Smooth signals, sharp edges

From polynomials to real-time trend detection—reworking the Savitzky-Golay filter for streaming financial data

Introduction

As you know, financial markets often resemble a theme park designed by a hyperactive toddler with a flair for chaos. Prices rocket skyward, nosedive without warning, and occasionally fling themselves into loop-the-loops while screaming, "Wheee!" Market participants grip their metaphorical safety bars, praying to exit with a profit—or at least enough lunch money to survive another ride.

Traders, analysts, and mathematicians have spent decades trying to impose order on this financial mayhem, crafting models and frameworks that range from rigorously structured to something that looks suspiciously like a potion recipe scrawled in your grandma’s basement. Some of these approaches feel like arcane magic; others are surprisingly simple—like the paper I stumbled upon a couple of weeks ago, which you’ll find at the end of this article.

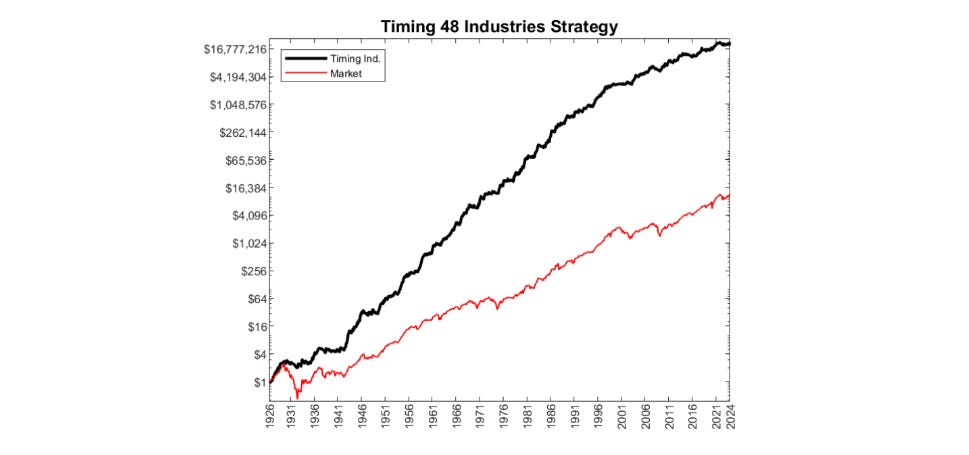

But before we get there, let’s cut through the noise with just one rule—tested across a century of market history—that has consistently delivered profit: