[INTEL REPORT] Cartel sanctions and market volatility

Cartels, sanctions, and state actors are reshaping global agriculture and pharmaceuticals

Table of contents:

Introduction.

From agriculture to pharmaceuticals.

Cartel sanctions and agricultural market dislocation.

Investing in supply chain fortification.

Pharmaceutical relocalization.

The shifting dynamics of global defense and security.

The F-35 program under pressure.

Europe's strategic rearmament.

The long-term bet on Ukraine's reconstruction.

Market sentiment and capital allocation signals.

The Miami international holding IPO.

The 2025 IPO pipeline.

Portfolio construction.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

A confluence of geopolitical shifts, protectionist trade policies, and escalating conflicts is fundamentally reshaping the global economic order. Today’s report provides an in-depth analysis for institutional investors, moving beyond headline events to identify the durable, investable macro themes emerging from this new landscape.

The analysis reveals a paradigm shift characterized by three core trends: the weaponization of global supply chains, the fragmentation of long-standing security alliances, and a strategic imperative for the onshoring of critical industrial capacity. These trends are creating a new set of winners and losers across multiple sectors, presenting significant opportunities for capital appreciation and demanding a rigorous reassessment of portfolio risk.

The primary investment theses derived from this analysis are as follows:

The weaponization of supply chains: U.S. sanctions targeting Mexican cartels' deep entanglement in the agricultural sector will disrupt key produce markets, creating a structural opportunity for producers in more stable regions, particularly South America. Simultaneously, a U.S. policy pivot to secure its pharmaceutical supply chain through onshoring initiatives will create powerful tailwinds for domestic drug and active pharmaceutical ingredient manufacturers and the contract manufacturing organizations that support them. This environment also mandates increased corporate spending on sophisticated supply chain security and compliance solutions, benefiting the technology and service providers in that space.

The fragmentation of global defense: U.S. trade policies are placing unprecedented strain on the F-35 fighter jet program, the cornerstone of Western air power. The resulting friction with key allies is undermining the program's economic model and creating a historic opening for European defense contractors. This dynamic is accelerating a strategic rearmament within Europe, favoring indigenous platforms and fostering a more sovereign continental defense industrial base. Concurrently, the prospect of a resolution to the conflict in Ukraine brings into focus a multi-trillion-dollar reconstruction effort, positioning U.S. and European infrastructure, energy, and materials companies for a generation of growth.

Shifting capital market sentiment: The highly successful Initial Public Offering of Miami International Holding, the first by a U.S. exchange in 15 years, signals a broadening of investor risk appetite beyond the narrow confines of technology and biotech. This suggests a healthier, more fundamentally driven capital market environment, potentially unlocking a pipeline of mature, high-quality companies and indicating renewed strength in the financial services and market infrastructure sectors.

Let’s synthesize these interconnected events into a series of portfolios to capitalize these long-term structural shifts. Besides you can go deeper in these topics by checking:

And also:

From agriculture to pharmaceuticals

Government policies and the actions of non-state actors are increasingly being used as instruments of strategic influence, transforming global supply chains from pathways of commerce into arenas of competition. This weaponization is creating dislocations in established trade patterns, forcing a strategic reassessment of risk and resilience across industries. For investors, this disruption creates a clear and durable set of opportunities, rewarding companies that provide stability, security, and domestic production capacity in critical sectors like agriculture and pharmaceuticals.

Cartel sanctions and agricultural market dislocation

The recent sanctions imposed by the U.S. Department of the Treasury's Office of Foreign Assets Control against the Mexican criminal organizations Cárteles Unidos and Los Viagras represent far more than a standard law enforcement action. They are a direct intervention into the agricultural economy of Michoacán, one of Mexico's most vital food-producing states, and a clear signal of a new, more aggressive U.S. enforcement posture. These cartels are not peripheral actors; they areembedded in the region's lucrative agricultural sector, engaging in rampant and violent extortion of farmers, packers, and exporters involved in the production of high-value crops like avocados, citrus, and mangoes. The violence and instability created by these groups are so severe that they have previously led to temporary suspensions of avocado exports to the United States after U.S. agricultural officials received direct threats.

This action is part of a broader strategic shift in U.S. policy, which is now employing financial tools like the Fentanyl eradication and narcotics deterrence off Fentanyl act to target not just the cartels themselves, but also the legitimate financial institutions and businesses that facilitate their operations, knowingly or not. This creates an environment of heightened scrutiny and significant compliance risk for any company involved in Mexican commerce.

