Table of contents:

Introduction.

US Fiscal stability and the political economy.

The military-industrial catalyst.

The cost of governance failure.

The Federal Reserve succession crisis.

The technology sector – valuation vs. reality.

The Deutsche Bank signal (institutional hedging).

Geopolitical fracture and energy security.

The EU’s 20th sanctions package.

Ukraine’s EU accession.

Asset class deep dive, portfolio construction & rebalancing updates.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

As of mid-November 2025, the global financial architecture is straining under the weight of a profound disconnect—a great divergence—between the exuberant valuations of the artificial intelligence sector and the deteriorating physical and political realities of the global economy. We are navigating a period defined by stagflationary fragility, where the simultaneous forces of monetary debasement, geopolitical fracturing, and institutional paralysis are reshaping the investment landscape.

The catalyst for this immediate crisis was the historic 43-day US government shutdown, a legislative impasse that concluded not through functional governance, but through the sheer necessity of preventing a total systemic collapse. The resolution, achieved on the 15th voting attempt after 14 failures, was characterized by high political drama—including the delayed arrival of a Texas senator caught in the very aviation chaos the shutdown had exacerbated. While the public narrative focused on the partisan battle over Affordable Care Act subsidies, proprietary analysis suggests the true forcing mechanism was the Military-Industrial Complex. The stoppage of progress payments had paralyzed critical defense supply chains, stalling work on classified seventh-generation fighter programs and threatening the flow of munitions to Ukraine and Taiwan. The eventual “minibus” deal, which extends funding only through early 2026, is less a solution than a temporary ceasefire in a continuing fiscal war.

Check more about the shutdown here:

This political dysfunction is mirrored by deep economic malaise. Consumer sentiment has collapsed to recessionary levels (University of Michigan Index at 50.3), driven by the erosion of purchasing power and the un-anchoring of inflation expectations. Yet, paradoxically, equity markets remain elevated, buoyed by a speculative mania in Artificial Intelligence that is increasingly detached from profitability. Major institutional signals, such as Deutsche Bank’s move to hedge its data center debt exposure via synthetic risk transfers and short equity baskets, indicate that smart money is preparing for a violent mean reversion in the tech sector.

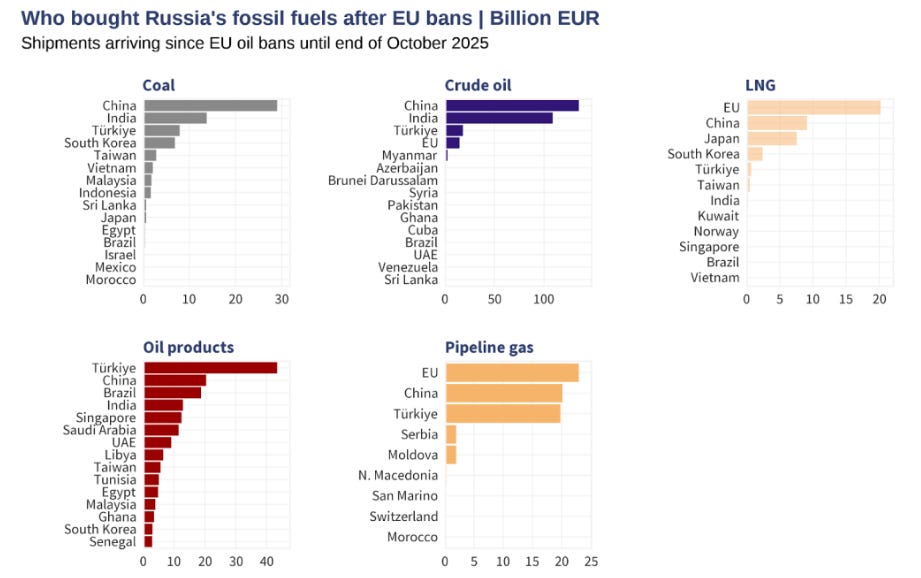

Concurrently, the geopolitical order in Europe continues to fracture. The European Union’s preparation of a 20th sanctions package against Russia underscores the failure of the previous nineteen. Russian hydrocarbons continue to flow freely into Europe, laundered through transshipment hubs in Morocco and Turkey, creating a sanctions premium that burdens European industry while failing to defund the Russian war machine. Furthermore, the accelerated push for Ukraine’s EU accession is creating internal fissures, with the potential displacement of Common Agricultural Policy (CAP) funds threatening the economic interests of existing member states like Poland and Spain.

In this environment, the traditional 60/40 portfolio is obsolete. Capital preservation and growth now require a decisive rotation from faith-based assets (fiat currency, long-duration treasuries, unprofitable tech) toward reality-based assets.

US Fiscal stability and the political economy

The conclusion of the longest government shutdown in modern US history was less a triumph of legislative compromise and more a tactical ceasefire necessitated by the imminent collapse of critical national infrastructure. The 43-day stalemate, which commenced on October 1, 2025, and concluded on November 12, 2025, furloughed approximately 900,000 federal employees and forced another two million to work without pay, effectively freezing a significant portion of the US economy’s discretionary spending power.

While the public narrative focused on the expiration of enhanced premium tax credits (PTC) under the Affordable Care Act—a central demand of the Democratic caucus—the underlying dynamics were far more complex. The shutdown was not merely a budgetary dispute but a stress test of the US federal system’s operational continuity. The minibus funding package eventually signed by the President extends funding for specific agencies—Military Construction-VA, Agriculture-FDA, and the Legislative Branch—through the end of September 2026. However, crucially, it provides only a temporary stopgap for other government functions through January 30, 2026, guaranteeing that this volatility will return in Q1 2026.

The exclusion of the PTC extension in the final deal represents a significant deflationary shock. These credits, originally enacted under the ACA and boosted by the Inflation Reduction Act, were essential for millions of households to afford health insurance. Their expiration implies a sudden contraction in disposable income for these consumers, who must now divert capital from consumption to essential healthcare coverage.

The military-industrial catalyst

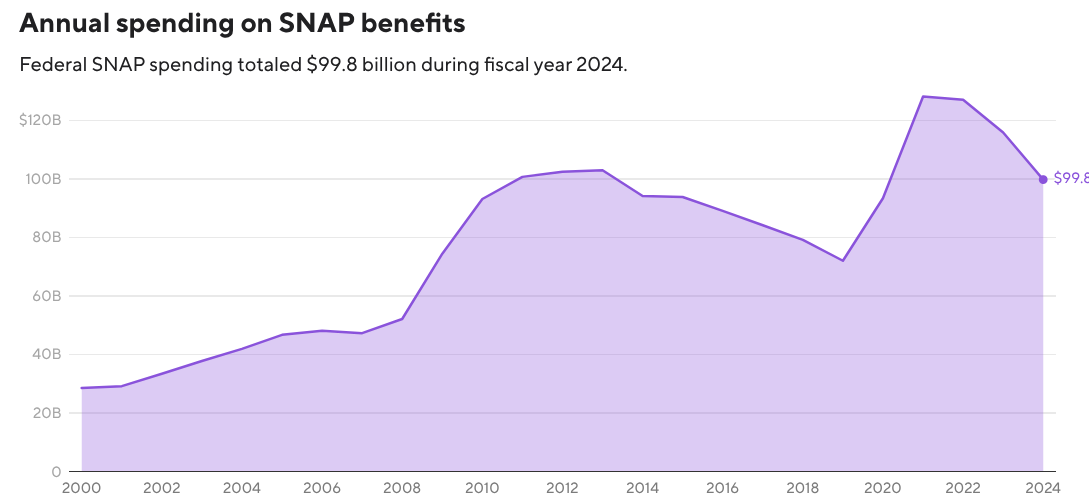

Analysis of the negotiation endgame reveals a critical, underreported driver of the resolution: pressure from the defense sector. While public attention fixated on the disruption to social programs like SNAP (Supplemental Nutrition Assistance Program) and the cancellation of thousands of flights due to air traffic controller shortages, market intelligence suggests the decisive factor was the paralysis of the Pentagon’s procurement pipeline.

The shutdown had halted work on highly classified and capital-intensive projects, including the development of seventh-generation fighters and new armaments that had not yet been fully licenced or budgeted. The defense industrial base, already strained by supply chain commitments to Ukraine and Taiwan, faced a critical liquidity crunch as progress payments stopped. The overruns on existing contracts—where projects exceed their budget and require immediate supplementary funding to continue—created a backlog that threatened to shutter production lines. It is highly probable that the intense lobbying from defense primes, who faced defaults on their own supply chain obligations, forced the Republican leadership to capitulate on the clean funding bill, stripping out the controversial healthcare demands to ensure the military machine resumed operation.

The cost of governance failure

The economic toll of the shutdown extends far beyond the direct loss of government output. The disruption to the SNAP threatened to cut off 42 million Americans from food benefits, a catastrophe averted only by the last-minute deal. The reimbursement of states for federal expenses incurred during the shutdown adds another layer of fiscal drag to the 2026 budget.

Politically, the resolution required a fracture within the Democratic party. Senate Republicans, who had blocked previous House measures, eventually secured the necessary 60 votes only after a group of Democrats crossed the aisle, decoupling the healthcare subsidies from the government funding bill. This vote count—60-40 in the Senate and 222-209 in the House—demonstrates the fragility of the governing coalition. The narrow margins imply that any future legislative action, particularly regarding the debt ceiling or further Ukraine aid, will face similar, if not greater, hurdles.

The most alarming signal for the US economy is the deterioration in consumer confidence, which has plummeted to recessionary depths. The wealth effect typically generated by high equity prices has been completely negated by the erosion of real purchasing power and the instability of the federal government.

The index falling to 50.3 is historically significant; such levels are typically only observed during severe economic contractions, such as the 2008 Global Financial Crisis or the stagflationary peaks of the late 1970s. The sharp divergence between the Current Conditions index (52.3) and Consumer Expectations (49.0) highlights a pervasive pessimism. Consumers are not just struggling now; they expect to struggle more in the future.

This sentiment is underpinned by sticky inflation expectations. The 1-year inflation expectation remains elevated at 4.7%, while the 5-year expectation sits at 3.6%. This un-anchoring of inflation expectations is the Federal Reserve’s nightmare scenario. It suggests that the public has lost faith in the central bank’s ability to restore price stability, leading to a self-fulfilling wage-price spiral even as growth decelerates.

The Federal Reserve succession crisis

Adding to the monetary uncertainty is the looming end of Jerome Powell’s tenure as Federal Reserve Chair in May 2026. The market has begun to aggressively price in the nomination of Kevin Hassett, a former senior economic adviser known for his supply-side orientation and close alignment with the executive branch’s growth agenda.

Prediction markets in November 2025 assign a probability of approximately 42% to Hassett’s nomination, significantly higher than other contenders like Kevin Warsh or Scott Bessent. Hassett has publicly stated his willingness to accept the role and has criticized the current Fed’s reluctance to cut rates more aggressively.

The nomination of a candidate perceived as loyalist or politically motivated introduces a binary risk to the US Treasury market. If the market concludes that the Fed’s independence is being compromised to facilitate fiscal expansion (i.e., keeping rates low to fund the deficit), we could see a revolt in the bond market. This would manifest as a steepening of the yield curve, with long-end yields (10Y and 30Y) spiking to reflect a higher term premium for inflation risk. Such a scenario is inherently bullish for non-sovereign stores of value, particularly gold and Bitcoin, and bearish for the US dollar in the long term.

The technology sector – valuation vs. reality

By November 2025, the euphoria surrounding Artificial Intelligence has begun to face intense scrutiny regarding profitability and return on investment. While the Magnificent 7 stocks continue to dominate indices, cracks are appearing in the narrative that AI expenditure will translate into immediate corporate profits. The market is currently pricing in a future of limitless growth that mathematical reality may not support.

The focal point of this anxiety is OpenAI. Reports indicate the company is preparing for a potential IPO in 2027 with a staggering valuation target of $1 trillion, despite generating massive losses—$13.5 billion in the first half of 2025 alone. The company’s transition to a for-profit entity and aggressive lobbying for government funding (described by critics as a prestigious welfare for the tech aristocracy) suggests that private capital markets may be reaching a saturation point regarding their willingness to fund endless CapEx without clear revenue models.

A dangerous disconnect has emerged between capital expenditure and revenue. Nvidia and other hardware suppliers are booking revenue that appears as CapEx on the balance sheets of hyperscalers (Microsoft, Google). Bain & Co. has warned that the AI sector needs to generate $2 trillion in annual revenue by 2030 to justify the current infrastructure build-out—a target that faces an $800 billion shortfall based on current trajectories. If the end-user demand for AI applications does not materialize to cover these costs, the CapEx cycle will contract violently. This would lead to an earnings recession for the entire semiconductor supply chain, as the shovels are no longer needed if no gold is found.

The Deutsche Bank signal (institutional hedging)