[INTEL REPORT] 2026 begins with easing inflation and rising war budgets

Ukraine, the Middle East, and new flashpoints collide with record deficits

Table of contents:

Introduction.

Geopolitical context and conflict overview.

War in Ukraine.

Israel–Hamas war and iran tensions.

U.S.–Venezuela conflict emerges.

Inflation and energy markets.

Growth and recession signals.

Monetary policy.

Sovereign debt and fiscal trends.

Implications for investment in U.S. and european assets.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

The start of 2026 finds global markets between stabilization and renewed disruption. While inflation has begun to moderate and monetary policy is entering a more flexible phase, investors are simultaneously contending with important geopolitical events, record peacetime defense budgets, and expanding sovereign debt burdens.

Across NATO and the European Union, rearmament is no longer a political debate. Defense outlays have surged to levels not seen since the Cold War, and governments have signaled further increases through the end of the decade. This expansion is occurring alongside new forms of fiscal accommodation, such as looser EU deficit rules for security expenditures and bipartisan consensus in the U.S. around increased military spending. These developments are fundamentally altering sovereign bond markets, with implications for duration risk, credit quality, and central bank behavior.

More about global risks here:

Meanwhile, the economic costs of conflict are not evenly distributed. Countries on the eurozone periphery face additional pressures as they are called to contribute both militarily and financially to common defense efforts, including support for Ukraine. Energy-importing nations remain vulnerable to price shocks and supply chain interruptions, especially amid the prospect of prolonged instability in Eastern Europe, the Middle East, or the Caribbean. These stressors compound existing concerns over debt sustainability, fiscal credibility, and political fragmentation, all of which are now influencing spreads, investor sentiment, and institutional mandates.

For capital allocators, the central challenge is to identify where policy responses are credible, where geopolitical outcomes are path-dependent, and where structural shifts may present new investment regimes. While certain risks—such as a sovereign default among G7 nations—remain low probability, the pricing of those risks is increasingly asymmetric.

Geopolitical context and conflict overview

As of early 2026, the global geopolitical landscape is increasingly fragmented, shaped by persistent armed conflicts, unresolved territorial disputes, and a resurgence of competition. Tensions between major global actors—particularly the United States, Russia, China, and key regional powers—have escalated, with multiple conflict zones driving fiscal and strategic responses. These dynamics are no longer isolated to defense policy but are deeply interwoven with energy security, debt trajectories, and macroeconomic stability. Among the most consequential flashpoints for investors are the enduring war in Ukraine, expanding military commitments in the Middle East, and recent confrontations involving Venezuela. Each of these developments continues to reshape risk perceptions, capital flows, and asset pricing in global markets.

War in Ukraine

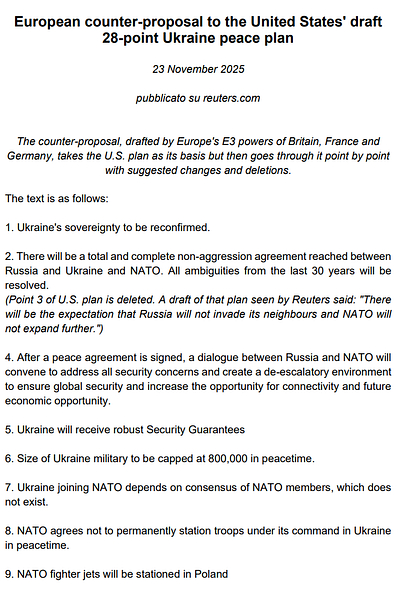

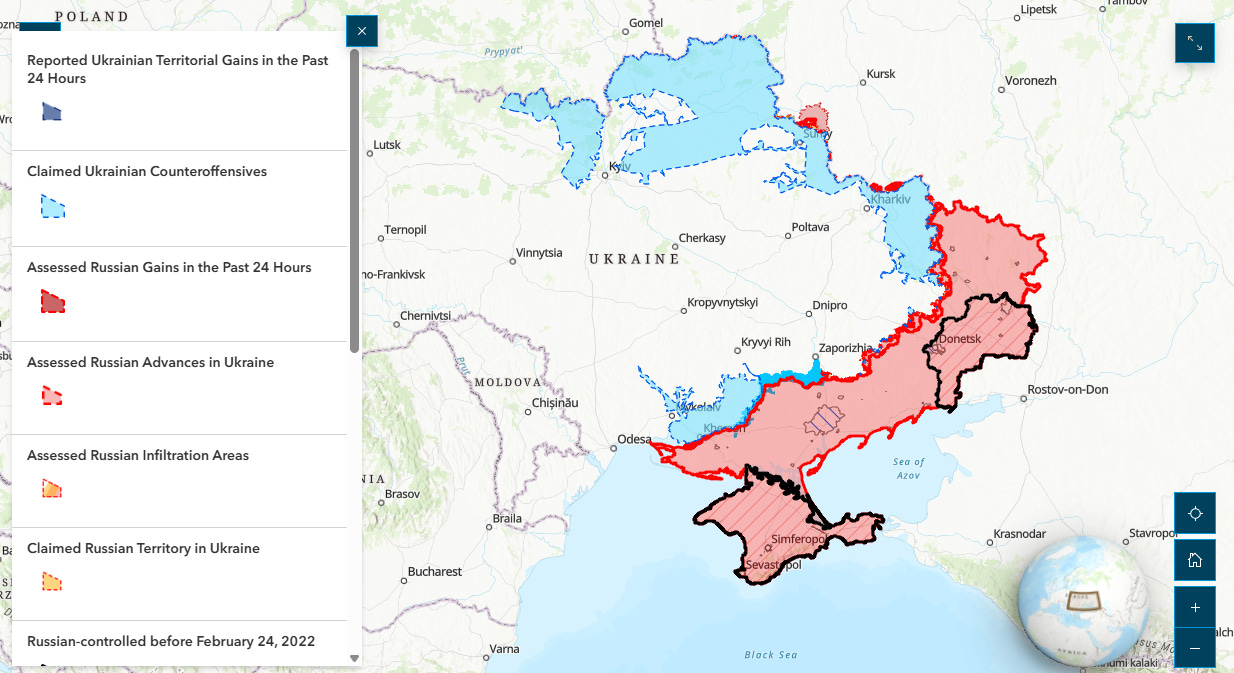

The conflict between Russia and Ukraine remains unresolved entering 2026, despite various negotiation initiatives. In late 2025, the U.S. administration under President Trump pursued a “28-point peace plan” to end the war, even holding a high-profile summit in Alaska with Russian officials.

While U.S. officials optimistically claimed substantial progress and even suggested a deal was 95% complete, these assertions proved misleading. According to former UN official Juan Antonio de Castro, Trump was not truthful about a 95% deal; a lasting peace is still far off. The major sticking point is territorial control in Donbas: Russia refuses to relinquish occupied areas and Ukraine refuses to concede, leaving talks at an impasse.

European leaders and Ukraine itself have been wary of Washington’s proposals, which were viewed as skewed toward Moscow’s terms (Ukraine’s foreign minister called the U.S. plan a capitulation). Indeed, The Guardian reported that the 28-point plan sparked intense debate and deep concern, temporarily distracting from other issues.

Ultimately, no peace agreement was reached by year-end 2025, and fighting continues into 2026. Russia even intensified bombardments of Ukrainian cities after diplomatic talks stalled, underscoring the grim reality that Moscow still sees military force as its primary lever.

For Europe, this protracted war has been economically draining. The EU’s efforts to aid Ukraine – from military support to massive financial packages – are straining public finances. Plans to use frozen Russian assets for reconstruction faltered due to legal objections, leading the European Commission to consider a new €90 billion joint EU loan for Ukraine. Critics warn that such debt could break the economy, with one estimate that it could cost Europe nearly 1% of GDP over the next 3–5 years if not repaid. That is a huge burden given the eurozone’s growth is barely 1% annually. European leaders appear resigned to a long war scenario – some even reportedly prefer prolonging the conflict, hoping to weaken Trump politically. In effect, Europe is caught in a dilemma: supporting Ukraine’s defense and holding a hard line on Russia, yet risking recession and social spending cuts at home to finance it.

From an investor standpoint, the Ukraine war introduces persistent macroeconomic uncertainty for Europe. Energy security remains a concern (though gas supplies have diversified, any escalation could disrupt remaining transit or push prices up). Defense budgets are swelling across EU nations, pushing fiscal deficits higher. The European Commission confirms that rising defence spending is a key factor lifting government expenditure and debt ratios into 2026. Meanwhile, EU unity is being tested: not all member states share the same tolerance for economic pain, raising long-term sovereign risk differentials (e.g. highly indebted countries like Italy face higher borrowing costs if growth stays weak). These factors merit caution on European assets until a clear path to peace – or at least a stable ceasefire – emerges.

Israel–Hamas war and iran tensions

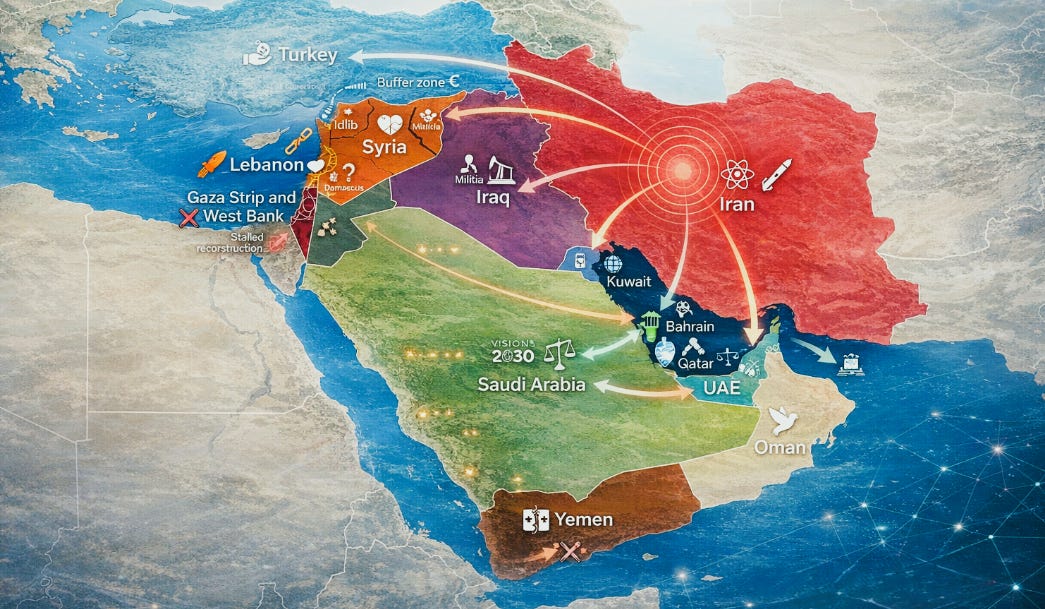

The Middle East remains another flashpoint with potential global spillovers. In the aftermath of the Israel–Hamas war that erupted in October 2023, Gaza has been devastated and fighting continued through 2024–25. By late 2025, despite international pressure for a ceasefire or political solution in Gaza, Israel’s stance hardened around eliminating Hamas entirely before any settlement. Peace efforts in Gaza have essentially stalled. A brief pause allowed hostage releases, but Israeli forces quickly resumed operations, aiming to neutralize Hamas’s presence in Gaza completely. Proposals for an interim international administration in Gaza or other diplomatic fixes have made little headway. This protracted conflict keeps the region on edge and poses ongoing risks of humanitarian crisis and regional destabilization.

More alarming for global markets is the rising tension between Israel and Iran. In mid-2025, Israel and the United States reportedly conducted a short, intense military confrontation with Iran – a 12-day war – involving strikes on Iranian targets (such as nuclear facilities). Although that conflict was contained and concluded without full-scale war, it failed to resolve underlying issues. Iran has since been rearming rapidly, bolstered by its missile program and proxy networks, while Israel grows increasingly anxious about Tehran’s nuclear potential. In a recent meeting at Mar-a-Lago, Israeli Prime Minister Netanyahu privately pressed President Trump on the possibility of further strikes on Iran’s military infrastructure in 2026. Trump – a close ally of Netanyahu – has signaled support for Israel’s security, and “all options” remain on the table, including preemptive military action. Analysts warn that any “round two” attack on Iran could provoke serious retaliation. Iran’s leadership has issued new threats against both Israel and U.S. bases in the region, and anti-regime protests within Iran complicate the picture.

For investors, the Israel–Iran standoff is a major tail risk. A direct conflict could disrupt Middle Eastern oil production and shipping routes overnight, sending crude prices skyward. Even absent an actual war, the situation injects a risk premium into energy markets and could spur defense spending in the region (benefiting defense contractors) as well as demand for safe-haven assets. So far, markets have largely priced in only a modest risk: the global economy in 2025 navigated the Ukraine and Middle East crises better than feared. However, geopolitical miscalculation – for instance, an Israeli strike on Iranian soil leading to closure of the Strait of Hormuz – would have outsized impacts on inflation and growth. Portfolio hedges against oil shocks and Middle East instability remain prudent heading into 2026.

U.S.–Venezuela conflict emerges