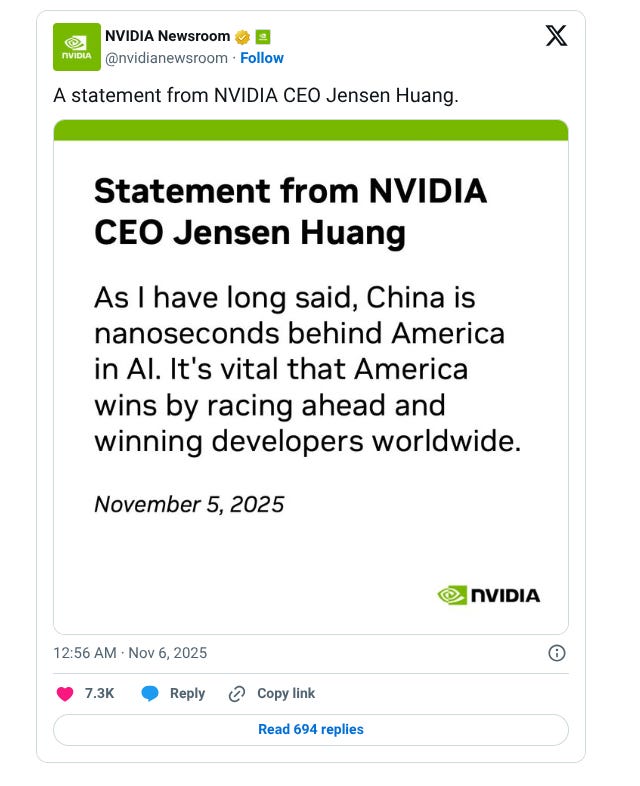

Furthermore, the velocity of infrastructure deployment in China vastly outpaces the US. Nvidia CEO Jensen Huang has starkly warned that while the US takes three to five years to permit, build, and power a new data center, China can assemble equivalent infrastructure in months. Huang’s assessment that China is “nanoseconds behind” the US in practical AI capability destroys the Western complacency that sanctions would permanently cripple the adversary. This realization is the catalyst for the US AI Action Plan, which reframes the data center buildout as a matter of national survival.

While Huang admires China’s construction speed, he’s even more concerned about energy capacity needed to support the AI boom. He noted that China has “twice the energy we have as a nation, yet our economy is bigger than theirs. It doesn’t make sense,” underscoring the challenge the U.S. faces in keeping up.

