[INTEL REPORT] Jobs, rates, trends

Repricing interest rates and reshaping market fundamentals

Table of contents:

Introduction.

The U.S. labor market.

Federal Reserve policy pivot.

Equity market response.

Unpacking sector rotation and valuation dichotomies.

The tariff tightrope and global trade flows.

Strategic recommendations for Q3 2025.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

Entering Q3 2025, investors are facing a uniquely landscape shaped by diverging economic indicators and shifting policy expectations. At the heart, lies the U.S. labor market, whose unexpected resilience has systematically defied persistent recession forecasts. This resilience has fundamentally reshaped expectations around monetary policy, compelling investors to recalibrate their strategies to manage increased uncertainty and volatility.

The quarter opened with a notable disparity between employment data sources, presenting a puzzle for analysts. The private-sector contraction reported by ADP contrasted sharply with robust job gains from the Bureau of Labor Statistics, reflecting deeper structural divergences within the economy. Notably, strength has predominantly originated from non-cyclical sectors such as government and healthcare, providing critical stabilization against underlying weakness in cyclical private industries.

Compounding this complexity, wage growth has remained firm yet moderate, carefully threading a needle between economic stability and inflationary pressure. This nuanced wage dynamic has reinforced the Federal Reserve’s cautious posture, substantially diminishing prospects for imminent rate cuts. As a consequence, financial markets have swiftly adjusted, embracing a "higher for longer" interest rate outlook.

Remarkably, equity markets have responded positively to these tighter monetary conditions, challenging conventional wisdom regarding market reactions to hawkish central bank stances. Robust employment conditions and moderate wage growth have fostered broad-based optimism, notably boosting performance among domestically oriented small-cap stocks. This shift signals investor sentiment transitioning away from defensive recession hedging toward expectations of a sustained economic expansion.

A significant market rotation is also underway as investors actively reduce exposure to overvalued mega-cap growth equities, diversifying into more attractively priced small- and mid-cap cyclical names. This rotation reflects heightened awareness of valuation risks and a strategic realignment with sectors likely to benefit directly from continued economic resilience.

Globally, however, trade policy continues to present substantial uncertainty. The recently announced U.S.-Vietnam trade agreement exemplifies an increasingly tactical approach aimed at recalibrating global supply chains and tariff dynamics. With a critical tariff truce nearing expiration, the outlook for global trade introduces elevated risks and potential volatility into market forecasting.

Commodity markets offer a further divergence in narrative, with gold maintaining a defensive equilibrium supported by persistent central bank accumulation, yet capped by dollar strength and elevated interest rate expectations. Silver, meanwhile, has emerged as a compelling bullish story driven by seasonality, technical signals, and relative undervaluation, possibly heralding broader shifts in macroeconomic expectations among commodity investors.

Collectively, these multifaceted dynamics signal a pivotal transition for financial markets from liquidity-driven to fundamentally-driven regimes. Navigating this transition effectively requires investors to adopt a nuanced understanding of the interplay between domestic economic strength, monetary policy, and global risk factors. This report provides an analytical framework and actionable recommendations to adeptly manage these critical crosscurrents and leverage emerging opportunities.

The U.S. labor market

The U.S. economic data for the third quarter of 2025 has been decisively shaped by the June employment data. At first glance, we see a contradictory picture of the labor market, ultimately revealing a resilient economy that has defied recessionary fears, albeit with notable underlying divergences. This resilience is the primary factor behind the significant shift in monetary policy expectations and subsequent market reactions. If you want to know more, check this document:

