Table of contents:

Introduction.

Inflation and the FED.

Nvidia's dominance and the U.S.-China policy pivot.

Market internals and technical structure.

Capital flows and sector divergence.

Factors and asymmetric opportunities.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

In a market environment defined by the loss of traditional long-term macroeconomic anchors, U.S. equities are demonstrating resilience, forcing investors to focus on the here and now. This strength is not born from a disregard for risk, but from a rational focus on a singular secular growth theme: Artificial Intelligence.

This AI-centric narrative is currently overriding near-term headwinds from complex inflation data and geopolitical uncertainty. The primary catalyst de-risking the market's growth engine has been a pivotal and unexpected policy shift by the Trump administration, which has granted approval for Nvidia to resume sales of its H20 AI chips to China. This move, part of a larger strategic negotiation involving rare earth materials, has removed a significant overhang for the tech sector, reinforcing bullish sentiment and explaining the Nasdaq's persistent strength.

This policy development provides a firm fundamental basis for the market's advance, allowing it to look past a nuanced June Consumer Price Index report. While headline inflation ticked up, driven partly by tariff-exposed goods, the underlying core inflation metrics continued a disinflationary trend, keeping the possibility of a September Federal Reserve rate cut alive but reducing its certainty. This complex macroeconomic picture supports a modestly pro-risk stance rather than an indiscriminate rush into all assets.

The market's internal structure confirms the rally's durability. Technical indicators for major indices remain bullish, with the S&P 500 and Nasdaq 100 charting new highs. Critically, aggregate investor positioning in the S&P 500 has not kept pace with the price rally since its February peak, suggesting a significant amount of sidelined capital could be forced into the market, fueling further gains.

This, combined with elevated short interest, creates a high potential for short squeezes that could amplify upward moves. Furthermore, a clear and targeted rotation of capital is underway. Analysts are revising Capital Expenditure (CapEx) forecasts sharply upward for AI-related sectors while trimming them for non-AI areas like traditional communication services, indicating a focused, thematic investment trend rather than a broad cyclical upswing.

Inflation and the FED

The current market environment is defined by a series of conflicting economic signals. While certain data points suggest inflationary pressures and potential economic slowing, a deeper analysis reveals a more nuanced reality that explains the market's ability to look past negative headlines and focus on underlying strengths.

The latest inflation data from the U.S. Bureau of Labor Statistics requires careful dissection to understand its true implications for monetary policy and asset prices.