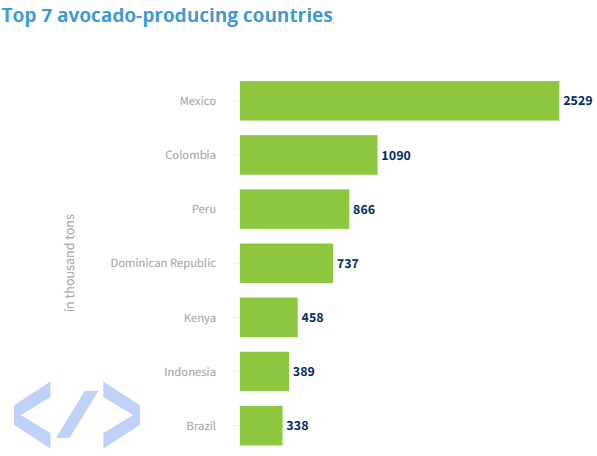

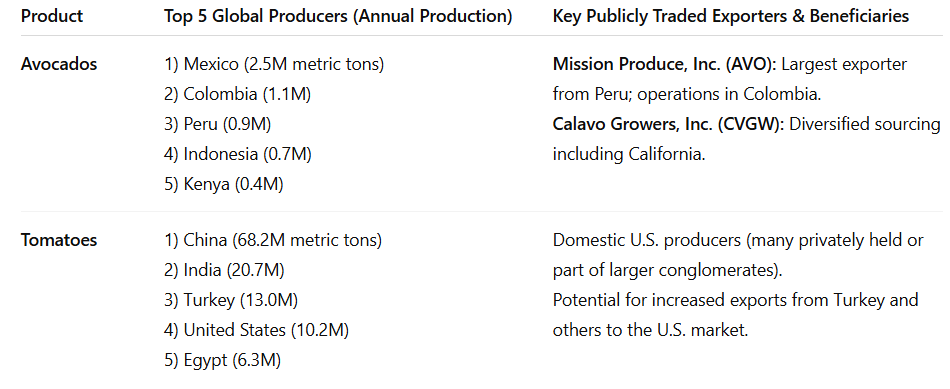

The market impact of this disruption cannot be overstated. Mexico is the undisputed global leader in avocado production, accounting for approximately 30% of the world's supply, with the state of Michoacán serving as the industry's epicenter. The country is also a dominant exporter of tomatoes and mangoes, with the United States being the primary destination for these agricultural products, absorbing roughly 60% of Mexico's total agricultural exports. The sanctions, combined with the underlying violence and extortion they aim to combat, will inevitably introduce significant friction into this critical supply chain, leading to price volatility, potential shortages, and a strategic imperative for U.S. importers to diversify their sourcing away from these high-risk regions.

This dislocation creates a clear structural opportunity for Mexico's primary agricultural competitors. In the global avocado market, Colombia and Peru rank as the second and third-largest producers, respectively, and have been rapidly increasing their export capacity to markets in Europe and the United States. In the tomato market, while the U.S. has substantial domestic production, sustained price increases or supply interruptions from Mexico would benefit American producers as well as other global exporters like Turkey. For mangoes, key competitors poised to capture market share include India, China, and Thailand.

The core investment thesis is that the U.S. sanctions will act as a catalyst, accelerating a long-term strategic diversification of agricultural sourcing away from cartel-affected regions of Mexico. Publicly traded companies with significant, vertically integrated production and export operations in competing, more stable geographies—particularly in South America—are uniquely positioned for sustained growth.

Mission Produce, Inc. (NASDAQ: AVO): As the world's largest supplier of Hass avocados and the single largest exporter of avocados from Peru, Mission Produce is perfectly positioned to fill any supply gap created by disruptions in Mexico. The company's significant and growing vertical integration in Peru and Colombia provides the kind of supply chain reliability and security that major U.S. food retailers and distributors will increasingly demand. Their investments in advanced post-harvest technologies like hydrocooling further enhance product quality and shelf life, strengthening their competitive advantage.

NASDAQ: AVO Calavo Growers, Inc. (NASDAQ: CVGW): While Calavo Growers has operations in Mexico, its diversified sourcing model, which also includes significant procurement from California and other growing regions, provides a degree of operational flexibility. This diversification could allow the company to pivot its sourcing strategy to mitigate risks and potentially benefit from overall market price increases driven by Mexican supply constraints.

NASDAQ: CVGW

The U.S. Treasury's actions are creating more than just a temporary supply shock; they are imposing a tangible geopolitical risk premium on agricultural goods sourced from regions where cartels exert significant influence. This is not a transient issue like a weather event but a persistent, structural risk embedded in the local economy. The fact that U.S. government officials have been directly threatened, leading to past import halts, demonstrates that this risk is material and can sever trade flows with immediate effect. For large corporate buyers, such as national supermarket chains and restaurant suppliers, supply chain volatility is anathema. An empty shelf or the removal of a popular menu item like guacamole represents a direct loss of revenue and customer goodwill. Consequently, these buyers will be increasingly willing to sign long-term contracts or even pay a modest premium for produce from suppliers in more stable regions to guarantee a secure and predictable supply. This dynamic fundamentally alters the competitive landscape. Producers in countries like Colombia and Peru can now market their products not just on quality and price, but on the crucial attributes of stability and security of supply. This provides a powerful new selling proposition and the potential for higher, more stable margins for well-positioned companies like Mission Produce.

Investing in supply chain fortification

The sanctions against Mexican cartels highlight a much broader and more systemic vulnerability: the increasing susceptibility of global supply chains to geopolitical shocks. The formal designation of these cartels as Foreign Terrorist Organizations and Specially Designated Global Terrorists elevates the compliance burden for any corporation with exposure to the region. This is not merely a suggestion to be cautious; it imposes a legal mandate. U.S. and international firms doing business in or with Mexico must now implement exceptionally rigorous due diligence processes to ensure they do not, even inadvertently, transact with sanctioned entities, their known affiliates, or shell companies. Under the governing statutes, OFAC can impose severe civil penalties based on a strict liability standard, meaning that ignorance of a counterparty's illicit connections is not a defense.

This new reality renders traditional corporate compliance and supply chain management controls insufficient. The challenge is compounded by the explicit warning from the U.S. government that these criminal organizations exhibit a convergence with other designated terrorist groups and even antagonistic foreign governments, deliberately obfuscating their financial trails. Consequently, corporations across all sectors will be compelled to significantly increase their investment in a new generation of supply chain security, visibility, and compliance solutions.

The evolution of this threat from a logistical problem of potential delays to a legal and financial crisis of counter-terrorist financing and anti-money laundering compliance is a critical development for investors. This shift elevates the purchasing decision for security and compliance solutions from the purview of a mid-level logistics manager to the highest levels of the C-suite, including the Chief Compliance Officer, the General Counsel, and the Chief Financial Officer. These executives are tasked with mitigating existential corporate risks, not just operational inefficiencies. As a result, they command larger, less price-sensitive budgets and will prioritize best-in-class, data-intensive solutions over cheaper, less comprehensive alternatives. A simple GPS tracker on a truck is no longer adequate when a company must understand the ultimate beneficial ownership of the trucking firm, the banks it uses, and its network of associates to ensure compliance. This creates a high-value market for firms that can provide the deep, data-driven intelligence necessary to navigate this new compliance minefield. Their value proposition is not merely efficiency, but existential risk mitigation, a service that commands a significant premium.

The investment thesis is to invest in the picks and shovels of this new era of supply chain resilience. Companies providing the essential technologies and services that enable corporations to map, monitor, secure, and ensure compliance across their global supply networks are poised for a period of sustained, non-cyclical growth.

Physical & logistics security: Companies that provide tangible security for goods in transit are on the front lines of mitigating these risks. Prosegur (BME: PSG), a global security firm, offers a comprehensive suite of relevant services, including 24/7 live monitoring from its Security Operations Center, GPS and GSM cargo tracking, deployment of global incident response teams, and security escorts for high-value cargo. These services directly address the physical threats of theft and extortion highlighted by cartel activities.

BME: PSG Data, analytics & compliance platforms: The ability to vet partners and monitor transactions is now paramount. Dun & Bradstreet (NYSE: DNB) is a foundational provider of commercial data and analytics that help companies mitigate financial and counterparty risk, which is critical for screening suppliers and customers to ensure compliance with complex sanctions regimes. Specialized platforms like

Resilinc and Exiger offer more targeted, end-to-end supply chain mapping, real-time disruption monitoring, and risk management solutions that are becoming indispensable for global corporations.

NYSE: DNB Software & technology: The technological backbone of a modern supply chain is a key area of investment. Trimble (NASDAQ: TRMB) provides positioning, monitoring, and fleet management technology that is used by 99% of the top 200 trucking fleets in the U.S., offering the real-time visibility necessary to manage complex logistics networks.

Manhattan Associates (NASDAQ: MANH) produces sophisticated software for supply chain and inventory management, which is essential for optimizing operations and building resilience in the face of potential disruptions.

NASDAQ: TRMB

Pharmaceutical "relocalization"

A clear and deliberate policy shift is underway in the United States to reduce its critical dependence on foreign nations for essential medicines. The announcement of potential tariffs on pharmaceutical imports, specifically targeting generic products under the national security provisions, coupled with a presidential executive order to build up a strategic reserve of domestically sourced Active Pharmaceutical Ingredients (APIs), signals a strategic realignment of the nation's drug supply chain.