[INTEL REPORT] Energy conflict and alliance rearmament

An integrated view of conflict, inflation and capital flows

Table of contents:

Introduction.

Global macro after the energy shock.

The United States, the axis of growth, finance, and military escalation.

The main price-maker in the global economy.

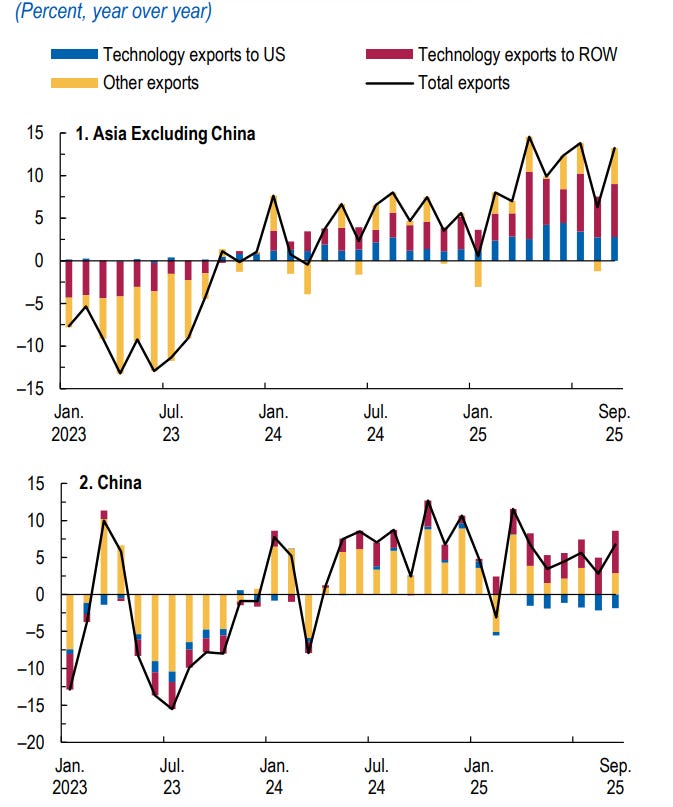

China and Asia are the first receivers of the Hormuz shock.

The dollar, bond markets, and the return of geopolitical duration risk.

NATO, military burden-sharing, and the remapping of Western power.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

The global backdrop has entered a harder regime. Energy, shipping, fiscal capacity, military posture, and capital allocation now trade through the same set of constraints. Variables that once sat in separate analytical buckets now belong to a single pricing framework. Oil routes shape inflation. Alliance commitments shape issuance. Industrial policy shapes defence readiness. Currency strength shapes import costs and external adjustment. The market is pricing all of it together.

The central question concerns the kind of growth that can endure when energy friction rises, logistics tighten, and states absorb a larger strategic burden. That shift changes the hierarchy of variables. Security of supply carries more weight. Duration risk carries more weight. Fiscal credibility carries more weight. The ability to convert spending into usable capacity also carries more weight, whether in semiconductors, power systems, refining, shipping, or defence production.

This piece follows that chain from the macro layer into the strategic layer and back again. It begins with the global economy after the energy shock, where an active investment cycle now meets a harsher cost structure. It then turns to the United States, the core balance sheet in the system, where growth leadership, Treasury funding, monetary policy, and force projection converge. From there, the focus shifts to the conflict itself as the marginal driver of price formation across oil, gas, freight, and risk premia.

The analysis then moves to Asia, where direct exposure to Gulf energy flows makes the region the first receiver of the shock in physical, financial, and policy terms. It then examines the dollar and sovereign debt markets, where the length of the shock has become a key variable for yields, term premium, and global liquidity demand. The final section studies NATO and the wider Western security architecture, where rising military spending points to a deeper redistribution of industrial capacity, operational responsibility, and strategic weight.

Check more about all of this here.

The aim is to frame the current environment the way markets are beginning to price it, as one integrated system. Growth, inflation, war, energy, debt, and alliance structure now move through the same circuit. The edge comes from seeing the connections early, before consensus fully absorbs their implications.

Global macro after the energy shock

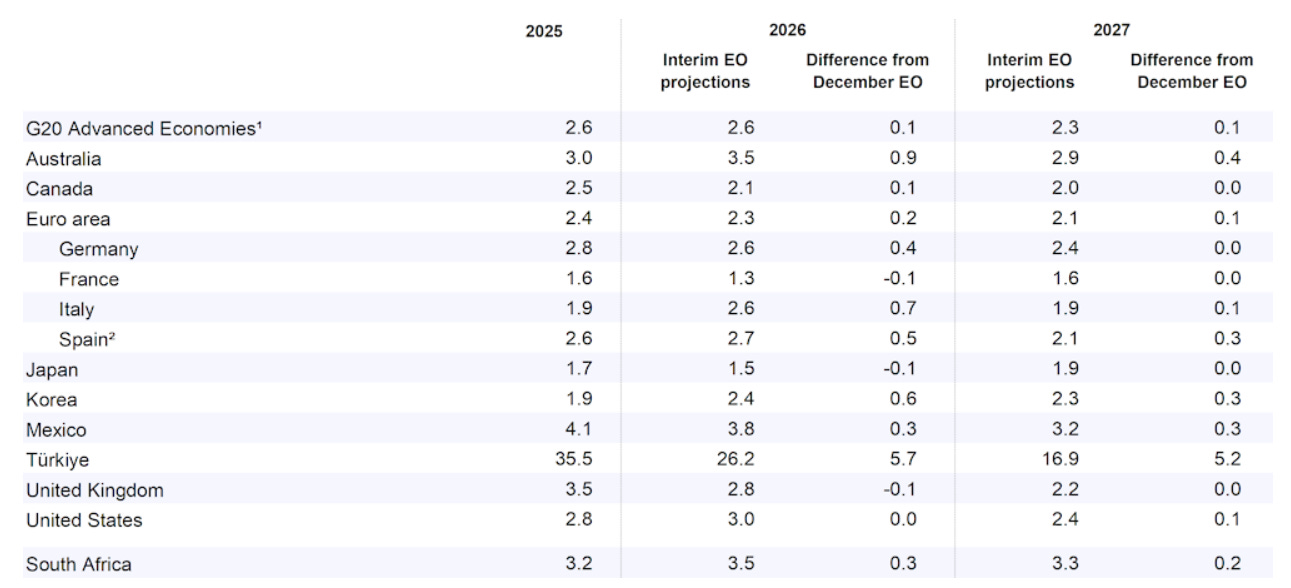

We can say we have two engines that pull in opposite directions. One engine comes from the capital cycle that formed through 2025 and carried into 2026 through technology investment, private-sector adaptation, and supportive demand. The other engine comes from the war-driven energy shock, the tightening of transport routes, and the rise in geopolitical risk premia across commodities, shipping, rates, and equities. The world economy is treated as a system where energy access, market confidence, military escalation, and asset pricing move together. The IMF and OECD now describe the same architecture in institutional language. The IMF’s update still presented a world economy with resilient growth, projecting global output growth at 3.3% in 2026 and 3.2% in 2027, driven in part by technology investment, supportive financial conditions, and private-sector adaptability. By late March, the OECD had redrawn that picture. It projected global growth at 2.9% in 2026 and 3.0% in 2027, with the Middle East conflict, higher energy prices, and supply-chain disruption pushing costs higher and demand lower.

The tension between those two engines defines the whole macro regime. The first engine still matters because technology investment remains large, especially in sectors tied to artificial intelligence, semiconductors, cloud infrastructure, industrial automation, and the digital build-out of the energy and security complex. The IMF highlighted strong performance in exports of semiconductors and related equipment across Asian economies and linked that strength to the rise in information and technology investment. That matters because a technology-led capex cycle creates growth through many channels at once. It supports equipment orders, lifts productivity expectations, raises corporate spending, improves cash-flow visibility for firms near the center of the build-out, and attracts capital toward the economies that lead those value chains. This is one reason the United States has strong relative support. It is also one reason parts of East Asia carried stronger industrial momentum into the year than many analysts expected at the end of 2025.

At the same time, the second engine has become the dominant marginal force in pricing. The OECD says the conflict in the Middle East is testing the resilience of a global economy that had been supported by financial and fiscal conditions and growing demand for artificial intelligence technologies. It states that the halt in shipments through the Strait of Hormuz and the closure or damage of energy infrastructure generated a surge in energy prices and disrupted the global supply of energy and other key commodities, including fertilisers. This is central because it shifts the macro discussion away from the classic debate about whether demand remains firm and toward a more strategic debate about how long the energy shock lasts, how broad the shipping disruption becomes, and how much of the rise in commodity prices passes into wages, services, industrial margins, and inflation expectations.

This leaves the world economy in a narrower corridor than the one investors saw at the beginning of the year. In January, the baseline still looked like a world of steady growth with disinflation in progress. Now that baseline became conditional on the moderation of energy-market disruption from mid-2026 onward. The OECD states that its projections rely on that technical assumption. The economic meaning is clear. A shorter disruption preserves a large part of the prior macro script. A longer disruption transforms the outlook into one shaped by persistent cost pressure, weaker real income growth, broader financial repricing, and stronger dependence on fiscal triage and central-bank credibility.

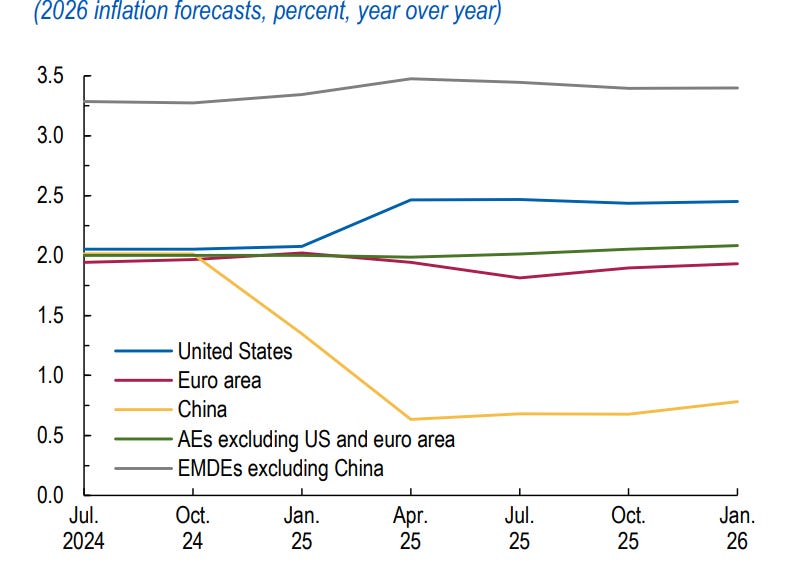

The inflation story reflects this shift with unusual clarity. The IMF’s update expected global inflation to fall, projecting headline inflation at 3.8% in 2026 and 3.4% in 2027. That forecast came from a world in which supply conditions improved, commodity pricing eased from earlier extremes, and private adaptation softened the impact of trade-policy friction. The OECD’s update already incorporates the war shock. It projects G20 inflation at 4.0% in 2026, which is 1.2 percentage points higher than it expected before the conflict escalated, before easing to 2.7% in 2027 under the assumption that energy pressures fade. This difference between the January IMF view and the March OECD view is one of the cleanest expressions of the regime change. It shows how quickly a global disinflation narrative can bend when energy, logistics, and risk premia move together.

The inflation process has also split into layers. Headline inflation is the first recipient of the shock because oil, gas, fuel transport, chemicals, and fertilisers transmit rapidly into measured prices. Core inflation then becomes the field of contest. If households and firms treat the energy shock as a passing event, core inflation stabilises with less secondary impact. If firms push higher input costs through broader price categories and workers seek compensation for weaker real incomes, core inflation becomes more persistent. The OECD says medium-term inflation expectations already rose following the energy-price spike. That point matters because expectations serve as the bridge between a commodity event and a more durable inflation process. The shape of that bridge has become one of the decisive macro variables.

Growth now rests on dispersion rather than on one shared global rhythm. The United States still benefits from strong AI-related investment, and the OECD projects U.S. growth at 2.0% in 2026 before easing to 1.7% in 2027. China remains a large growth pole at 4.4% in 2026 and 4.3% in 2027 in the OECD baseline, with state support and industrial strength still carrying weight. The euro area carries a weaker profile. The OECD projects euro area growth at 0.8% in 2026 before a move to 1.2% in 2027, helped in part by stronger defence spending. These numbers describe more than regional variation. They describe the way energy exposure, trade composition, industrial structure, and policy room now shape macro outcomes. Economies close to the technology capex wave retain momentum. Economies more exposed to imported energy and external demand face a tighter balance.

That regional dispersion also changes the meaning of policy credibility. In a calmer cycle, policy credibility often refers to a central bank’s ability to anchor inflation and a finance ministry’s ability to sustain debt. In the current cycle, the idea becomes wider. Credibility now includes the ability to secure energy, preserve transport flows, design temporary support measures without weakening the fiscal base, and maintain enough strategic coherence that firms can plan capital expenditure with confidence. The OECD writes that government measures to cushion higher energy prices should be targeted, preserve incentives to lower energy use, and carry clear expiry mechanisms. It also stresses limited fiscal space and the need for credible medium-term adjustment paths. This means macro policy has become an exercise in war-era selectivity rather than a broad stimulus exercise.

The capital-market layer follows the same logic. In the technology engine, markets still reward growth visibility, margin durability, and long-duration cash flows linked to infrastructure, semiconductors, power systems, software, automation, and data architecture. In the energy-shock engine, markets demand compensation for transport friction, raw-material scarcity, rate volatility, and policy uncertainty. The OECD says financial conditions tightened after the outbreak of hostilities, with volatility rising and the previous degree of accommodation shrinking. The important point lies in the combination rather than in a single asset class. Equities, bonds, currencies, commodities, and credit spreads are all trying to price the same unknown at once, namely the duration and reach of the conflict shock. That creates a macro system in which every bond curve carries an energy assumption, every central-bank path carries a shipping assumption, and every equity multiple carries an embedded judgment about geopolitical durability.

The structural dimension runs deeper than the current quarter. The OECD highlights that persistent disruptions to Middle East exports could aggravate shortages of key commodities and produce a broader repricing in financial markets. It also notes that countries in the Gulf serve as an important source of aluminium, helium, bromine, fertiliser inputs, and logistics services. This widens the macro significance of the current conflict. The issue extends beyond oil and gas. It reaches into food systems through fertilisers, into industrial production through metals and specialty materials, and into advanced manufacturing through chemical and memory-chip supply chains. A prolonged disruption therefore reshapes more than headline inflation. It reshapes the cost map of the industrial economy.