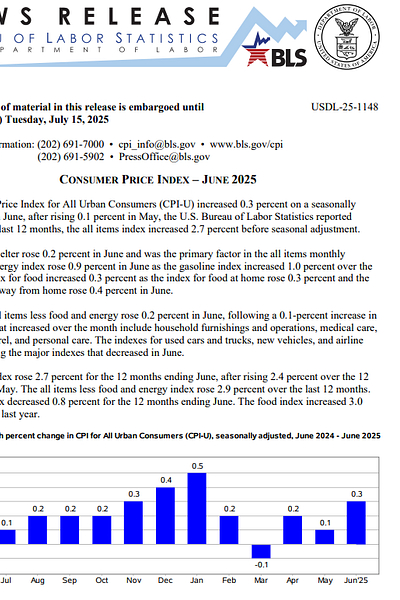

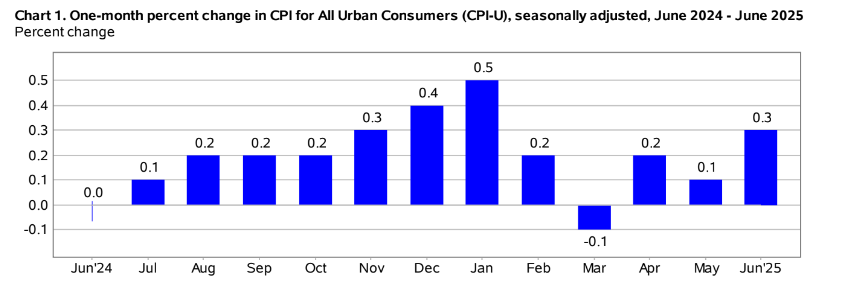

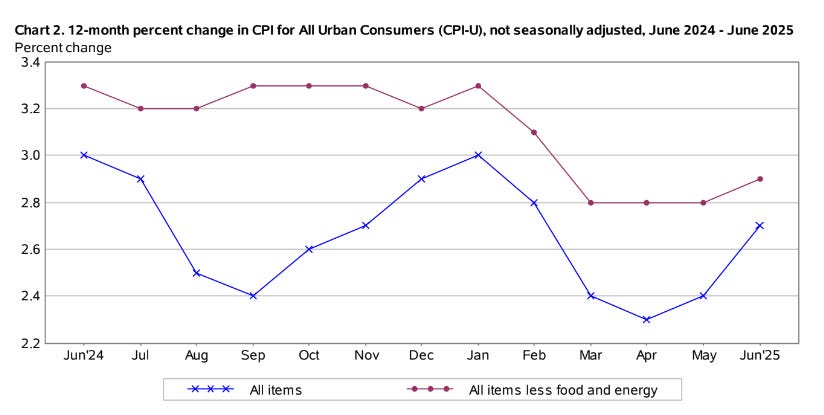

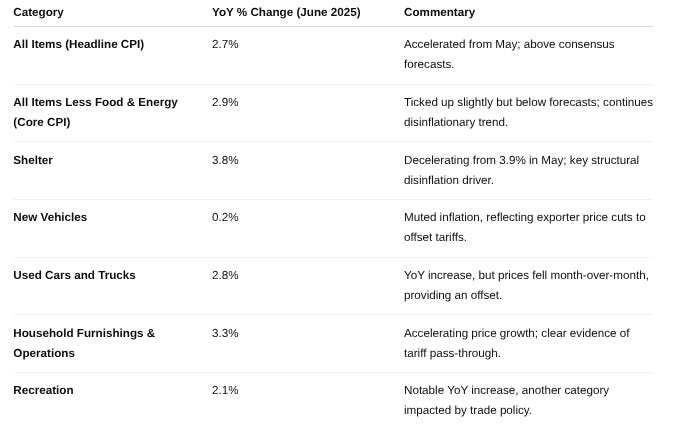

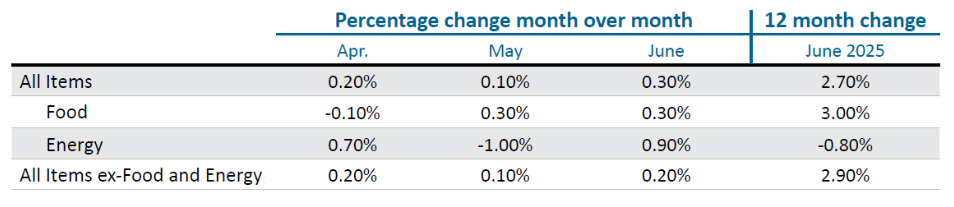

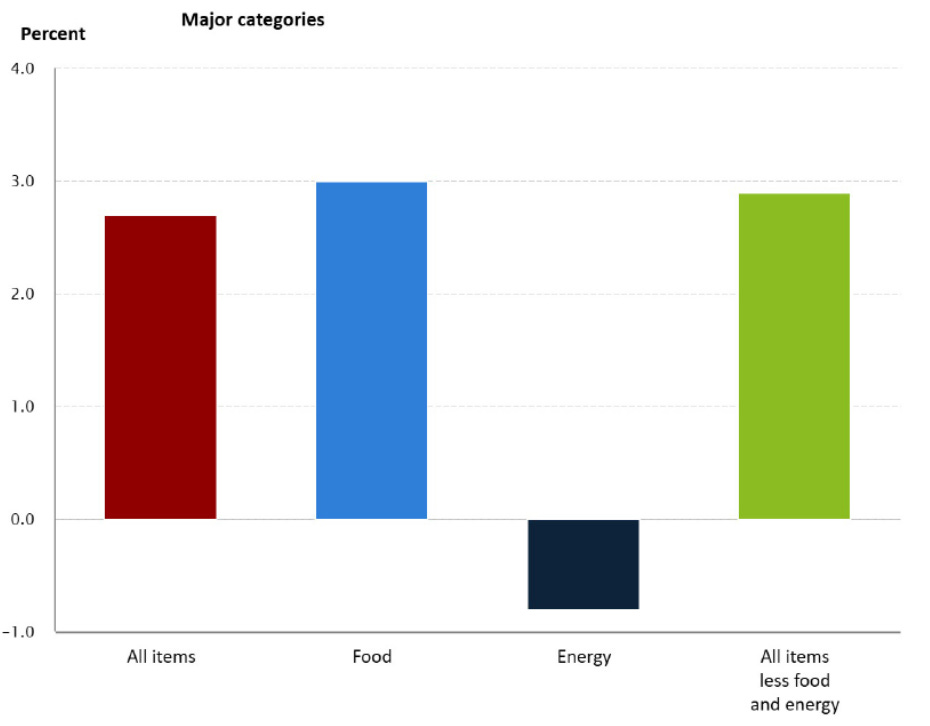

The headline Consumer Price Index for All Urban Consumers rose 0.3% month-over-month (MoM) in June, an acceleration from the 0.1% rise in May. On a year-over-year (YoY) basis, headline inflation increased to 2.7%, the highest reading since February and above consensus forecasts of 2.6%. This uptick reversed several months of cooling inflation and, on the surface, presents a challenge to the disinflation narrative.

However, the core CPI, which excludes volatile food and energy prices and is more closely watched by the Federal Reserve, tells a different story. Core CPI rose just 0.2% MoM, marking the fifth consecutive month it has come in below expectations. The annual core rate edged up to 2.9% from May's 2.8% but was below the 3.0% market forecast, continuing a broader disinflationary trend. This divergence between a hotter headline and a cooler core is central to the market's interpretation. The market's resilience is not a sign of ignoring bad news, but rather a rational assessment that the underlying, persistent inflation drivers are moderating, while the sources of headline pressure are more isolated and policy-driven.

The shelter component, which is the largest single category within the CPI, rose 0.2% MoM and 3.8% YoY. While it was a key contributor to the monthly increase, its annual rate of increase has decelerated from 3.9% in May, confirming a continued cooling trend in this crucial, slow-moving component.

In contrast, the impact of recent tariffs is becoming visible in specific goods categories. The index for household furnishings and operations rose a notable 1.0% MoM and 3.3% YoY, while recreation goods prices were up 2.1% YoY. This suggests that policy, rather than broad-based economic overheating, is responsible for pockets of inflation. The Federal Reserve is more likely to look through these identifiable, policy-induced price shocks, especially as they are not spilling over into the core services trend.

