[INTEL REPORT] Market environment of mid-2025

Mid-2025 Crossroads of tariffs, tech, and liquidity

Table of contents:

Introduction.

The macroeconomic & market landscape.

De-risking or delayed reaction?

Q2 2025 earnings season in-depth.

Cross-asset signals.

Where and when to invest.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

The prevailing market environment of mid-2025 presents a study in contrasts, demanding a nuanced and highly selective investment approach. Global equity markets, particularly in the United States, have ascended to record highs , fostering a climate of apparent calm and investor complacency. This placid surface, however, belies a precarious balance. The constructive long-term narrative, underpinned by resilient corporate profitability and the transformative potential of artificial intelligence , is set against a backdrop of potent and underappreciated near-term macroeconomic risks.

The central thesis of this report is that the market is exhibiting a dangerous level of complacency toward three critical threats. First, a significant and impending liquidity drain is set to emanate from the U.S. Treasury's plan to rebuild its cash balance, a development with a historical precedent of disrupting risk assets. Second, a stark divergence has emerged between buoyant equity prices and the deeply bearish positioning of sophisticated institutional investors, or "smart money," creating an unstable "coiled spring" dynamic that portends a sharp move. Third, and most importantly, markets are failing to price in the full economic consequences of a new global tariff regime, instead clinging to the belief that political threats will inevitably be withdrawn.

Se can identify two primary market tensions. The first is an ideological clash between the market's faith in the TACO Trade and explicit, high-level government statements that the August 1st tariff deadline is firm and will not be extended. The second, more subtle tension lies in the market's reaction to recent trade agreements. While the first-order effects of deals like the U.S.-Japan accord have been celebrated, their negative second-order consequences—most notably an alarming spike in Japanese Government Bond yields—signal potential for global financial instability that is being largely ignored.

In this environment, a "barbell" strategy is the most prudent course of action. Investors should maintain strategic long exposure to durable, secular growth themes that have demonstrated pricing power and demand resilience, particularly in enterprise-focused artificial intelligence and cloud infrastructure. Simultaneously, tactical caution is warranted through the volatile August period. This involves implementing portfolio hedges, raising cash levels modestly, and preparing for binary outcomes around key event risks. Actionable ideas derived from this analysis include positioning for a potential short-squeeze in the technology sector, closely monitoring the USD/JPY exchange rate for signs of a paradigm-shifting Bank of Japan policy change, and holding a strategic allocation to gold as a hedge against a policy error or a global liquidity event.

The macroeconomic & market landscape.

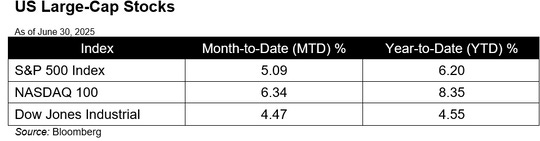

The mid-summer market session of 2025 is characterized by a deceptively quiet tone. Trading volumes have been seasonally low, consistent with the summer doldrums that have historically marked the period between the U.S. Fourth of July and Labor Day holidays. Yet, this low-volume environment has not hindered a powerful upward trend in equities. Major U.S. indices, including the S&P 500 and the Nasdaq Composite, have repeatedly set fresh all-time closing highs through July. This momentum follows a robust second quarter, during which the S&P 500 gained 10.94% and the tech-heavy Nasdaq surged an impressive 17.96%.

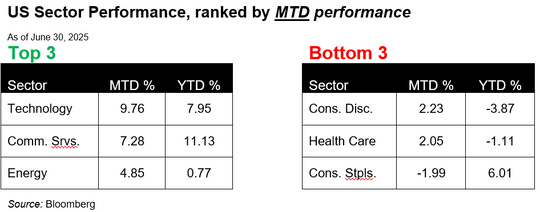

This bullish price action persists despite several well-documented headwinds. Chief among these are the historically soft seasonal patterns of August. A surface-level analysis points to August as a historically weak month for equities. However, a more granular examination of seasonal patterns reveals a critical divergence. While broad indices such as the S&P 500 and the NYSE Composite have indeed shown weakness, the technology-centric Nasdaq 100 has demonstrated historical strength during this period. This suggests that the traditional summer doldrums disproportionately affect older-economy sectors, and that any market resilience through the coming month will likely depend on continued leadership from technology. This reinforces the theme of a bifurcated market and provides a specific area of focus for relative outperformance.

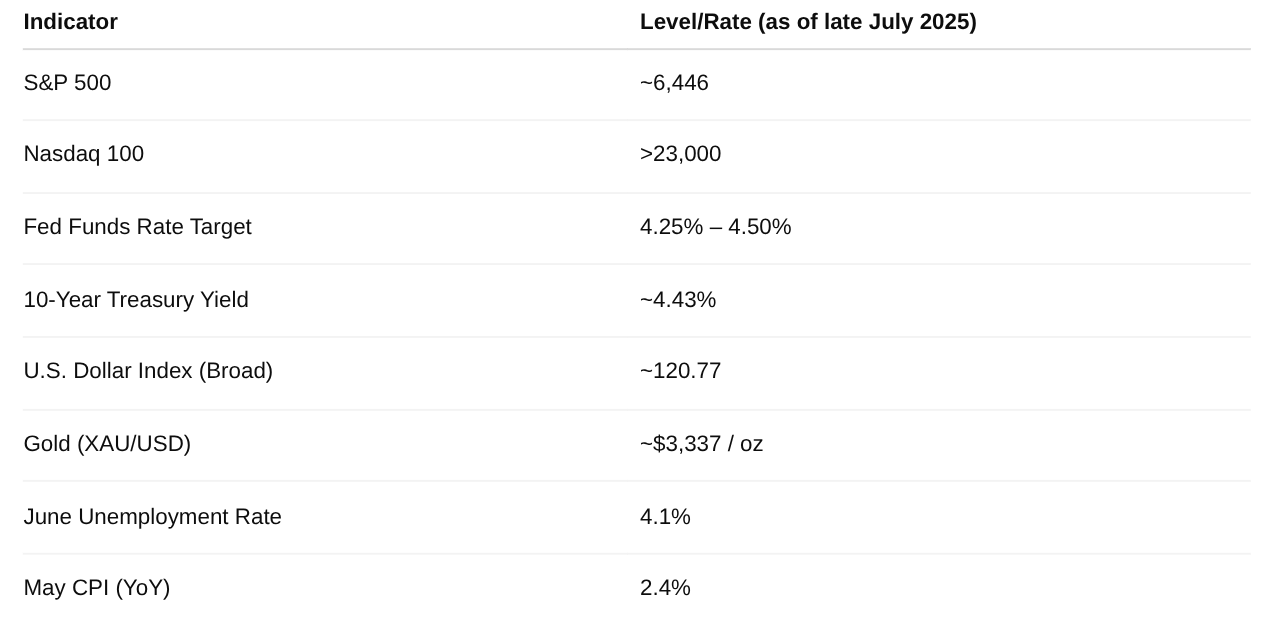

The monetary policy backdrop remains cautiously accommodative. At its mid-June meeting, the Federal Reserve maintained the federal funds rate at a target of 4.25% to 4.50%, with its updated projections still pointing toward two quarter-point rate cuts by the end of 2025. However, this consensus is fraying, with a growing minority of officials anticipating no cuts this year, viewing the current policy stance as appropriate rather than overly restrictive.