Europe: The Draghi report, regulations, the impact of the AI and capital flight

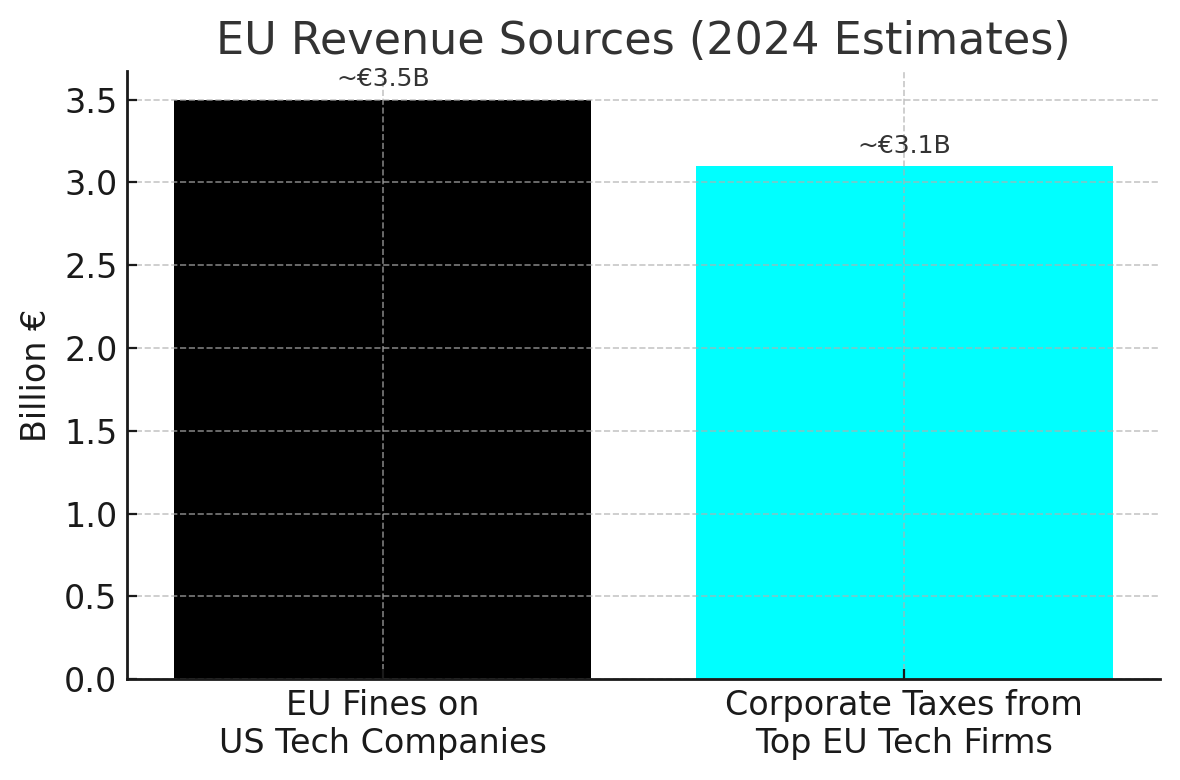

In the absence of innovation, the EU has pivoted to a business model of “regulatory extraction.” This dynamic was starkly illustrated in December 2025, when the European Commission levied a €120 million fine against X (formerly Twitter) for alleged breaches of the Digital Services Act (DSA). While the fine itself is manageable for a US tech giant, the signal it sends is catastrophic for institutional investment sentiment.

A statistical comparison, referred to in market circles as the Chart of Shame, reveals the perverse incentives of the Brussels bureaucracy:

The European Union now generates more revenue from penalizing successful American companies than it does from taxing the profits of its own technology sector. This parasitic model creates a hostile environment for foreign capital. The Draghi report itself notes that the EU has over 100 laws focused on technology and 270 regulators active in digital networks, a complexity that deters companies from operating within the bloc. If you want to delve deeper, check this out:

The implementation of the EU AI Act in 2025 has exacerbated the region’s uninvestability. Data from the App Association reveals that 60% of European small tech companies have delayed product development due to the new regulations, compared to only 44% of US companies facing similar but less draconian constraints.

The Compliance Premium required to operate in Europe—involving legal fees, audit costs, and feature downgrades—has decimated the startup ecosystem. Venture capital is fleeing the continent. European founders are increasingly relocating to the US or the UK (which has adopted a light-touch regulatory approach closer to the US model) to escape the stifling environment.

The political fallout from the X fine has also heightened the risk of a transatlantic trade war. US officials, including Vice President JD Vance and Senator Marco Rubio, have characterized the EU’s actions as attacks on American free speech and sovereignty, threatening retaliatory tariffs. For investors, this introduces a new layer of risk: holding European assets that rely on US exports or technology partnerships is now a geopolitical liability.

Europe is essentially “uninvestable” for high-growth technology portfolios in 2026. The combination of high energy costs, regulatory caprice, and demographic stagnation makes the region a “short” in global allocations. We recommend a structural underweight position in European equities, particularly in the tech and industrial sectors.

The physics of scaling: 106 GW by 2035

The central thesis for our 2026 portfolio rebalancing is that AI scaling is no longer limited by silicon availability, but by electricity availability. The US power grid is hitting a hard wall. Projections from BloombergNEF indicate that US data center power demand could reach 106 GW by 2035, a massive upward revision from previous estimates. To put this in context, the entire current installed capacity of the US grid is being challenged by a single sector’s exponential growth.

Grid congestion has become the primary bottleneck. In key data center hubs like Northern Virginia (managed by PJM Interconnection) and Texas (ERCOT), connection queues for new facilities are stretching to 3-5 years. Capacity prices in the PJM market have skyrocketed, signaling a desperate shortage of reliable baseload power. The market is screaming for electrons, and the current renewable-heavy strategy is failing to deliver the firm power required for 24/7 AI training clusters.

Given the intermittency of wind and solar, the technology industry has concluded that nuclear energy is the only scalable solution for carbon-free, always-on power. This realization has triggered a nuclear renaissance in late 2025, characterized by direct partnerships between hyperscalers and nuclear operators.

The Duane Arnold restart: In a bellwether event, NextEra Energy and Google announced a partnership in December 2025 to restart the Duane Arnold Energy Center in Iowa by 2029. This deal, which dedicates the plant’s 615 MW output to Google’s AI operations, validates the thesis that existing nuclear assets are undervalued strategic fortresses.

Small Modular Reactors (SMRs): While large plants take decades to build, the industry is betting heavily on SMRs for the 2030 horizon. Nvidia CEO Jensen Huang has publicly endorsed nuclear SMRs as essential for the future of AI, stating that data centers will eventually need to be co-located with dedicated reactors. This endorsement has sent stocks of SMR developers like Oklo (backed by Sam Altman) and NuScale Power soaring.

Government support: The Trump administration’s AI Action Plan explicitly calls for quadrupling domestic nuclear generation capacity and streamlining the Nuclear Regulatory Commission permitting process.

While nuclear represents the long-term solution, it cannot come online fast enough to meet the demand shock of 2026-2028. Consequently, natural gas has emerged as the critical bridge fuel.

Forecasts suggest that natural gas demand for power generation will rise by 3 to 6 billion cubic feet per day (Bcf/d) by 2030 solely to support data centers. Utilities are delaying the retirement of coal plants and commissioning new gas turbines to ensure grid reliability. This reality contradicts the energy transition narrative of a linear move to renewables; instead, we are seeing a power pragmatism where carbon goals are secondary to the imperative of keeping the lights on for AI.

Power generation is useless if it cannot be delivered. The physical grid infrastructure—transformers, switchgear, transmission lines—is facing its own supply chain crisis. Lead times for high-voltage transformers have extended from an average of 50 weeks in 2021 to 120 weeks in 2025.

This bottleneck creates a supercycle for companies that manufacture electrical components. Firms like Eaton Corporation, Hubbell, and Schneider Electric are effectively sold out for years, granting them immense pricing power. The grid modernization trade is no longer a government policy play; it is a corporate survival play for the world’s largest tech companies.

Copper, uranium, and critical minerals

The electrification of intelligence is metal-intensive. Every data center, every grid upgrade, and every new power plant requires massive quantities of copper. New analysis indicates that a single megawatt of data center capacity requires approximately 27 tonnes of copper for cooling systems, power distribution, and grounding.

If AI data centers reach the projected 10% of North American electricity demand within five years, the associated copper requirement will exceed 2.7 million tonnes annually for this sector alone. This demand shock is colliding with a supply crisis. Major producers like Chile’s Codelco are struggling with declining ore grades and aging infrastructure, while no new mega-mines are scheduled to come online in 2026. Investment banks like JPMorgan and UBS are forecasting copper prices to breach $12,000-$13,000 per ton by 2026.

The uranium market is undergoing a structural deficit that will define the energy landscape of the late 2020s. With major miners like Kazatomprom cutting production guidance for 2026 and Western governments banning Russian enriched uranium, the supply side is constrained just as demand explodes.

The reference scenario from the World Nuclear Association now projects reactor requirements to rise by 124% by 2040, driven by life-extensions of existing fleets and the deployment of SMRs. For investors, uranium miners represent a leveraged play on the AI energy thesis. Companies like Cameco and Kazatomprom are the gatekeepers of the fuel required for the Stargate era.

The US Department of the Interior’s update to the critical minerals list in late 2025 underscores the geopolitical urgency of securing supply chains. The list now includes 60 minerals, with a renewed focus on materials like Gallium, Germanium, and Graphite—inputs essential for semiconductors and batteries that are currently dominated by China.

The One Big Beautiful Bill, legislation passed in 2025, appropriates billions for the National Defense Stockpile to secure these minerals. This marks the return of strategic stockpiling, creating a floor under the prices of these commodities and benefitting domestic miners operating in friendly jurisdictions. Check more about this here:

Portfolio strategy 2026

Institutional portfolios enter 2026 dangerously overweight Bits (Software, SaaS, Consumer Tech) and underweight Atoms (Energy, Materials, Infrastructure). The convergence of the risks outlined above—valuation compression in software due to AI deflation, regulatory headwinds in Europe, and physical shortages in infrastructure—dictates a massive rotation.

The Trade: Sell the AI hype (unprofitable software wrappers with no moats) and buy the AI reality (the physical infrastructure required to run the models).

The following tables outline specific asset allocations recommended for the 2026 fiscal year, categorized by the themes developed in this report.

