[INTEL REPORT] Geopolitical situation in Late 2025

Investment strategy outlook (December 27, 2025)

Table of contents:

Introduction.

Russia-Ukraine war.

U.S.-Venezuela tensions.

U.S.-China rivalry over Taiwan.

Implications for markets, energy, inflation, and stability.

Geopolitical risks.

Macroeconomic risks.

2026 outlook scenarios.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

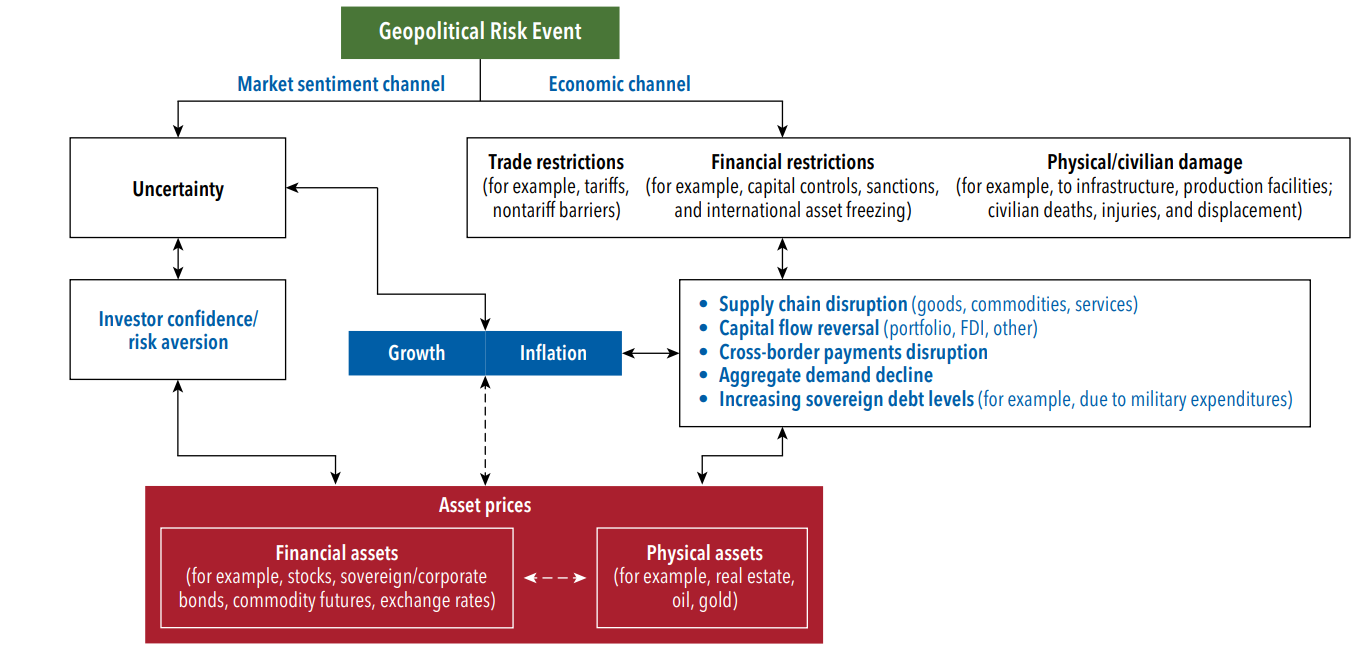

Geopolitics has become a first-order input into portfolio construction going into 2026, not a background narrative. Late-2025 conditions are defined by a set of conflicts and strategic rivalries that are simultaneously persistent (dragging on confidence and investment) and capable of abrupt escalation (creating discontinuous price moves). For investors, the practical challenge is to manage exposure to a changing distribution of outcomes—where small shifts in probabilities can drive large changes in risk premia, correlations, liquidity, and the relative performance of asset classes.

A useful way to frame the current environment is through transmission channels. Geopolitical shocks typically reach markets through energy and broader commodity pricing, inflation expectations and the policy reaction function, trade, tariffs, and supply-chain constraints, financial conditions and risk appetite, and regional stability and fiscal trajectories. These channels interact: a commodity spike can reawaken inflation at the same time that confidence weakens, producing a stagflationary mix; sanctions or blockades can fragment trade flows, raising costs and volatility even if headline growth remains positive; and fiscal demands linked to defense, subsidies, or industrial policy can reshape bond-market dynamics and term premia.

The information ahead organize the investment problem around three active theatres—Russia–Ukraine, U.S.–Venezuela, and U.S.–China/Taiwan—and then connect them to market implications for risk sentiment, energy balances, inflation paths, and stability. The objective is to move toward decision structure:

What conditions define a base case.

What developments would constitute a regime shift.

Which portfolio sleeves historically provide resilience or convexity when those shifts occur.

That structure is especially important because diversified portfolios can behave very differently across regimes: in some environments, duration hedges equity drawdowns; in others, inflation risk can cause equities and bonds to weaken together.

Baseline assumptions for 2026 growth and inflation are grounded in late-2025 institutional projections and then stress-tested under alternative geopolitical and policy paths. Check more about this here:

Market outcomes, however, depend not only on the shock itself but on amplification mechanisms—liquidity conditions, leverage, funding fragilities, and confidence dynamics that can turn a risk event into a broader repricing across assets and geographies. Check more about this here:

With these anchors in place, the analysis proceeds from the specific to the general: it begins with the three geopolitical theatres, then maps their market channels, then consolidates the risk inventory (geopolitical and macro), and finally lays out 2026 scenarios that investors can use to decide when the portfolio should remain stable, when it should rotate defensively, and when it should shift toward opportunities created by de-escalation.

Russia-Ukraine war

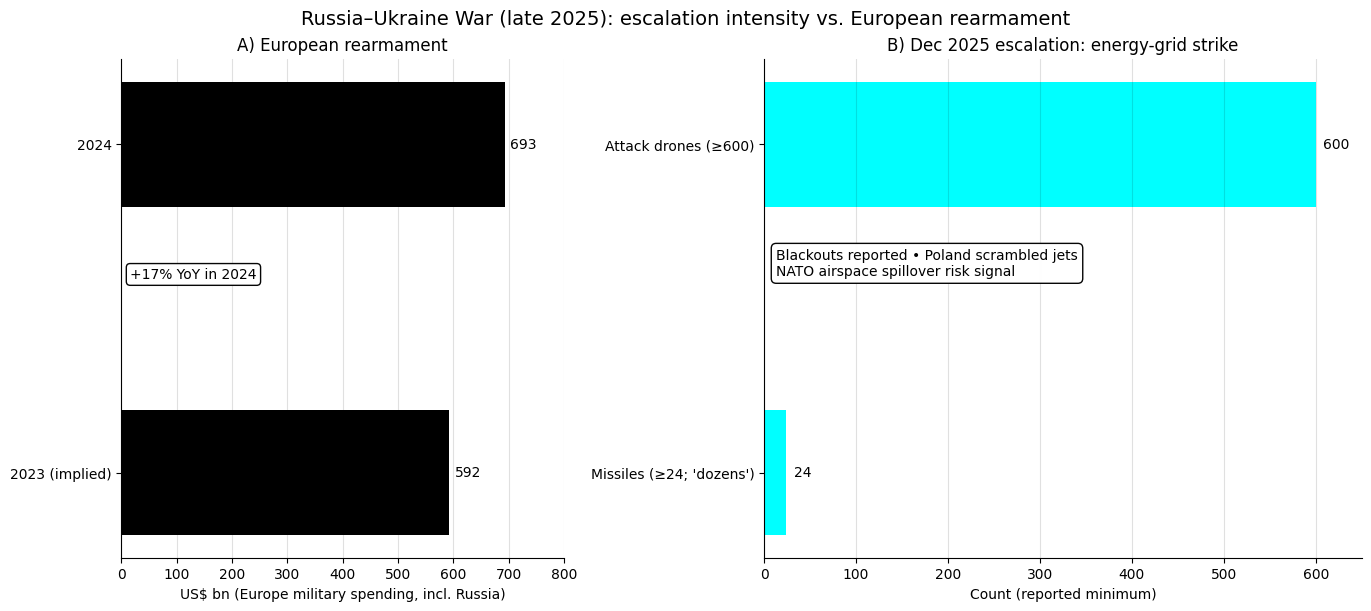

Russia’s invasion of Ukraine, now nearing its fourth year, remains a central source of geopolitical risk. After a grueling war of attrition through 2024–2025, recent developments signal escalation rather than resolution. Just this week, Russia launched an unprecedented massive attack on Ukraine’s energy infrastructure, firing over 600 attack drones and dozens of missiles in a single overnight barrage. Ukrainian officials condemned it as a deliberate attempt to cripple the power grid on the eve of Christmas, and indeed widespread blackouts were reported. The strikes were brazen enough to prompt Poland to scramble fighter jets to protect its airspace, underscoring persistent fears of spillover into NATO territory.

On the battlefield, neither side has achieved a decisive breakthrough in 2025. Ukraine’s forces, bolstered by Western weapons and training, have fought Russia to a grinding stalemate across the eastern and southern fronts. Russia, while absorbing heavy losses and economic sanctions, still controls significant swathes of Ukrainian territory and retains the capacity for concentrated offensives like the recent drone barrage. Civilian and infrastructure targeting – as evidenced by the attacks on Ukraine’s power grid – has become a core element of Russia’s strategy to erode Ukrainian resilience during the winter months.

Politically, Western support remains vital for Ukraine’s war effort. European nations have largely maintained unity, dramatically increasing defense spending (European military budgets surged ~17% in 2024 and continued high in 2025) and supplying arms to Kyiv. The United States’ stance, however, has shifted with its new administration. President Donald Trump, inaugurated in January 2025, has sent mixed signals – at times voicing a desire for negotiation, but also indicating a reduced willingness to give Ukraine a “blank check.” So far, U.S. military aid has continued, but investors are wary that U.S. policy could pivot, potentially altering the war’s trajectory. In Moscow, President Putin shows no intent of backing down, framing the war as an existential fight against Western encroachment. Peace talks remain stalled, making a prolonged conflict into 2026 the base case.

From a risk perspective, the range of outcomes remains wide. A contained stalemate could persist, but there is a non-trivial risk of escalation – whether via a Russian offensive surge, a NATO-Russia incident, or even nuclear brinkmanship if Putin grows desperate. Conversely, an unexpected diplomatic breakthrough or ceasefire, while unlikely in the near term, would be a game-changer for markets (removing a major risk premium on European assets and energy prices). In summary, the Russia-Ukraine war continues to cast a long shadow over European stability and global security, demanding close monitoring by investors.

U.S.-Venezuela tensions

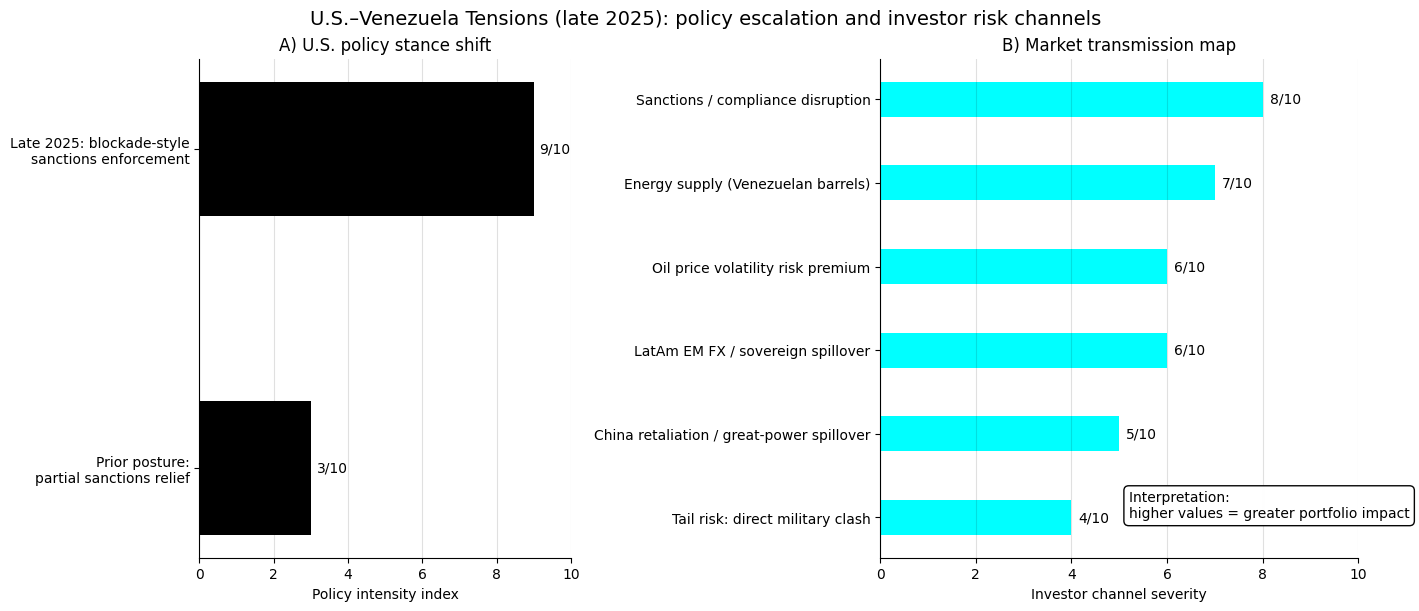

Geopolitical risk is also rising in the Western Hemisphere. The United States has escalated tensions with Venezuela in late 2025, as the Trump administration seeks to reassert U.S. influence and curtail rival powers’ foothold in Latin America. In recent weeks, President Trump openly threatened Venezuela’s leader Nicolás Maduro, stating that a U.S. naval armada – “the largest… in [South America’s] history” – is deployed off Venezuela’s coast. He warned that if Maduro challenges the U.S., it “will be the last time he can do so”, a remarkably direct threat that has raised fears of a potential blockade or even military confrontation.

Indeed, a U.S. naval blockade is already effectively underway. Washington ordered that all sanctioned oil tankers entering or leaving Venezuela be stopped, ostensibly to enforce oil sanctions. This move has choked off Venezuela’s recent recovery in oil exports (which had hit their highest levels since 2019 after partial sanctions relief), and drew an angry response from Caracas and its allies. President Trump has not ruled out the possibility of war with Venezuela if provocations continue, a stark reminder of the extreme endgame risk. These actions mark a 180-degree turn from the prior U.S. administration’s tentative rapprochement (which had briefly allowed some Venezuelan oil back on the market).

Underlying this hard-line stance is oil and great-power politics. As one analyst noted, Trump has dispensed with polite fictions – he explicitly stated that “the oil of Venezuela is our oil, the assets are ours”. The administration views Venezuela’s vast oil reserves as strategically important for U.S. energy security and is unwilling to see them controlled by an anti-U.S. regime or leveraged by rivals like China. Trump and his advisors also object to China’s growing economic presence in Latin America; they have demanded, for example, that China be ousted from Panama’s infrastructure projects and warned Latin American governments against deepening ties with Beijing. The U.S. Southern Command’s leadership was reportedly so concerned about these aggressive moves that its top officers resigned in protest, reflecting internal U.S. debate over the legality and wisdom of overt regime-change tactics.

Venezuela’s neighbors are on edge. Colombia’s President Gustavo Petro – a leftist who opposes U.S. intervention – criticized Washington’s actions related to Venezuelan oil, only to have Trump lambaste Colombia as a haven for drug production, worsening diplomatic relations. The broader region is becoming a geopolitical chessboard: U.S. efforts to isolate Venezuela are aimed at curbing Chinese and Russian influence in Latin America. Beijing, which has heavily invested in Venezuelan oil and lent billions to Caracas, has so far responded only rhetorically. However, U.S. interception of a tanker carrying Chinese-paid Venezuelan crude triggered warnings from experts that China could at some point retaliate – potentially even by establishing a military presence in the Americas (mirroring U.S. deployments in Asia) if its interests are directly threatened.

For now, a direct U.S.-Venezuela military clash has been averted, and Venezuela’s beleaguered economy struggles on under tightened sanctions. But political risk is high: 2024’s postponed Venezuelan elections and any regime-change attempts (internal or external) in 2026 could lead to unrest or conflict. For investors, this raises concerns about energy supply (Venezuela’s oil output and the broader oil price impact) and emerging-market exposure in Latin America (sovereign risk, currency volatility, etc., especially if U.S. actions spark sanctions or proxy conflicts involving regional players like Cuba, Nicaragua, or even a split within OPEC). U.S.-Venezuela tensions thus represent a new front of geopolitical risk emanating from the Western Hemisphere.

U.S.-China rivalry over Taiwan

The strategic contest between the U.S. and China – particularly over Taiwan’s fate – has escalated into a full-spectrum rivalry. Throughout 2025, both powers have taken steps that raise the stakes in the Taiwan Strait, even as they stop short of direct conflict. A recent Pentagon report (as revealed in Washington) warns that China’s military is refining its capabilities for a potential Taiwan invasion by 2027, including developing long-range strike abilities to hold off U.S. forces in the Pacific. Chinese President Xi Jinping has repeatedly asserted China’s historical claim on Taiwan and has ramped up People’s Liberation Army (PLA) drills around the island. These include frequent incursions of Chinese fighter jets across the Taiwan Strait median line and naval exercises seen as rehearsals for a blockade. Taiwan’s own defense ministry has had to stay on constant alert, though no outright clash occurred in 2025.

One startling development is China’s rapid nuclear arsenal expansion. U.S. intelligence indicates Beijing has been loading over a hundred new DF-31 intercontinental ballistic missiles into newly built silo fields in western China. China appears on track to triple or quadruple its nuclear warhead stockpile to ~1,000 warheads by 2030, a dramatic shift from its historically minimal deterrent. This is happening just as the last U.S.-Russia arms control pact is set to expire in February 2026 with no extension. Alarmingly, China has refused to join any arms control talks, meaning the world could enter 2026 with no binding limits on the nuclear arsenals.

On the U.S. side, the Trump administration has pursued a policy of strength through deterrence. President Trump announced plans to construct new cutting-edge warships controlled by artificial intelligence, equipped with hypersonic missiles and laser weapons, to maintain U.S. naval dominance. The U.S. Pacific Fleet has been visibly active around Taiwan and the South China Sea, conducting freedom-of-navigation operations near Chinese-claimed islands. Washington has also boosted security cooperation with allies Japan, Australia, and the Philippines, aiming to present a united front. Notably, defense spending in the Indo-Pacific is surging: the FY2025 U.S. defense budget included major investments in Indo-Pacific deterrence (missile defenses, new deployments), and U.S. pressure has led NATO to declare China a “systemic challenge” for the first time.

Despite these moves, diplomatic channels are not entirely shut. High-level U.S.-China meetings in late 2025 yielded small confidence-building measures (on climate cooperation and military-to-military communication hotlines), suggesting neither side wants an active war. But the structural issues remain unresolved – Taiwan’s political status, trade and technology disputes (Trump’s tariffs on Chinese goods remain in effect, some even increased, contributing to a re-shoring trend), and the broader ideological competition. Beijing’s internal shakeups, such as anti-corruption purges in the PLA, slowed some defense procurement in the short run (per experts, China’s arms industry revenues actually dipped in 2024 due to canceled contracts amid the purge). However, those efforts could ultimately make China’s military more efficient and loyal, potentially strengthening its hand in a few years.

For investors, the U.S.-China rivalry presents a complex risk. In the near term, it’s manifested in export controls (U.S. curbs on advanced chip exports to China), investment restrictions, and supply-chain diversification – impacting tech sectors and emerging Asia markets. The tail risk, though, is a crisis over Taiwan that could disrupt global trade (Taiwan’s semiconductor exports are vital, and conflict could sever shipping lanes across the Indo-Pacific). Even short of war, military posturing or sanctions can roil markets – for instance, rumors of a blockade or an air defense identification zone over Taiwan would likely spark a global sell-off and flight to safety. Thus, the U.S.-China-Taiwan triangle is a critical focus for scenario analysis as we look into 2026.

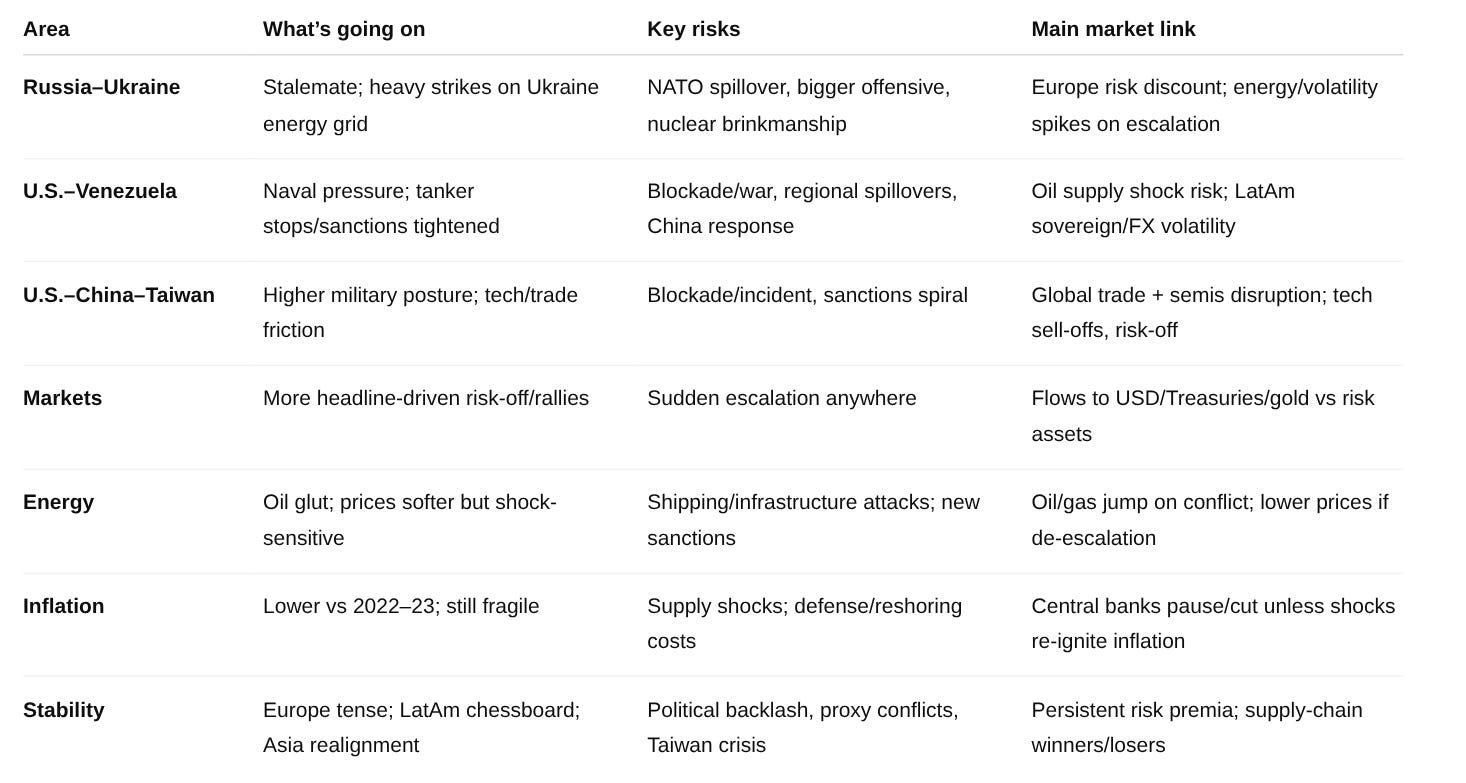

Implications for markets, energy, inflation, and stability

The above conflicts have tangible impacts on financial markets, commodity supplies, inflation dynamics, and regional stability. The key implications are outlined below:

Market volatility and risk sentiment: Periodic risk-off episodes have hit markets whenever these geopolitical tensions flare. For example, each time Russia unleashed major assaults or nuclear threats in the Ukraine war, global equities tended to dip and volatility spiked. Similarly, rising U.S.-China frictions (such as tariff announcements or military encounters near Taiwan) have triggered sell-offs in Asian markets and tech stocks. Investors now demand a geopolitical risk premium, particularly in exposed regions: Eurozone equity valuations remain somewhat discounted due to the war on its doorstep, and Chinese/Hong Kong markets trade at low multiples reflecting geopolitical discount. On the flip side, U.S. markets have been relatively resilient – even seen as safe-havens – given America’s energy independence and distance from the conflicts. Overall, the correlation between conflict news and market moves has strengthened: bad news (escalation) sends investors toward Treasuries, gold, and the U.S. dollar, whereas hints of peace or de-escalation spark relief rallies in risk assets.

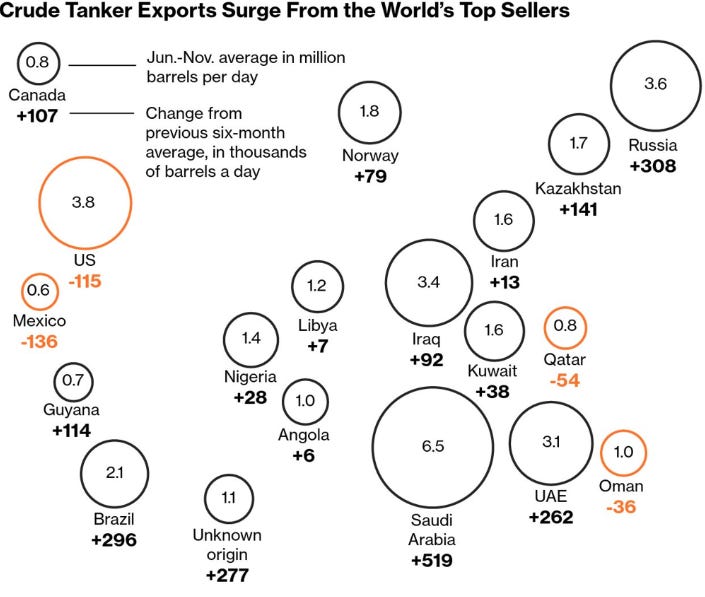

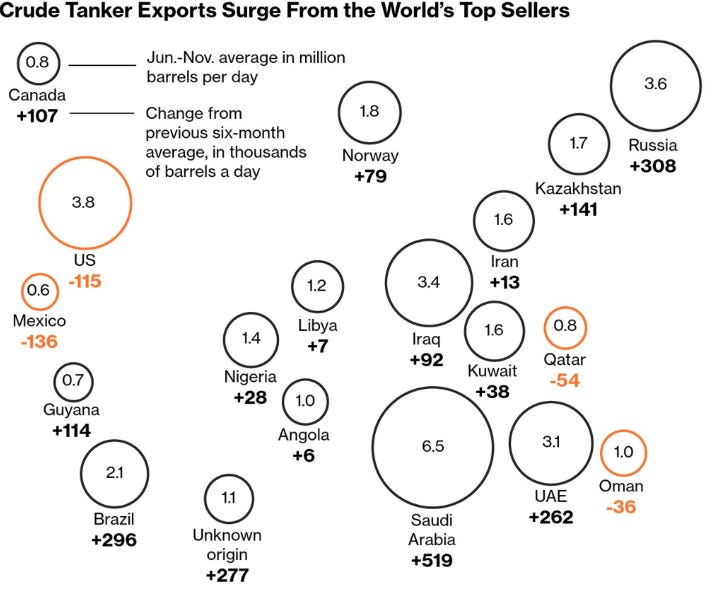

Energy supply and prices: Geopolitics has been a major driver of energy prices since 2022. The Russia-Ukraine war initially sent oil and natural gas prices soaring in 2022–2023, as Russian exports were curtailed and Europe scrambled for alternate supplies. However, by late 2025, the dynamic has reversed into a surprising oil glut. High prices incentivized massive supply responses: OPEC+ producers (including Saudi Arabia and even sanctioned Russia and Iran) increased output, and non-OPEC sources surged. Brazil’s oil production hit record highs in 2025, U.S. shale output reached a fresh peak under Trump’s pro-drilling agenda, and even newcomer producers like Guyana and new fields in Africa ramped up exports. Meanwhile, global demand growth has been moderate. The result: global oil inventories swelled, with a record 1.3 billion barrels afloat on tankers worldwide. Benchmark Brent crude prices are on track for their biggest annual drop since 2020, down about 20% this year to the ~$60 range. Gasoline in the U.S. has fallen below $3/gallon on average – a welcome relief for consumers and a political win for Trump.

Oil prices set to be pushed lower in 2026 Despite this softening of oil prices, energy markets remain finely balanced and highly sensitive to geopolitical shocks. Any escalation – say, an attack on oil infrastructure or shipping lanes – could send prices spiking overnight. The U.S.-Venezuela confrontation exemplifies this: news of Trump’s tanker blockade and war threats injected short-term volatility in crude prices (initially lifting prices on supply concern, though the broader glut limited the sustained impact). Conversely, a resolution of conflicts (a durable Ukraine ceasefire allowing sanction relief for Russian oil, or a political deal on Venezuela that increases its exports) could further depress oil prices in 2026. Natural gas has its own story: Europe, having largely weaned off Russian pipeline gas, built up comfortable storage (>80% full entering winter) and secured ample LNG supplies, resulting in much lower gas prices in 2023–2025 than the crisis peaks. Yet Europe’s energy resilience is not bulletproof – a harsh winter or damage to critical infrastructure could still cause localized shortages or price spikes. In short, energy-dependent sectors and countries are not out of the woods, but the baseline going into 2026 is one of improved supply and lower prices compared to the immediate post-invasion period. This has broad implications for inflation and policy, as discussed next.

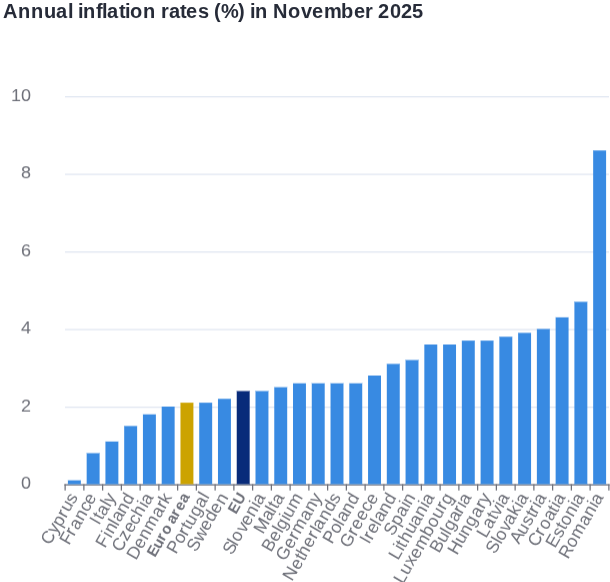

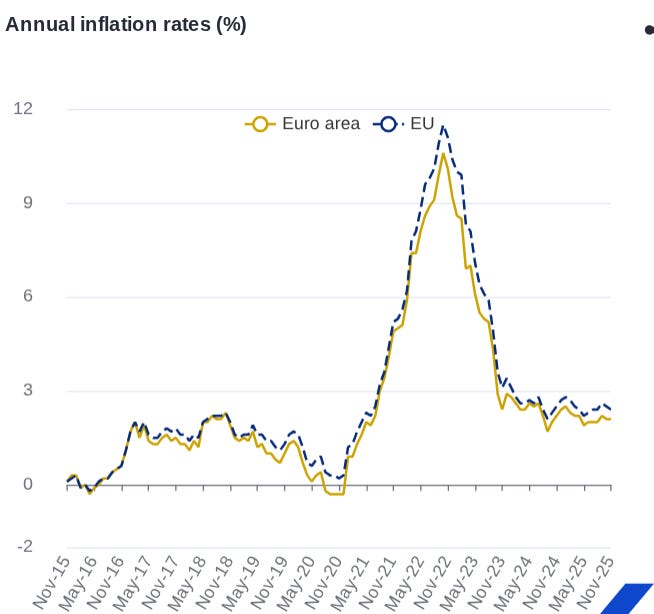

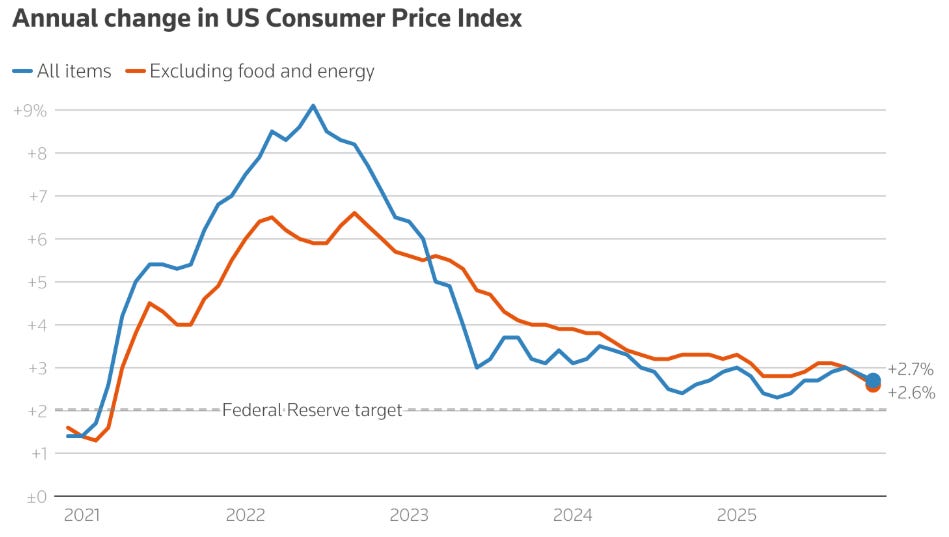

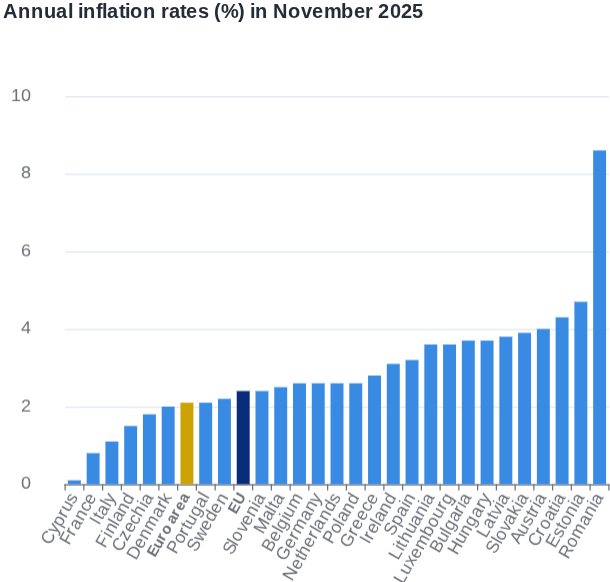

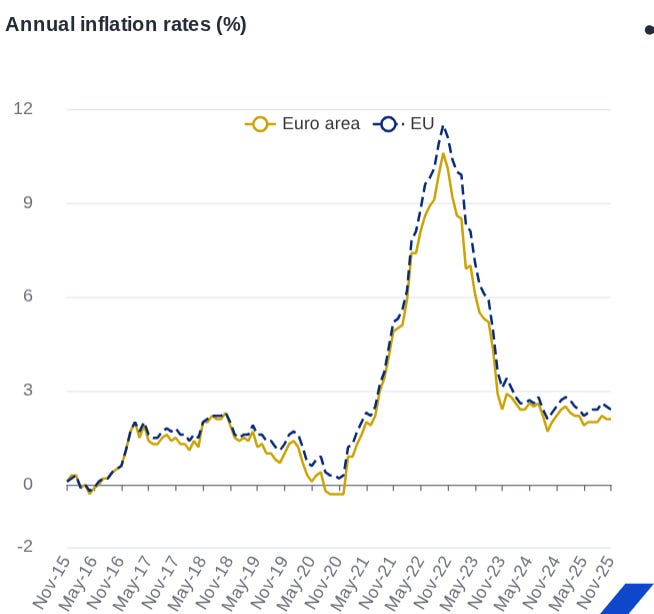

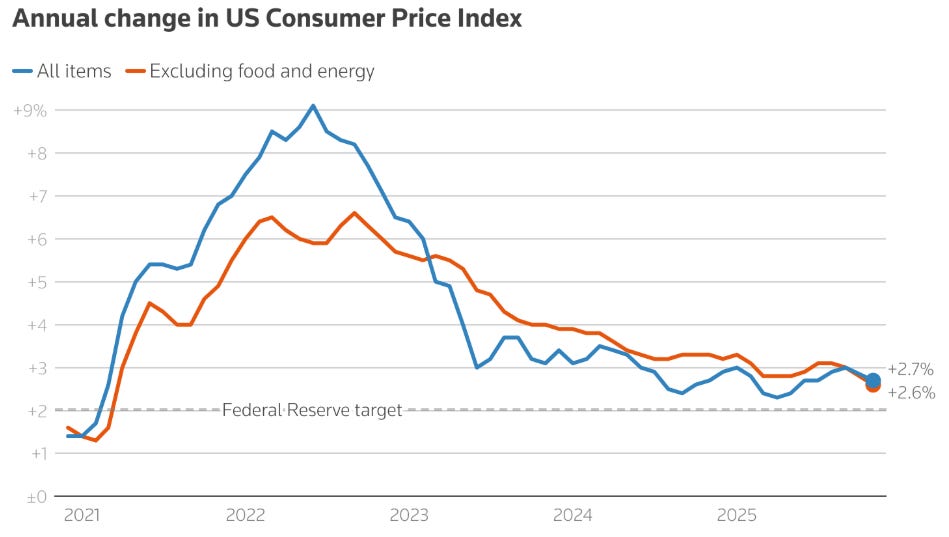

Inflation and monetary policy: The inflationary storm that rocked the world in 2022–2023 (fueled in part by war-related commodity spikes and supply disruptions) has largely subsided by late 2025. Headline inflation in the U.S. is back near 3% (2.7% YoY in Nov 2025), and in the euro area ~2.1%– a dramatic improvement from double digits two years prior. The easing of energy costs has been a major driver of this disinflation. Cheaper oil and gas directly lower fuel and utility prices; indeed, European energy prices in 2025 are contributing negatively to inflation on net. Additionally, supply-chain pressures have abated, and higher interest rates from central banks cooled demand.

Annual inflation rates in the Euro Area Crucially, however, geopolitical risks keep an underlying floor under inflation expectations. Firms and governments are adapting to a less globalized, more fragmented world: reshoring production, diversifying suppliers, and building strategic stockpiles of commodities. These moves improve resilience but can be inflationary (due to higher production costs and duplication of supply chains). Moreover, conflict-driven spending – notably defense outlays – has ballooned fiscal deficits in many countries. World military spending hit a record $2.7 trillion in 2024 (+9% YoY), and continues to rise in 2025. While defense spending itself adds demand stimulus (supporting industries and jobs), it can crowd out productive investment and, if debt-financed, put upward pressure on interest rates long-term. Central banks are thus caught in a balancing act: they welcome the return of inflation closer to target, but cannot be complacent. The Federal Reserve’s recent rate cuts (bringing the policy rate down to ~3.6%) acknowledge improved inflation, yet Fed officials voice caution that further conflict or commodity shocks could force a reversal to tightening. The European Central Bank likewise treads carefully as energy security remains a strategic concern for the continent.

Under current geopolitical conditions, the base case is that inflation remains near target in 2026, allowing a stable or slightly easing rate environment. However, a serious pessimistic scenario (a Taiwan crisis or a wider war) could re-ignite inflation via supply shocks just as in 2022, leading to a stagflationary twist. Conversely, a rapid de-escalation of conflicts with a surge in commodity supplies (imagine a Russia-Ukraine peace lifting sanctions, or a U.S.-Iran nuclear deal adding oil) could even push inflation below target. Thus, inflation hedges should remain in the toolkit given the wide range of plausible outcomes.

Regional stability and security order: Each conflict carries broader implications for regional stability, which in turn affect investment climates:

Europe: The Ukraine war has paradoxically strengthened Western unity (NATO enlargement and rearmament) but also exposed structural vulnerabilities (energy dependence, defense gaps). Europe’s economy proved resilient in 2023–2025, but the war’s ongoing costs – supporting Ukraine, higher defense budgets, hosting refugees, and lost trade with Russia – are a drag on growth. Eastern Europe faces higher security risks (Poland stepped up air defenses after spillover incidents), and political strains are visible (extreme parties gaining ground in some countries by exploiting war fatigue or inflation angst). For investors, Europe now carries a persistent geopolitical discount: higher required returns to compensate for proximity to conflict. If stability improves (ceasefire), that discount could shrink, unlocking upside in European assets. If instability worsens (war escalation or political upheaval in a NATO state), Europe could underperform significantly due to capital flight to safety.

Latin America: U.S.-Venezuela frictions risk destabilizing the northern South America region. Venezuela itself remains economically fragile; any confrontation could trigger a migrant exodus and ripple effects in neighbors like Colombia, Brazil, and Caribbean states. U.S. sanctions and pressure might also push Venezuela and aligned countries further into the orbit of U.S. rivals (China, Russia, Iran), potentially leading to a bifurcation in the region’s economic alignments. Investors with Latin American exposure must watch for country-specific risk (sanctions risk for firms dealing with Venezuela or political risk in countries caught between superpowers). On the positive side, some Latin nations (Brazil) might benefit if they can play a neutral role – attracting investment as alternate suppliers (Brazil’s record oil exports in 2025 highlight this potential) or as mediators.

Asia-Pacific: The U.S.-China rivalry has prompted a significant realignment in Asia. U.S. allies like Japan, South Korea, and Australia are increasing defense spending and cooperation. Southeast Asian nations are hedging between the two giants, but a few (the Philippines) have swung toward the U.S. to counter Chinese assertiveness. Taiwan remains the flashpoint; its January 2024 elections (not long past) yielded a new leadership that is comparatively more Beijing-friendly than its predecessor – a factor that has slightly eased cross-strait tensions in the near term. Nonetheless, China’s military posture keeps the region on edge. A conflict in Asia would be globally catastrophic for stability: beyond the immediate human and economic toll in East Asia, it would likely sever critical supply chains (electronics, shipping routes), jolt commodity flows, and force nearly all economies to take sides, essentially splintering the global trading system. Even absent war, decoupling trends mean investors must navigate an environment where trade barriers and investment restrictions are higher, and where access to the Chinese market (the world’s second-largest economy) could be suddenly constrained by geopolitical considerations. Conversely, countries like India, Vietnam, and Mexico are positioning to capture supply chain shifts – a source of opportunity if stability holds.

In summary, today’s geopolitical climate is one of heightened but manageable risk. Markets have largely adapted to a new normal of persistent tensions, but they remain prone to shock reactions if any conflict takes an unexpected turn. Energy and inflation pressures have moderated for now, providing a window of opportunity for portfolios to recoup and reposition. However, the underpinning fragility of peace in multiple theaters means that risk management and scenario planning are absolutely critical as we head into 2026.