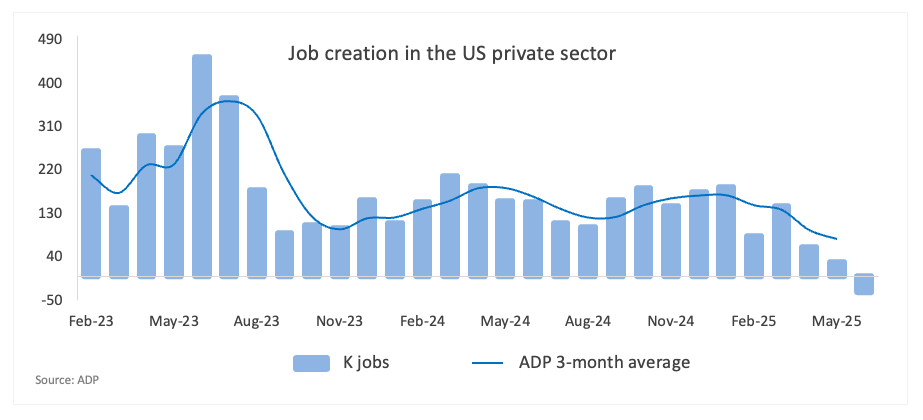

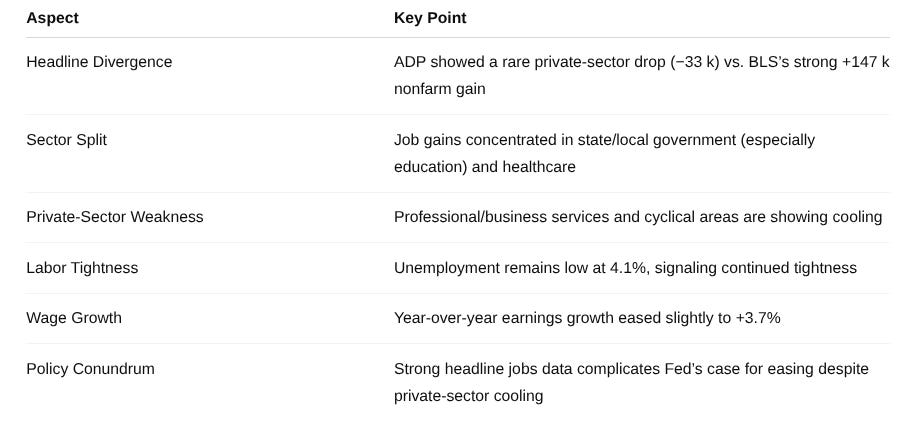

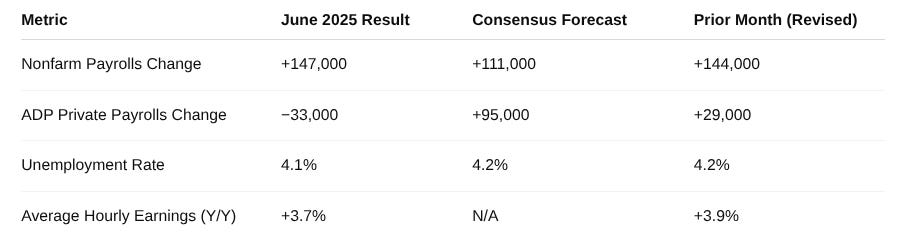

The week's key economic releases presented a puzzle for investors. On July 2, 2025, the ADP National Employment Report indicated a surprise contraction, showing that private sector employment shed 33,000 jobs in June. This result was a stark reversal from the previous month's revised gain of 29,000 and fell dramatically short of economists' forecasts for a 95,000 job gain. The ADP report, which draws on payroll data from over 25 million U.S. employees, pointed to a clear slowdown in the private sector, with ADP's chief economist noting that a hesitancy to hire and a reluctance to replace departing workers led to job losses. This was the first decline reported by ADP in over two years, sparking initial concerns about the health of the U.S. economy.

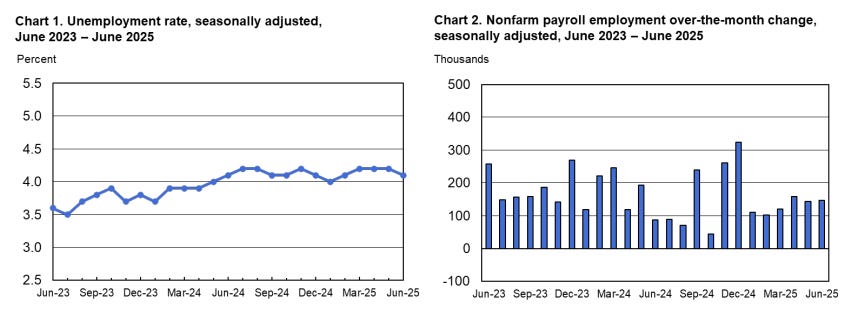

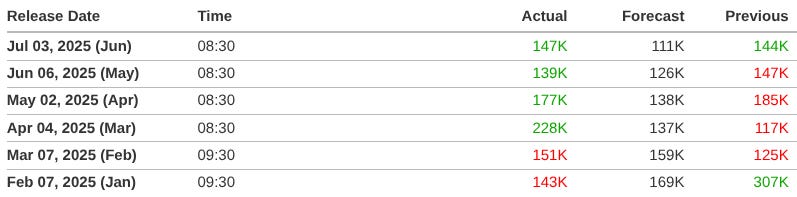

However, just one day later, on July 3, the official Bureau of Labor Statistics Employment Situation Summary delivered a much stronger message. The headline Nonfarm Payrolls figure showed a net gain of 147,000 jobs in June, comfortably beating the consensus forecast of 111,000. Furthermore, the unemployment rate ticked down slightly to 4.1%, remaining within the narrow 4.0% to 4.2% range it has occupied for over a year. The BLS also revised the figures for the prior two months upward by a combined 16,000 jobs, adding to the report's positive tone. This well-documented potential for divergence between the two reports underscores that they measure the labor market through different methodologies, with the government-led BLS survey providing a broader picture that includes public sector employment.

A granular analysis of the NFP data reveals that the headline strength was not evenly distributed across the economy. Instead, it was heavily concentrated in non-cyclical, government-funded sectors, which provided a powerful backstop that masked softness elsewhere.

The government sector was the primary engine of job creation in June, adding a robust 73,000 positions. This surge was driven almost entirely by hiring at the state and local levels, particularly in education. State government employment increased by 47,000, with 40,000 of those jobs in state government education. Similarly, local government employment trended up, adding 23,000 jobs in education. In contrast, the federal government continued to shed jobs, losing 7,000 positions in June, contributing to a total decline of 69,000 since its recent peak in January 2025.

The healthcare sector also remained a bastion of consistent growth, adding 39,000 jobs in June, a figure in line with its average monthly gain of 43,000 over the prior 12 months. Gains were notable in hospitals (+16,000) and nursing and residential care facilities (+14,000). The closely related social assistance sector added another 19,000 jobs.

This composition is critical. The strong headline NFP number was propped up by sectors that are less sensitive to the economic cycle and changes in interest rates. The weakness reported by ADP in private sector areas like professional and business services (-56,000) and its conflicting reading on education/health services (-52,000) highlights a two-tiered labor market. While the private, cyclical part of the economy shows signs of fatigue, the non-cyclical public and quasi-public sectors are demonstrating significant strength. This dynamic creates a policy conundrum for the Federal Reserve, as the robust headline figure makes it difficult to justify monetary easing, even if the underlying private sector is cooling.

The wage component of the jobs report further complicates the picture for the Federal Reserve. Average hourly earnings for all private nonfarm employees rose by 8 cents, or 0.2%, in June to $36.30. Over the past 12 months, average hourly earnings have increased by a solid 3.7%. While this pace of wage growth is not accelerating in a way that would trigger alarm about a wage-price spiral, it is firm enough to give the Fed pause. Combined with a resilient headline jobs number and a low unemployment rate, this steady wage pressure provides little justification for the central bank to rush into rate cuts, reinforcing the "higher for longer" interest rate narrative that has gained traction in markets.

Federal Reserve policy pivot

The robust June Nonfarm Payrolls report acted as a catalyst, triggering an immediate and dramatic repricing of Federal Reserve policy expectations across financial markets. The data effectively extinguished any lingering hopes for a rate cut at the upcoming July meeting, forcing investors to recalibrate their outlook for the path of monetary policy for the remainder of 2025 and beyond. This pivot reflects a crucial shift in the market's perception of the Fed's reaction function, raising the bar for future easing.

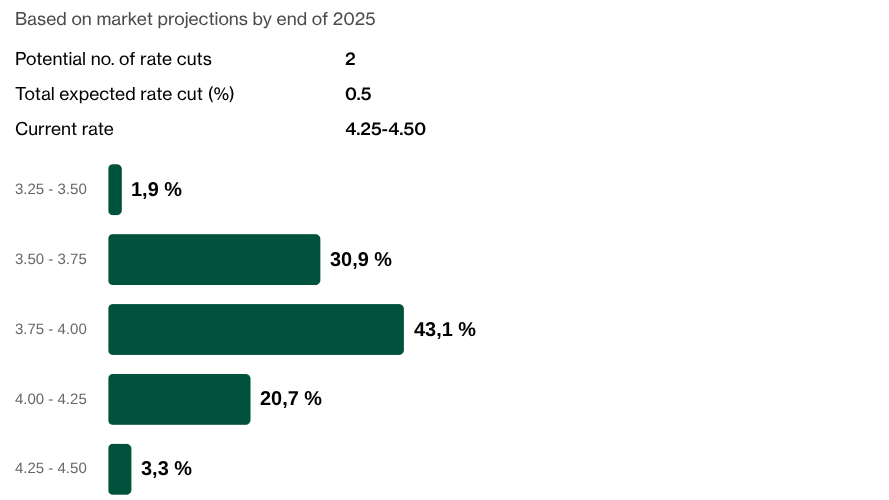

In the moments following the 8:30 a.m. ET release of the jobs data on July 3rd, interest rate futures markets moved swiftly to price out the possibility of a near-term rate cut. According to data from the CME FedWatch Tool, which analyzes 30-Day Fed Fund futures prices to derive market-implied probabilities, the odds of a 25-basis-point cut at the July 30, 2025, FOMC meeting collapsed.

As of July 7th, the probability of the Fed maintaining the target rate in its current 4.25% - 4.50% range at the July meeting stood at an overwhelming 93.6%. Correspondingly, the probability of a cut to a 4.00% - 4.25% range fell to just 6.4%. This marks a stunning reversal from just one week prior, when the market was pricing in a more than 20% chance of a July cut. The strong employment figure, combined with persistent wage growth, removed the primary justification for a precautionary or insurance cut, which some market participants had anticipated to preempt a potential economic slowdown. With the labor market demonstrating clear resilience, the impetus for the Fed to act imminently has vanished.

With a July cut now firmly off the table, the market's focus has shifted to the subsequent FOMC meetings later in the year. The consensus has coalesced around the September 17, 2025, meeting as the most likely starting point for a potential easing cycle.