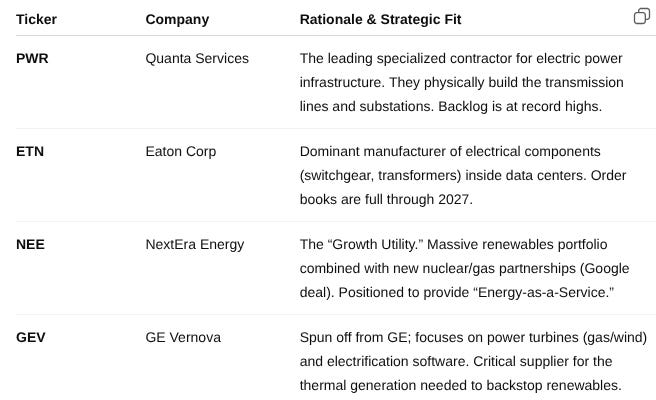

Basket A: Uranium & Generation

Rationale: Scarcity value of baseload power and hyperscaler demand for carbon-free energy.

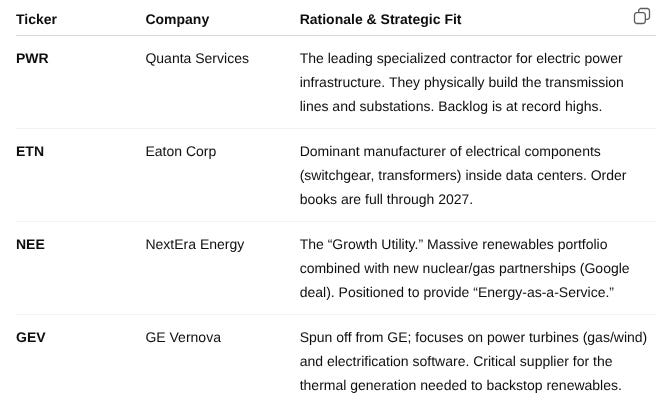

Basket B: Grid & electrical infrastructure

Rationale: The grid must double in capacity; hardware is the bottleneck.

Basket C: Cooper

Rationale: The wire of the AI revolution; structural supply deficit in 2026.

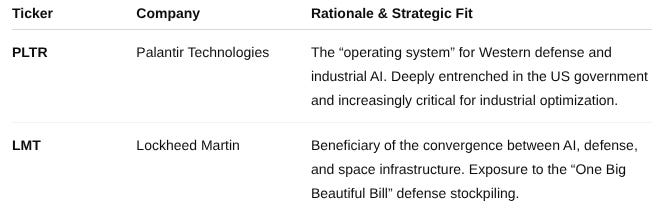

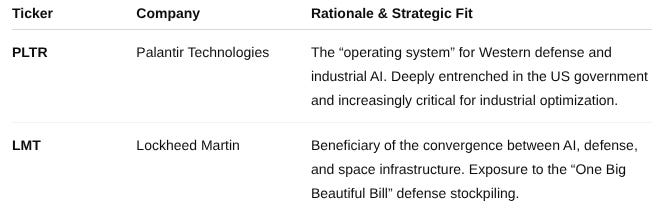

Basket D: Sovereign defense & industrial AI

Rationale: Alignment with “Sovereign AI” and US industrial policy.

What to avoid?

European tech Indices (MSCI Europe IT): Regulatory risk is unpriced. The X fine sets a precedent for arbitrary wealth extraction.

Consumer AI hardware: High risk of commoditization and reliance on complex Asian supply chains that may be disrupted.

Blind ESG funds: Many legacy ESG funds exclude nuclear and defense stocks. These funds will underperform in an era where nuclear is green and defense is necessary.

The primary risk to this physical AI thesis is inflation. A government-backed infrastructure boom of this magnitude—$1 trillion for OpenAI, billions for the grid, subsidized energy—is inherently inflationary. If the US government guarantees massive loans, it is effectively monetizing debt to compete for scarce physical resources (copper, steel, concrete). This could reignite CPI inflation, forcing the Federal Reserve to keep interest rates higher for longer, which punishes long-duration assets while benefiting the real assets recommended in this report.

The US-China tech war is escalating from decoupling to containment. The risk of China restricting exports of critical minerals (Gallium, Germanium, Graphite) remains high. Such a blockade would cause short-term chaos in the US tech supply chain but would ultimately accelerate the domestic mining thesis advocated here.