A key counter-narrative to tariff-driven inflation is unfolding in the automotive sector. In a bid to protect their U.S. market share following a 25% tariff hike, major Japanese automakers have aggressively cut their factory-gate export prices by nearly 20%. This strategic pricing has had a direct deflationary effect on U.S. consumer prices, with the index for new vehicles falling 0.3% MoM and used cars and trucks declining 0.7% MoM. This deflation in a major consumer durable category has helped to offset some of the inflationary pressures seen in other tariff-exposed goods.

The nuanced inflation data creates a delicate balancing act for the Federal Open Market Committee. The persistence of headline inflation above the 2% target makes an aggressive easing cycle unlikely in the immediate future.

Despite this, futures markets continue to price in a significant probability of a rate cut before year-end. As of mid-July, the odds of at least one 25 basis point cut by the September 17th FOMC meeting stand at approximately 61.5%. While this is down from near-certainty in previous weeks, it remains the market's base-case scenario. Concurrently, the probability of the Fed holding rates steady has risen to a non-trivial 38.5%, encapsulating the market's current state of uncertainty. The next FOMC meeting on July 29-30 is expected to produce a statement that is highly cautious and data-dependent, reinforcing that the committee's decisions will be guided by monetary policy objectives, not fiscal developments like tariffs.

For much of the past year, a notable divergence has existed between soft economic data, such as consumer and business sentiment surveys which have been weak, and hard economic data, such as inflation and employment reports which have remained resilient. This gap now appears to be closing. Recent hard data points, including the downside surprise in core CPI and a disappointing retail sales report in May, are beginning to align with the pessimism long expressed in sentiment surveys.

This convergence is reflected in the Citigroup Economic Surprise Index, which measures data outcomes relative to consensus expectations. As of July 17, the index stood at a moderately positive 12.3, indicating that recent data is no longer surprising to the upside as consistently as it had been. This alignment suggests the economy is likely entering a phase of slower growth. Paradoxically, this can be bullish for risk assets, as it strengthens the case for a preventative Fed rate cut while diminishing fears of an economic overheating that would necessitate further tightening.

Nvidia's dominance and the U.S.-China policy pivot

While the macroeconomic backdrop is complex, the equity market's primary driver is a singular force: the artificial intelligence revolution, with Nvidia at its epicenter. A recent and unexpected shift in U.S. trade policy has served as a major catalyst, reinforcing Nvidia's central role and providing a firm foundation for the market's risk appetite.

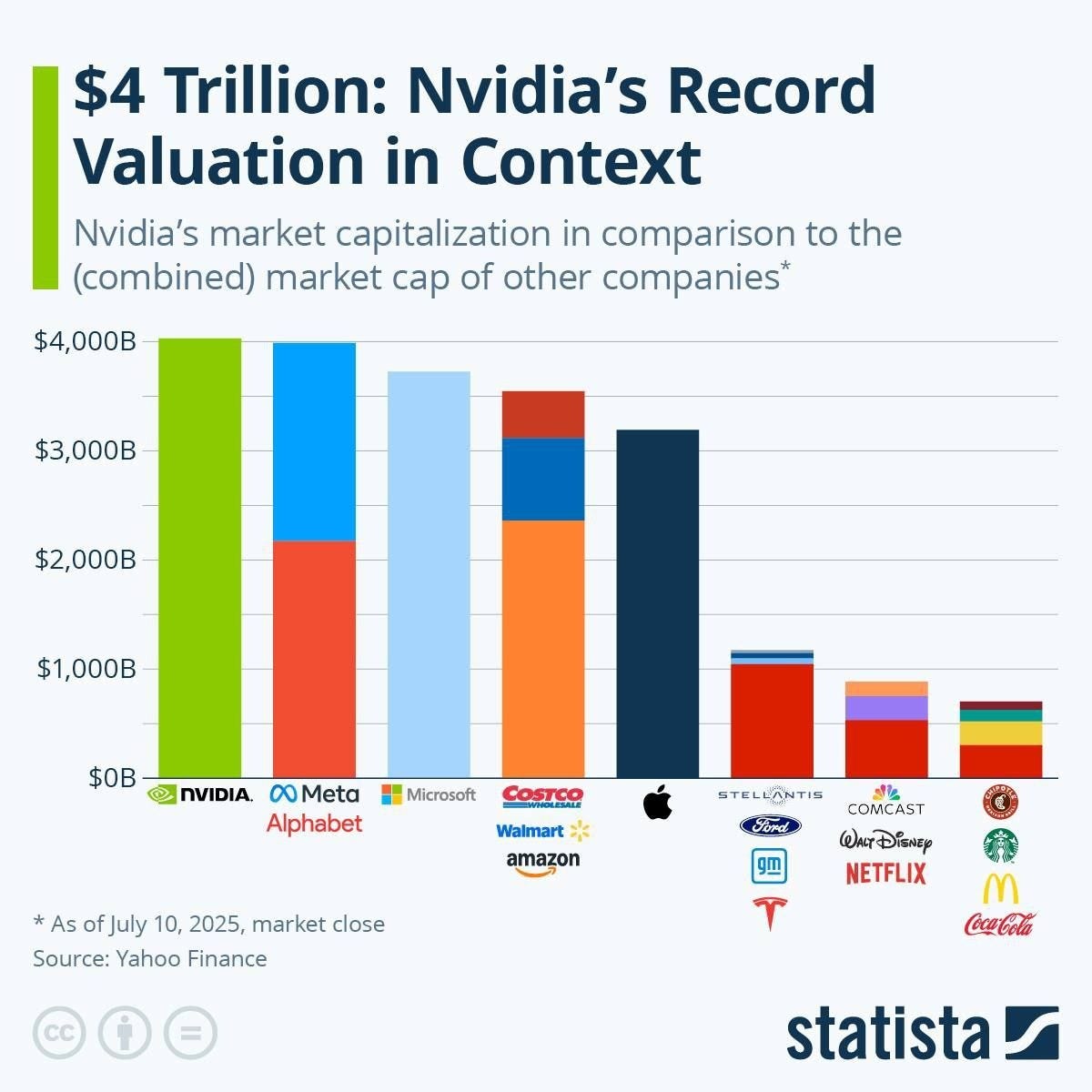

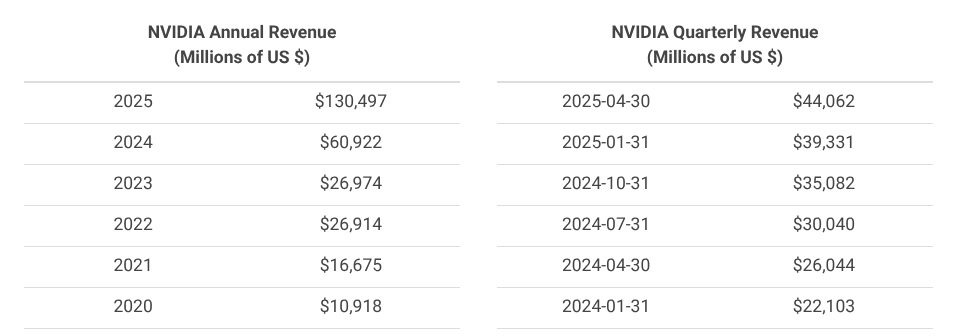

Nvidia's ascent has been historic. In early July 2025, it became the first public company in history to achieve a $4 trillion market capitalization, a milestone that underscores its critical importance to the global economy. This valuation surpasses the GDP of major economies like Japan and India and is greater than the combined value of the entire Canadian and Mexican stock markets.

This valuation is built on the company's foundational role in the AI ecosystem. Its graphics processing units are the essential hardware powering the development and deployment of AI models across every major technology firm, including Microsoft, Google, Amazon, and Meta. This has translated into explosive revenue growth and a stock price that has rebounded over 88% from its tariff-induced lows in April 2025. As a result, Nvidia now constitutes over 7.5% of the S&P 500 index, making its performance a key determinant of the broader market's direction.

The primary risk factor for Nvidia and the broader semiconductor industry has been geopolitical tension, specifically U.S. export controls aimed at limiting China's access to advanced technology. These restrictions created a significant revenue headwind, with Nvidia previously warning of a potential multi-billion dollar impact.

In a pivotal policy shift in July 2025, the Trump administration announced it would begin approving licenses for Nvidia to resume sales of its H20 AI chips to China. The H20 is a specialized chip designed to comply with U.S. export rules but had nonetheless been blocked from sale in April. This reversal is not an isolated decision but part of a larger strategic negotiation. Commerce Secretary Howard Lutnick confirmed that the move is directly linked to a trade deal securing U.S. access to China's supply of rare earth materials, which are essential for American manufacturing in sectors from defense to consumer electronics.

The implications of this policy pivot are pretty important. First, it de-risks the entire AI investment theme by removing a major source of geopolitical uncertainty that had been an argument for bears. This has an immediate positive effect on the tech-heavy Nasdaq 100, where Nvidia and its ecosystem carry significant weight.

Second, it unlocks a substantial revenue stream. China is home to half of the world's AI researchers, and its technology giants are key customers for AI hardware. The resumption of sales is a direct fundamental catalyst for Nvidia's earnings growth.

Most importantly, this development provides a powerful, fundamental justification for the market's advance, allowing investors to look past the ambiguous macroeconomic data. The primary risk to the high-valuation tech sector was a combination of a hawkish Fed and geopolitical disruption. With the geopolitical risk now significantly mitigated, the market has a stronger foundation to withstand uncertainty around the Fed's next move. This reduction in the geopolitical risk premium effectively acts as a countervailing force to monetary policy uncertainty, allowing the tech sector to sustain higher valuation multiples and explaining its remarkable resilience.