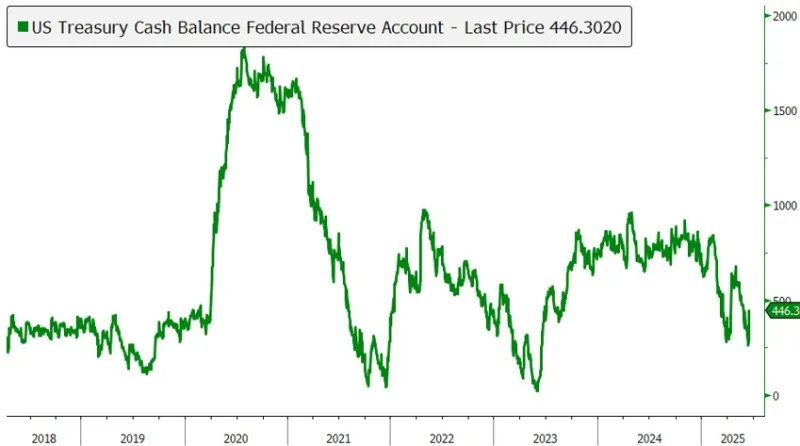

While the market remains fixated on the Fed's rate path, a more immediate and potentially disruptive factor is emerging from fiscal policy: the state of the U.S. Treasury General Account (TGA). The TGA, which is the Treasury's primary checking account held at the Federal Reserve, is set to be replenished on a massive scale. After closing at approximately $349 billion on July 24, 2025 , the Treasury's own financing estimates assume an end-of-September cash balance of $850 billion. This implies a net liquidity withdrawal of over $500 billion from the financial system in the coming two months. Take a look of this presentation to know more:

Historically, such rapid increases in the TGA balance, which are achieved by issuing more government debt and pulling cash out of the private sector, have acted as a form of reverse QE and have often coincided with sharp equity market drawdowns and periods of financial stress. This process effectively drains liquidity from the system, tightening financial conditions.

However, the ultimate market impact is not determined solely by the size of the TGA increase, but by the source of the funding. A critical distinction must be made between liquidity drawn from the Federal Reserve's Overnight Reverse Repurchase (ON RRP) facility versus liquidity drawn directly from commercial bank reserves. If money market funds, which are major participants in the ON RRP facility, use their excess cash to purchase newly issued Treasury bills, the effect on banking system liquidity is largely sterilized. This represents a simple transfer on the Fed's liability sheet—a decrease in ON RRP balances offset by an increase in the TGA balance—with minimal impact on the reserves available to the banking system. Conversely, a TGA replenishment that directly drains reserves from commercial banks constitutes a direct and potent tightening of financial conditions, reducing the capacity for lending and risk-taking. Therefore, monitoring the Fed's weekly H.4.1 statistical release for changes in bank reserves alongside the TGA and ON RRP balances is paramount for assessing the true liquidity impact in the coming weeks. A rising TGA funded by a falling ON RRP balance is manageable; a rising TGA funded by falling bank reserves is a significant red flag.

A significant and troubling divergence has emerged between the market's bullish price momentum and the positioning of its most key participants. As noted in the initial query, hedge funds have aggressively increased their net short positions in equity futures to the highest levels since the first quarter of 2025. This is confirmed by the latest data from the Commodity Futures Trading Commission. The CFTC's Commitment of Traders report for the week ending July 18, 2025, showed that "non-commercial" traders—a category primarily composed of large speculators like hedge funds and Commodity Trading Advisors—held net short positions in S&P 500 futures totaling -167,800 contracts. This bearish stance intensified further in the subsequent report for the week ending July 25, with net shorts increasing to -168,500 contracts.

This deeply pessimistic positioning stands in stark contrast to the S&P 500's ascent to new all-time highs, creating a coiled spring scenario with two clear potential outcomes. The first possibility is that the smart money is correct. Their short positions may be a calculated bet that the confluence of macro risks—the impending TGA liquidity drain, the unpriced impact of tariffs, and negative August seasonality—will finally catalyze a long-overdue market correction.

The second, equally plausible outcome is that these funds are caught offside. Should a positive catalyst emerge, such as a favorable resolution to the tariff standoff or a series of blowout tech earnings, these large short positions would be vulnerable to a painful squeeze. Forced buying to cover losing short bets could ignite a cascade effect, propelling the market higher momentum-driven rally. The sheer magnitude of the net short position means the potential energy for such a squeeze is exceptionally high. This divergence does not, therefore, serve as a simple signal to go short alongside the hedge funds. Rather, it signals that volatility is underpriced and that the market is primed for a sharp, decisive move in one direction or another. The primary catalysts to watch are the resolution of the August 1st tariff deadline and the ongoing big-tech earnings reports.

De-risking or delayed reaction?

The disconnect between market pricing and economic reality is starkly illustrated by a detailed analysis from the Yale Budget Lab, which quantifies the potential damage from the tariffs implemented and threatened in 2025. The study's findings, which appear to be largely ignored by investors, paint a grim picture: