[INTEL REPORT] Defense, resources, and digital infrastructure

From central bank policy to supply chains

Table of contents:

Introduction.

Central bank policy.

Geopolitical risk & reward.

Investment opportunities.

Trade wars, tariffs, and strategic supply chains.

Building the portfolio.

Assessing digital asset.

Strategic allocation and recommendations.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

The global landscape in August 2025 is defined not by a single crisis, but by a confluence of interlocking challenges—a "polycrisis." This environment is characterized by persistent, policy-driven inflation in the United States, constraining the actions of the Federal Reserve; an escalation of great power competition, most visibly through the war in Ukraine and a renewed nuclear arms race; and a fundamental, likely irreversible, rewiring of global trade and supply chains. The post-Cold War era of hyper-globalization, predicated on the primacy of economic efficiency, has definitively ended. It has been replaced by a world where national security imperatives now dictate economic, trade, and industrial policy. This paradigm shift invalidates many of the assumptions that guided capital allocation over the past three decades.

Today we synthesizes extensive macroeconomic, geopolitical, and technological data to formulate three primary, actionable investment theses:

The escalating geopolitical risk is fueling a secular, non-discretionary, and global spending cycle in national security. The return of state-on-state conflict and the collapse of arms control treaties have made military modernization and technological superiority an existential priority for nations. This creates durable, long-term investment opportunities in the indispensable hardware and software of modern deterrence, spanning the defense, aerospace, and cybersecurity sectors. You can check more about this here:

The weaponization of trade policy is forcing a costly but necessary global industrial reconfiguration. This creates compelling investment opportunities in the foundational enablers of this shift: the strategic raw materials and critical minerals required to build new industrial capacity, and the emerging logistics corridors, such as those in the Arctic, that offer strategic alternatives to traditional, contested trade routes.

The market is bifurcating into two distinct streams: high-beta digital commodities like Bitcoin, which are becoming financialized as a macro asset, and the utility-driven adoption of blockchain technology by enterprises. The latter represents a long-term investment in the infrastructure of digital trust—a critical need in a low-trust geopolitical world where verification, transparency, and security are paramount.

Central bank policy

2025 is the year of contradiction. Monetary policy, the traditional lever for managing economic cycles, is no longer operating in a vacuum. It is heavily constrained and influenced by the crosscurrents of geopolitical conflict and aggressive trade policies. This dynamic has created a challenging landscape where central banks, particularly the U.S. Federal Reserve, are forced to navigate between fighting persistent inflation and avoiding a policy error that could destabilize an already fragile global system.

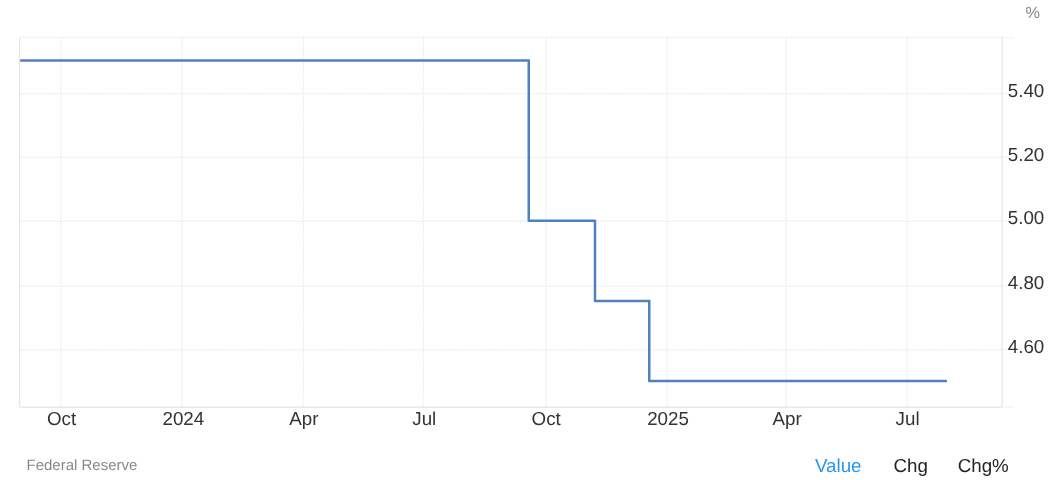

The U.S. Federal Reserve finds itself in a precarious position. At its meeting on July 30, 2025, the Federal Open Market Committee opted to maintain the target range for the federal funds rate at 4.25% to 4.50%. This marked the fifth consecutive meeting without a rate change, a holding pattern adopted despite clear evidence that inflation remains stubbornly above the central bank's 2% target.

The data underscores the Fed's dilemma. Nowcasting figures from the Federal Reserve Bank of Cleveland, updated as of August 11, 2025, show year-over-year Core Consumer Price Index inflation at 3.02%. The Fed's preferred inflation gauge, the Core Personal Consumption Expenditures Price Index, is running at 2.92% year-over-year. These figures are not only significantly above target but are showing signs of re-acceleration, with the annual inflation rate having risen to 2.7% in June, its highest level since February. Analysts at major financial institutions project that this trend will continue, with year-over-year core CPI expected to rise to 3.3% by December 2025.

A significant driver of this persistent inflation is the administration's aggressive trade policy. The imposition of broad tariffs is directly increasing the cost of imported goods, with economists noting that these price increases are now appearing in headline inflation readings. The Fed is thus being asked to use its blunt monetary tools to counteract the inflationary effects of fiscal and trade policy, an inherently difficult and inefficient task.

This complex situation has led the FOMC to acknowledge that uncertainty about the economic outlook remains elevated. In his public statements, Fed Chair Jerome Powell has consistently pushed back against market expectations for imminent rate cuts, particularly one in September, reiterating a data-dependent wait-and-see approach. However, this united front is beginning to show cracks. For the first time since September 2020, the July decision saw two dissenting votes, with Governor Christopher Waller among those favoring an immediate 0.25% rate cut. This dissent signals a growing internal debate about the mounting risks to economic growth from maintaining a restrictive policy stance for an extended period.

Compounding the challenge is the intense political pressure being exerted by the White House. President Trump has publicly and repeatedly criticized the central bank's policy, demanding that the Fed slash interest rates to as low as 1% to stimulate economic growth and, critically, to reduce the soaring costs of servicing the national debt. This public pressure raises concerns about the erosion of the Fed's independence and adds another layer of political complexity to its decision-making process.

The Fed is effectively caught in a vise. On one side, persistent, policy-fueled inflation argues against rate cuts. On the other, moderating economic growth, internal dissent, and extreme geopolitical risks—including an active war in Europe and rising nuclear tensions—argue against further rate hikes. A significant tightening of financial conditions could trigger a recession or a financial crisis, an outcome that would be strategically and politically untenable in the current global environment. This reality creates an effective ceiling on how high the Fed can push interest rates, a dynamic that acts as a "geopolitical put" on monetary policy, limiting the potential downside for risk assets from further aggressive tightening.

While the U.S. grapples with policy-induced inflation, the macroeconomic picture in the Eurozone is markedly different, highlighting a significant divergence between the two economic blocs. According to a flash estimate from Eurostat, the Euro area's headline inflation was stable at 2.0% in July 2025, precisely at the European Central Bank's target. Core inflation, which excludes volatile energy, food, alcohol, and tobacco prices, stood at a relatively benign 2.3%. This stands in stark contrast to the U.S., where core inflation metrics are hovering near 3%.

The primary driver of this divergence is energy. In July, energy prices in the Euro area fell by 2.5% on a year-over-year basis. This reflects the lingering economic drag and base effects from the massive energy price shock that hit the continent following Russia's invasion of Ukraine in 2022. Europe is still contending with the demand destruction caused by that geopolitical event. The U.S., in contrast, is experiencing inflation driven by internal policy choices, namely tariffs that are raising the prices of consumer goods like furniture, toys, clothing, and shoes.

Even within the Eurozone's largest economy, Germany, the inflationary pressures are more subdued. The expected inflation rate for July 2025 is +2.0%, with core inflation anticipated at +2.7%. This divergence in the nature and source of inflation gives the ECB a much clearer policy path than the Fed. With the primary inflationary shock being external and now fading from the year-over-year data, the ECB has greater latitude to adopt a more accommodative or dovish stance to support its economy. The Fed, facing a self-inflicted inflation problem, does not have the same luxury. This structural divergence is likely to contribute to a persistently strong U.S. dollar relative to the euro, with significant implications for trade balances, corporate earnings, and international capital flows.

This complex macroeconomic backdrop has direct and actionable implications for investors.

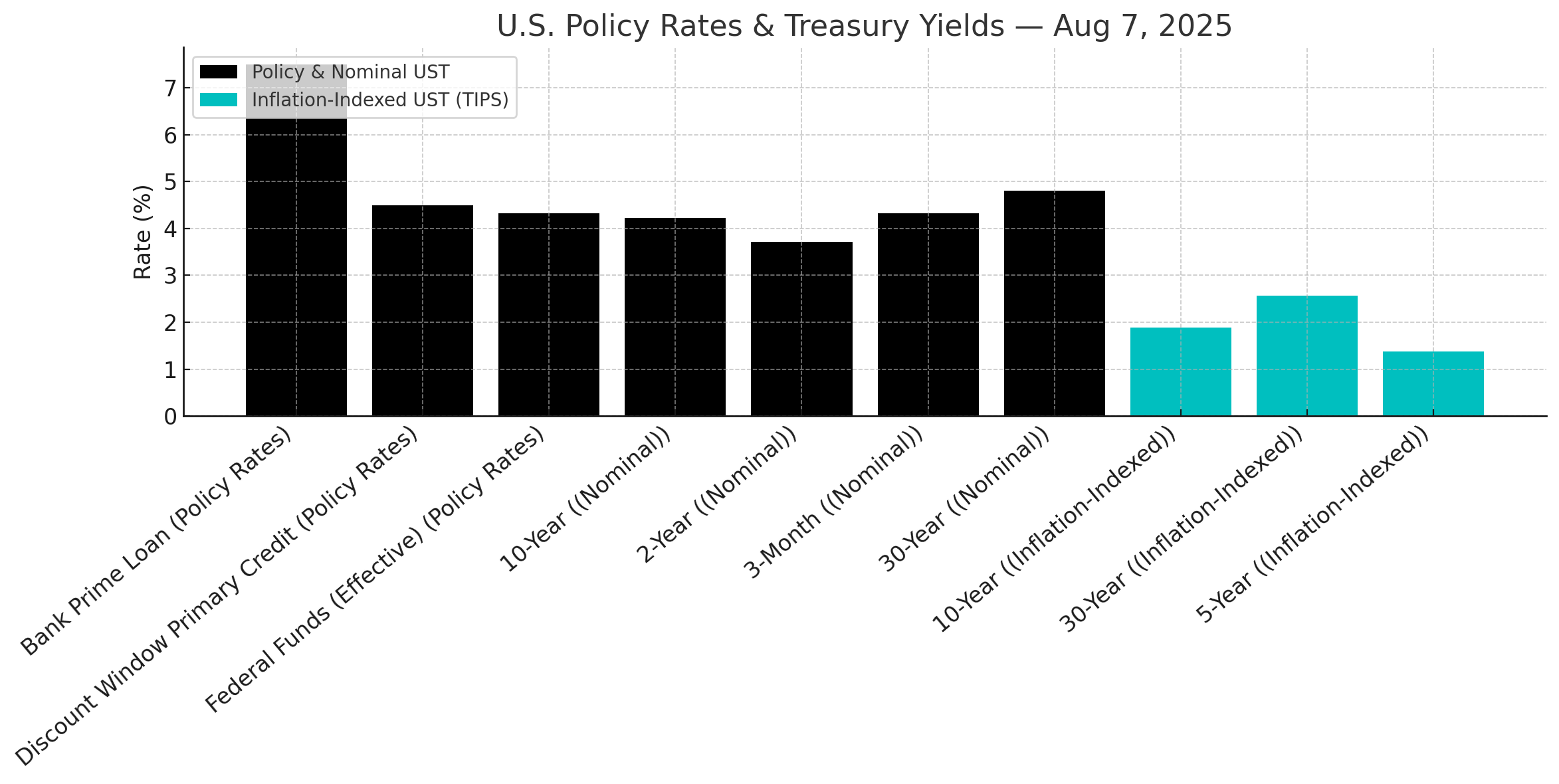

In the fixed income market, the U.S. Treasury yield curve is signaling caution. As of August 7, 2025, the yield on the 3-month Treasury bill was 4.32%, while the 10-year Treasury note yielded 4.23%. This slight inversion, where short-term rates are higher than long-term rates, is a classic market indicator of concern about future economic growth. For investors, the Fed's higher for longer stance, necessitated by inflation, makes short-duration government debt an attractive option for generating yield with relatively low price risk. However, the elevated risk of a policy error by the Fed or a sudden geopolitical shock could trigger a rapid flight to safety, which would cause a rally in long-duration bonds (i.e., their prices would rise and yields would fall). A balanced approach, with exposure to both the short and long ends of the curve, may be prudent.

In the equities market, the environment favors specific sector characteristics. Highly rate-sensitive sectors, such as housing, have seen some modest relief as 30-year fixed mortgage rates have recently dipped to 6.63%. However, with the Fed's policy rate still elevated at 4.25%-4.50%, overall financing costs remain a significant headwind for the sector. The current flat-to-inverted yield curve is also a challenge for the financial sector, which typically profits from borrowing at short-term rates and lending at long-term rates. The most resilient companies in this environment will be those with strong pricing power, enabling them to pass on rising input costs, and those whose products and services are non-discretionary, making them less vulnerable to a slowdown in consumer spending.

Geopolitical risk & reward

The era of the peace dividend that followed the Cold War has unequivocally ended. The world has entered a new period of institutionalized great power competition, marked by active conflict, the collapse of international arms control treaties, and a pervasive sense of instability. This paradigm shift has profound implications for investors. It signals the start of a secular, non-cyclical, and global supercycle in spending on national security. This creates durable, long-term investment opportunities in the companies that provide the essential hardware, software, and services for modern deterrence.

A pivotal event on the geopolitical calendar is the scheduled meeting between U.S. President Donald Trump and Russian President Vladimir Putin in Alaska on August 15, 2025. The stated purpose of the summit is to negotiate an end to the war in Ukraine, which has been ongoing since February 2022. However, the prospects for a genuine and lasting peace appear remote.

According to officials briefed on the matter, President Putin's negotiating position involves a ceasefire in exchange for Ukraine ceding sovereignty over the four territories Moscow claims to have annexed: Luhansk, Donetsk, Zaporizhzhia, and Kherson. This demand aligns with public statements from President Trump, who has hinted that a deal would likely involve some swapping of territories.

This framework is a non-starter for Kyiv and its key European allies. Ukrainian President Volodymyr Zelenskyy has been excluded from the bilateral talks, a move Russia insisted upon, stating that a meeting with Zelenskyy could only happen in the final phase of negotiations. Ukrainian military commanders and European leaders have voiced strong opposition, warning that Ukraine cannot be sidelined from talks concerning its own sovereignty and territorial integrity. Ukrainian forces remain determined to continue fighting, expressing deep skepticism about Russia's willingness to negotiate in good faith.

Viewed through a strategic lens, the Alaska summit appears less a genuine peace initiative and more a calculated geopolitical maneuver. For Russia, it is an attempt to formalize its territorial gains, create a schism between the United States and its European allies, and freeze the conflict on terms favorable to Moscow. For the Trump administration, it represents an effort to deliver on a key campaign promise to end the war and pivot U.S. strategic focus away from a costly and protracted European conflict.

The most probable outcome is not a comprehensive peace treaty but the establishment of a frozen conflict. This would likely reduce the intensity of active fighting but would institutionalize the current frontlines, creating a permanent state of high tension and militarization in Eastern Europe. This outcome would not reduce the need for robust defense and deterrence; on the contrary, it would make it a permanent feature of the European security architecture.

The backdrop to this high-stakes diplomacy is a rapid and dangerous deterioration of the global arms control framework. On August 4-5, 2025, the Russian Foreign Ministry formally announced that it would no longer consider itself bound by its unilateral moratorium on the deployment of intermediate-range missiles. This declaration effectively marks the final death of the 1987 Intermediate-Range Nuclear Forces Treaty, which banned ground-launched missiles with ranges between 500 and 5,500 kilometers. The United States had already withdrawn from the treaty in 2019, citing Russian violations, but Moscow had maintained a self-imposed moratorium on deployment until this announcement.

Moscow has justified this move as a necessary response to the deployment of U.S. missile systems in Europe and the Asia-Pacific region. The announcement was accompanied by a barrage of aggressive rhetoric, particularly from Dmitry Medvedev, the deputy chairman of Russia's Security Council. He characterized the decision as creating a new reality for Russia's opponents and ominously warned them to expect further steps.

This is far more than just rhetoric. Russia has already demonstrated its new capabilities by using the Oreshnik hypersonic intermediate-range missile in a conventional strike against Ukraine in November 2024. President Putin has announced plans to deploy these nuclear-capable systems in neighboring Belarus. Such weapons are considered profoundly destabilizing due to their extremely short flight times—capable of reaching targets in Western Europe in under 15 minutes—and their hypersonic speeds, which make them exceptionally difficult to intercept.

This Russian escalation is part of a dangerous tit-for-tat dynamic. It followed President Trump's announcement that he had ordered the repositioning of two U.S. nuclear submarines in direct response to what he termed Medvedev's highly provocative statements and nuclear threats.

The nearly simultaneous timing of the Alaska summit announcement and the INF moratorium withdrawal suggests a coordinated strategy. This good cop, bad cop approach presents the West with a stark choice: either accept a peace in Ukraine on Russia's terms, as offered by Putin, or face a new, highly dangerous arms race featuring hypersonic missiles, as threatened by Medvedev. This coercive diplomacy is designed to exploit Western risk aversion and fracture the transatlantic alliance. For investors, the critical takeaway is that a genuine, stable peace is highly improbable. Instead, these events signal the formalization of a new, long-term adversarial relationship between Russia and the West. This reinforces the durability of the defense spending cycle, as deterrence, not diplomacy, becomes the primary instrument of statecraft for the foreseeable future.

Investment opportunities

The return of great power competition and the collapse of the post-Cold War security order are translating directly into a robust, long-term investment cycle in the defense and cybersecurity sectors.