[INTEL REPORT] Special report on interest rates

FED's dovish pivot and geopolitical situation

Table of contents:

Introduction.

The new monetary regime.

The federal reserve's dovish pivot.

Stagnation signals and persistent inflation.

The weakening U.S. labor market.

Dominant market risks.

Historical precedent vs. modern dynamics.

Political pressure and internal dissent at the Fed.

U.S. sovereign debt and its market implications.

Geopolitical hotspots and energy market rebalancing.

Core portfolio strategy for late 2025.

Reassessing the equity allocation.

Fixed income re-engagement.

The role of hard assets and alternatives.

Investment themes and timing.

Winning sectors for the new cycle.

Long-term opportunity.

Gold and strategic hedge.

Capitalizing on a weaker U.S. dollar.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

An era of disinflation, predictable central bank support, and the steady tailwind of ever-lower interest rates has come to an end. From the aftermath of the Global Financial Crisis through the pandemic stimulus wave, monetary policy played a familiar role—suppressing volatility, compressing yields, and cushioning every downturn with liquidity injections. Asset allocators grew accustomed to the idea that markets could rely on a Federal Reserve acting as both stabilizer and guarantor of financial conditions.

That era is now over. What we are entering is not a continuation of the old paradigm with slightly different parameters, but a new monetary regime defined by contradictions, fragility, and constraints that fundamentally alter the investment landscape. The linchpin of this transition is the Federal Reserve’s September 2025 pivot: the first rate cut in nearly a year, executed not from a position of confidence but as a concession to worsening conditions. The Fed has framed this as a “risk-management” cut, yet the subtext is unavoidable—its priorities have shifted, its independence is under question, and its traditional playbook no longer fits the economic reality it confronts.

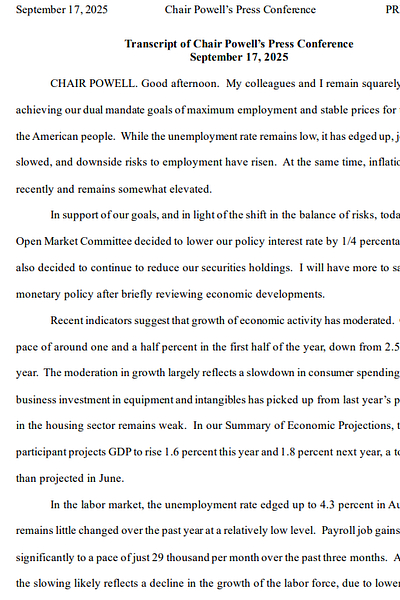

You can see the last Powell’s intervention here:

Transcription below:

Unlike past easing cycles, this one does not arrive with a clean narrative of crisis followed by stabilization. Instead, it unfolds against a backdrop of conflicting signals: inflation that refuses to retreat to target, growth that is visibly slowing, labor markets that are beginning to crack, and a debt burden so large that it exerts gravitational force on policy choices. Monetary policy is being asked to square the circle—support growth, protect employment, and preserve debt sustainability—all while tolerating inflation above the official target. This is not a cycle of optional adjustments; it is a reactive, constrained maneuver forced by structural imbalances that have been building for years.

The implications for investors are key. Every Fed rate-cutting cycle of the 21st century has coincided with recession. Yet equity valuations remain elevated, propped up by a handful of mega-cap firms while broad market fundamentals deteriorate. Fixed-income markets are caught between the promise of falling policy rates and the threat of relentless Treasury issuance to refinance trillions in government debt. Hard assets such as gold are no longer fringe hedges but strategic necessities, given the credibility risks now haunting central banks. Currency markets, too, face a decisive shift as a structurally weaker dollar rewrites the terms of global capital flows.

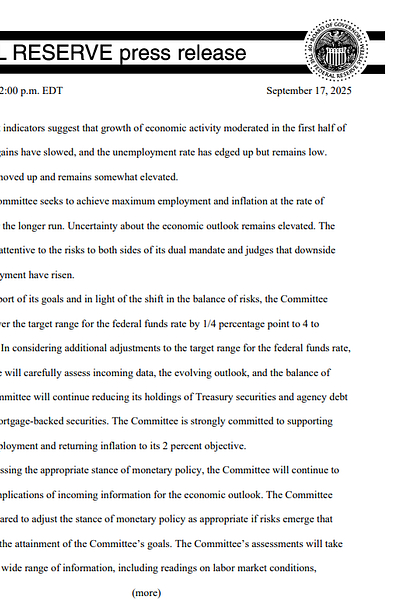

Check more about the press realease here:

This regime change is not merely about monetary policy; it is about the erosion of assumptions that defined the last decade. The presumption that inflation would always trend lower, that fiscal dominance was a distant problem, that the Fed was immune to political interference, and that liquidity alone could restore confidence—each of these pillars has been weakened, if not outright dismantled. In their place stands an environment where investors must think in terms of resilience, optionality, and defense against systemic shocks.

To navigate this new terrain requires abandoning the habits of the disinflationary era. Buy the dip and passive index exposure will no longer suffice. Instead, the successful investor will be the one who recognizes that the rules of the game have changed—who reallocates away from crowded growth trades, who locks in fixed-income opportunities before yields fall, who holds core positions in gold and other real assets, and who seizes undervalued segments like small-cap equities and international markets poised to benefit from dollar weakness.

The Fed’s dovish pivot and its unusual context, the stagnation signals coupled with persistent inflation, the weakening labor market that has forced policymakers’ hand, and the structural risks tied to debt, politics, and geopolitics. From there, it distills the implications into a coherent portfolio strategy designed not for the world we knew, but for the volatile and uncertain environment now taking shape.

The transition underway is not cyclical—it is structural. It demands a recalibration of expectations, a restructuring of allocations, and above all, a recognition that the foundation of investment strategy has shifted beneath our feet. The question is no longer whether the Fed can engineer a soft landing. The question is how investors will adapt to a regime where the central bank itself is constrained, credibility is fragile, and history’s precedent points toward turbulence ahead.

The new monetary regime

The macroeconomic foundation for investment strategy has fundamentally changed. The Federal Reserve's policy pivot is not a proactive measure from a position of strength but a reactive move forced by a deteriorating economic reality. Understanding the nuances of this shift—the conflicting data, the underlying weaknesses, and the constraints on policymakers—is one of the most important variables for successful capital allocation.

The federal reserve's dovish pivot

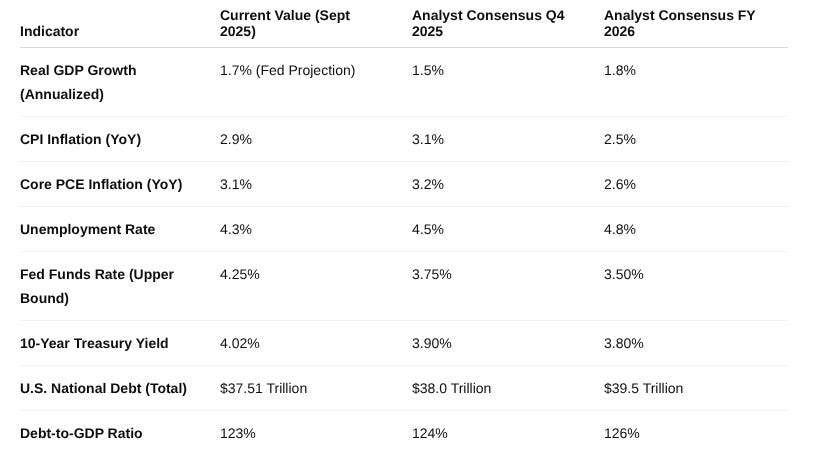

At its September 2025 meeting, the Federal Open Market Committee initiated its first interest rate cut in nearly a year, reducing the target range for the federal funds rate by 25 basis points to 4.00%-4.25%. This move marks a definitive end to the tightening cycle and a formal shift in the central bank's priorities.

Chairman Jerome Powell has carefully framed this decision not as a response to an imminent crisis, but as a risk-management cut. The Committee's official statement provides the critical context, highlighting a change of balance of risk and explicitly judging that downside risks to employment have risen. For the first time in this cycle, the labor market has been elevated above inflation as the Fed's primary near-term concern.

This policy easing occurs under highly unusual circumstances. The cut was delivered even as Powell acknowledged that inflation has increased and remains something elevated, with the latest Consumer Price Index reading at a stubbornly high 2.9%. The Fed has effectively demoted its 2% inflation target to a longer run objective, signaling a significant tolerance for above-target price pressures in its pursuit of stabilizing the labor market.

The forward guidance from the Fed reinforces the expectation of a sustained easing cycle, not a mere one-off adjustment. The Committee's own Summary of Economic Projections, colloquially known as the dot plot, reveals a median expectation among members for the fed funds rate to fall to a range of 3.50%-3.75% by the end of 2025. This implies at least two additional 25-basis-point cuts in the year's remaining two meetings. Looking further, the median projection sees rates falling to a range of 3.25%-3.50% by the end of 2026, signaling a clear path of continued easing. This clear signal of future easing provides a crucial directive for fixed-income and currency markets.

Stagnation signals and persistent inflation

Chairman Powell's description of the U.S. economy as exhibiting highly unusual behavior is a candid admission of the conflicting and confusing data confronting policymakers. The traditional economic models are struggling to capture a reality characterized by slowing growth, persistent inflation, and a breakdown in the transmission of monetary policy.

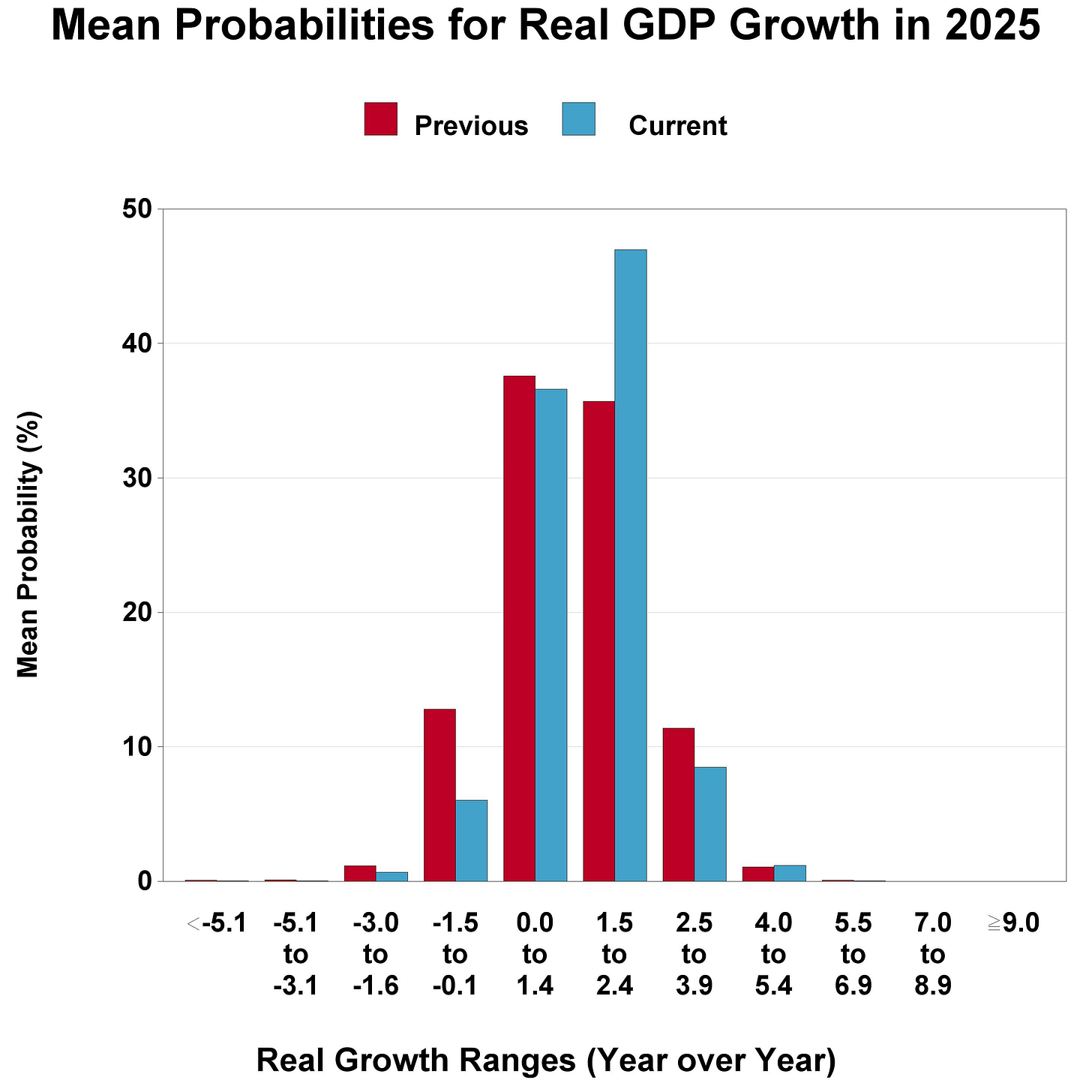

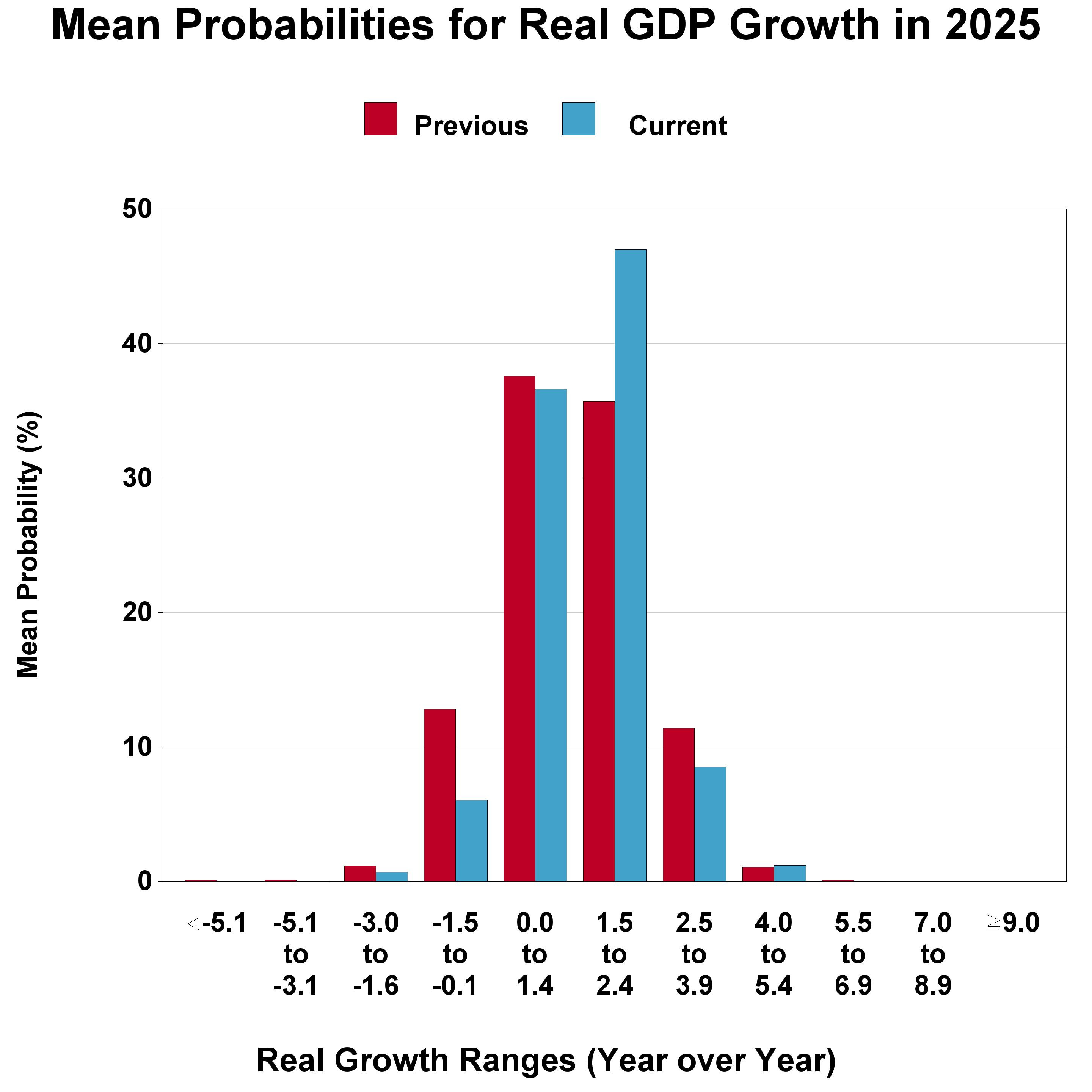

Slowing growth: The Fed has been forced to materially downgrade its forecast for economic growth. It now projects a real GDP growth rate in the 1.7%-1.8% range, a stark contrast to the more robust 3% estimate from the Atlanta Fed's GDPNow model that the market had been watching. The official FOMC statement concurs, noting that growth of the activity economic moderated in the first quarter of the year. This slowdown is not a forecast; it is an observed reality.

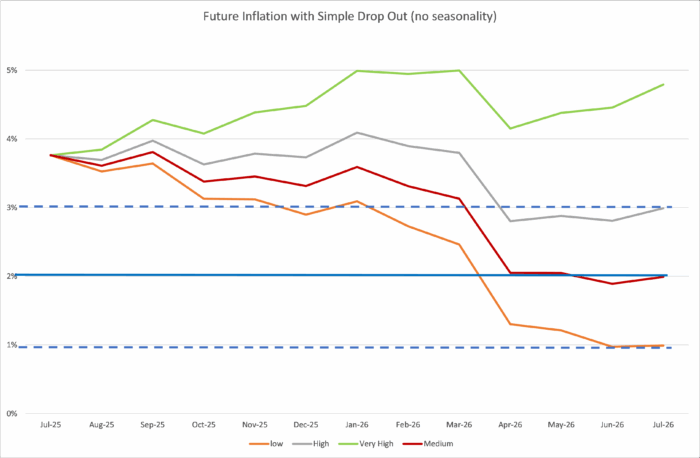

Persistent inflation: While growth is faltering, key leading indicators of inflation suggest price pressures will remain entrenched. The University of Michigan's Survey of Consumers, a historically reliable gauge, shows short-term inflation expectations hovering near 4% and long-term expectations approaching 5%. These consumer beliefs can become self-fulfilling, influencing wage demands and spending habits. More fundamentally, the Producer Price Index, which measures input costs for businesses, has been steadily increasing for both the manufacturing and services sectors. This indicates that companies are facing higher costs for raw materials and inputs, which they will inevitably seek to pass on to the final consumer to protect their profit margins.

Perhaps the most critical and underappreciated variable is the velocity of money. This metric, which measures the rate at which money is exchanged in an economy, has fallen in the most recent quarter. This is a concerning signal. It indicates that even if the Federal Reserve injects more liquidity into the system through rate cuts, that newly created money is not being spent or invested at a normal pace. Instead, it is being hoarded by consumers and corporations, likely out of fear and uncertainty about the economic future. This phenomenon effectively short-circuits the intended stimulative effect of monetary easing. As analyst Ernesto Rebelo notes, liquidity matters, but the velocity of money matters more. This slowdown in velocity explains the highly unusual economic behavior Powell referenced and points to a deep-seated crisis of confidence that monetary policy alone cannot easily solve.

The weakening U.S. labor market

The Fed's explicit justification for its dovish pivot is the tangible deterioration of the U.S. labor market. After months of emphasizing its strength, Chairman Powell made a significant concession in his recent press conference, stating, I can no longer say that the labor market is very solid.

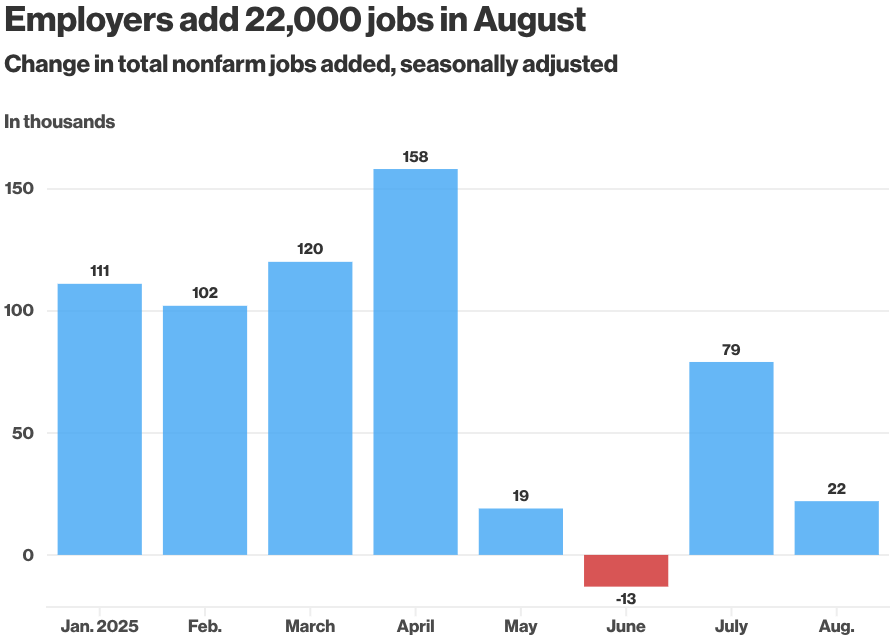

The top-line data supports this shift. The FOMC statement notes that job creation has decelerated and the unemployment rate has increased slightly. The August 2025 jobs report confirmed this trend, with the headline unemployment rate rising to 4.3%, its highest level in nearly four years. This weakness was further underscored by a significant downward revision of previous data, which found that the U.S. had created 911,000 fewer jobs in the 12 months ending March 2025 than previously reported, indicating a more prolonged period of labor market softness.

However, a deeper analysis of the labor market reveals structural problems that go beyond cyclical softness. Youth unemployment, specifically for individuals aged 20 to 24, has reached a deeply concerning level of 10%. This is not merely a cyclical fluctuation; it is indicative of a structural impediment to young workers entering the workforce, with scarring effects that can depress economic growth for years to come.