[INTEL REPORT] Reconstruction or Recolonization?

The plan to rebuild through dispossession and reshape U.S. foreign policy around returns.

Table of contents:

Introduction.

Geopolitical post-conflict middle east.

Trump peace accord.

The “GREAT Trust”.

Regional reconstruction.

Inflation, Interest rates, and the erosion of wealth.

Persistent inflationary environment.

Mapping the policy paths of the Fed, ECB, and PBOC.

Strategic case for hard assets.

Assessing cryptocurrencies as an institutional asset.

U.S.-China strategic competition and the tech decoupling.

China’s economic ascendancy and its global impact.

Chip war escalatation.

Review of previous thesis.

Cracks in the financial foundation.

The corporate credit overhang.

The AI bubble.

Global equity outlook.

Strategic investment.

The nuclear renaissance and the AI power demand.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

Global markets in October 2025 are characterized by a deceptive calm. While surface-level indicators, such as the performance of major equity indices, project an image of resilience and opportunity, a detailed analysis of underlying geopolitical and macroeconomic trends reveals mounting fragilities and significant unpriced risks. The political spectacle surrounding a new peace accord in the Middle East is serving as a distraction from a series of structural challenges that will define the investment landscape for the coming 12-24 months. This report cuts through the prevailing market narrative to identify these core risks and formulate a strategic investment framework designed to preserve capital and capture value in an increasingly uncertain world.

Four primary risks now dominate the global outlook:

The Trump Peace Accord in the Middle East, while presenting a facade of stability, masks deep-seated unresolved issues. It has created a high-stakes, commercially-driven environment centered on the reconstruction of Gaza that is fraught with ethical controversy and significant potential for regional miscalculation, particularly concerning Iran’s response.

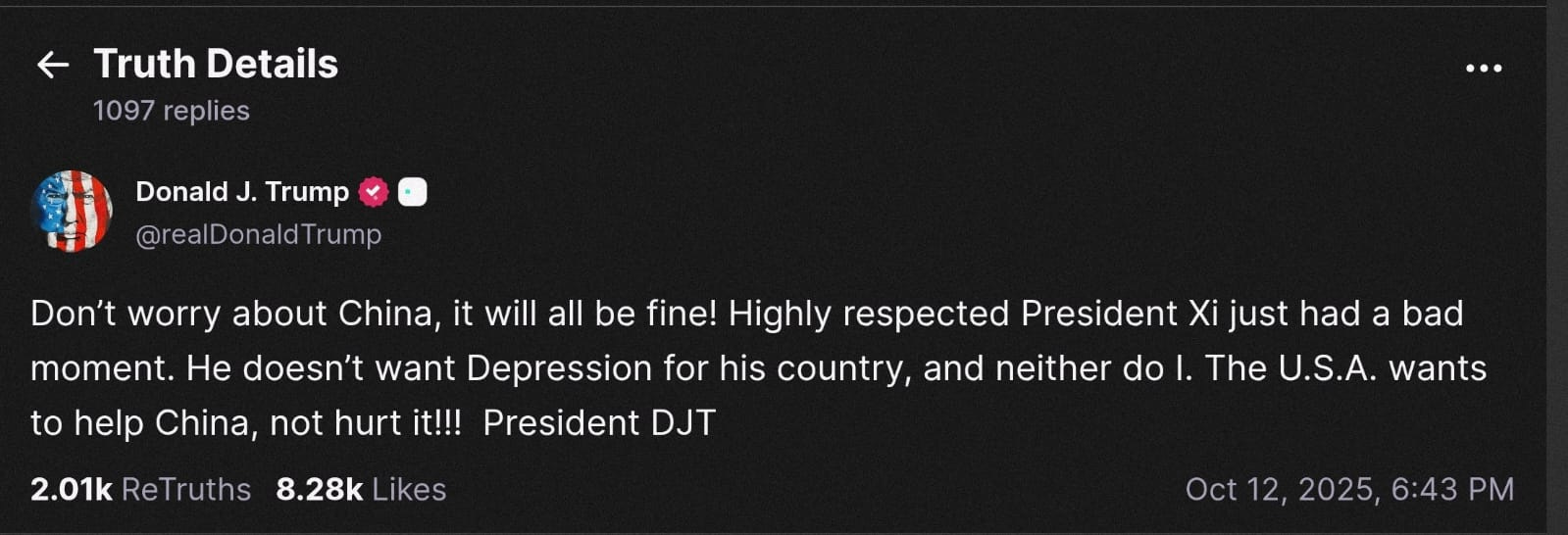

Furthermore, the stability Trump provides on one hand, he takes away on the other. We continue to see more pranks in the purest TACO style, like the one on Friday, October 3rd, which disintegrated >$15 billions. It won’t be the last, although there are still an additional $30 billions to be destroyed from the financial system.

But then…

“haha” how funny The result? 5 billion dissapeared…

Western economies face a structural, not cyclical, inflationary environment. This is driven by continued fiscal expansion and the implicit commitment of central banks to provide liquidity to prevent recession, a policy mix that will systematically erode real returns and the purchasing power of fiat currencies.

Years of accommodative monetary policy have created latent vulnerabilities. A potential bubble in the U.S. corporate credit market is showing signs of stress, with default rates projected to rise. Simultaneously, AI-driven equity valuations have become stretched, increasing the risk of what the Bank of England has termed a sudden correction.

The strategic competition between the United States and China is accelerating, moving beyond tariffs into a full-scale Chip War. This conflict is now manifesting as direct state intervention in corporate ownership, a development that will fundamentally restructure global technology supply chains and create clear winners and losers.

In response to this complex risk matrix, we will look for potential paths for portfolio allocation but before we continue, check this PDF about US market situation:

Geopolitical post-conflict middle east

The global geopolitical risk in October 2025 is dominated by events in the Middle East, where a U.S.-brokered peace accord has ostensibly ended the conflict in Gaza. However, the celebratory political theater, amplified by extensive media coverage, masks a fragile and highly transactional arrangement.

Trump peace accord

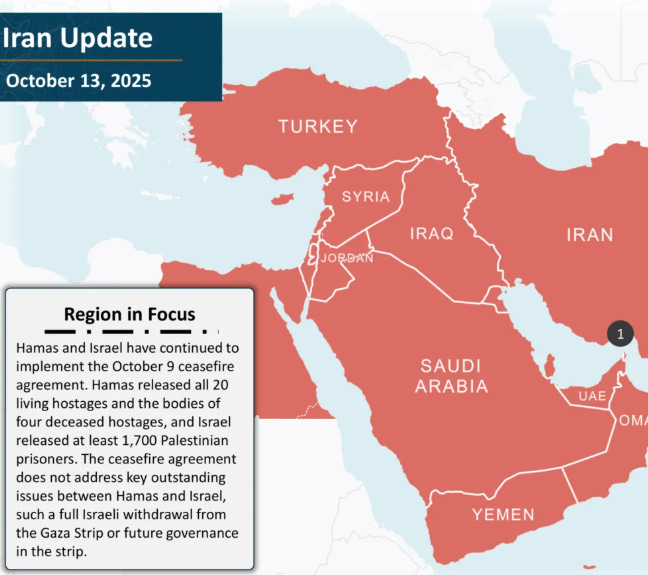

In early October 2025, a diplomatic summit in Egypt culminated in what is being hailed as the Trump peace accord, an agreement that secured a ceasefire and hostage exchange between Israel and Hamas. The event was framed as a personal triumph for former U.S. President Donald Trump, who was acclaimed as a peacemaker for averting a wider regional war. The official Trump declaration for enduring peace and prosperity, signed on October 13 by the leaders of the United States, Egypt, Qatar, and Türkiye, commits the parties to a vision of hope, security, and a shared vision for peace and prosperity.

A closer examination of the agreement, however, reveals a foundation built on principles rather than on concrete, enforceable mechanisms. The declaration emphasizes broad commitments to dialogue, dismantling extremism, and respecting sacred sites, but it conspicuously omits binding procedures for dispute resolution or verification. More importantly, the underlying ceasefire agreement leaves several critical, long-standing issues entirely unresolved. These include the disarmament of Hamas, the terms of a full Israeli withdrawal from the Gaza Strip, and, most crucially, the final structure of future governance in the territory. The absence of a direct Palestinian signatory on the October 13 declaration further underscores concerns about the long-term legitimacy and sustainability of the arrangement.

This structure suggests that the accord should not be viewed as a definitive resolution to the conflict. Rather, it is a transactional ceasefire, a high-risk gambit designed primarily to create a security environment stable enough to enable the next, far more ambitious phase: a massive, commercially-driven reconstruction effort. The peace is not the end goal; it is the prerequisite for the deal.

The “GREAT Trust”

Immediately following the peace accord, the focus has shifted to the Gaza Reconstitution, Economic Acceleration and Transformation aka GREAT Trust. Colloquially dubbed the Riviera de Gaza project, this is not a traditional humanitarian aid program but a vast and controversial economic development plan. The vision, detailed in a 38-page slide deck, is to transform the war-torn territory into a Dubai-style commercial and tourism hub, complete with smart cities, an Elon Musk smart manufacturing zone, advanced data centers, and a Trump Touristic Riviera and Islands featuring artificial islands akin to Dubai’s Palm Islands.

The project’s scale and ambition are matched only by the depth of the controversy surrounding it. The plan has been fiercely criticized as a blueprint for dispossession and a modern form of ethnic cleansing. Critics point to provisions that offer Palestinians financial incentives to volunteer to leave Gaza, with the plan calculating that for every 1% of the population that relocates, $500 million in reconstruction costs are saved. This approach, combined with the complete exclusion of Palestinians from the planning and governance of their own future, has led analysts to label the project as colonialism repackaged in the language of reconstruction.

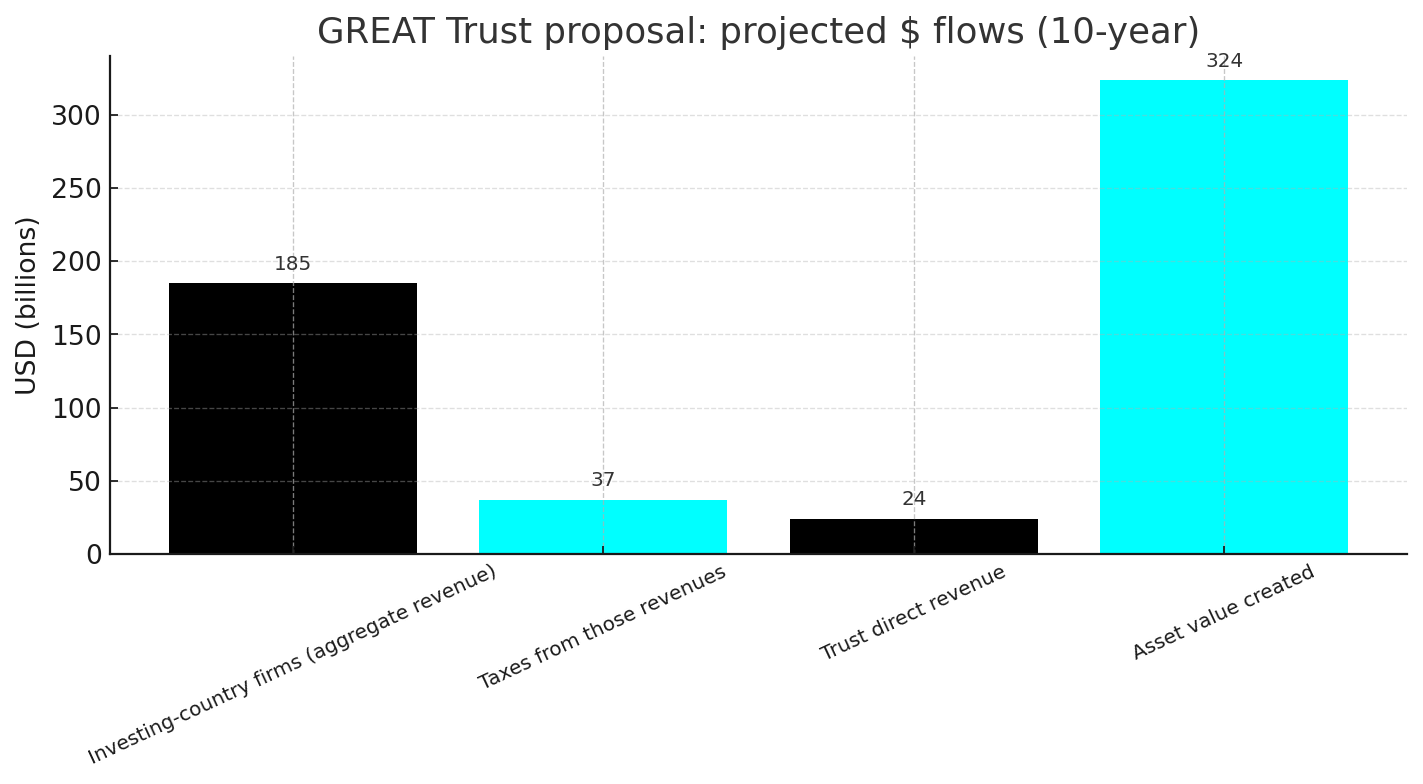

The financial architecture of the GREAT Trust is another point of contention and a source of significant risk. The plan explicitly states that it will not depend on U.S. public funds. Instead, the enormous capital requirements will almost certainly have to come from the Gulf states. The project’s marketing materials appear designed to whet the appetite of Gulf political and economic elites to both endorse and invest in it, borrowing architectural motifs from Riyadh and Dubai and even naming proposed infrastructure after Gulf leaders. This financial structure makes the entire project dependent on the political will and economic capacity of regional powers, creating a complex web of dependencies and introducing a new vector of geopolitical leverage. The plan’s authors project that the trust can generate some $185 billion in revenue within a decade, signaling that the primary motive is profit, not humanitarianism. This represents a fundamental shift in U.S. foreign policy in the region, moving from a model based on diplomacy and aid to one that is purely transactional and commercially driven. The stability of the region is now intrinsically linked to the project’s return on investment.

Regional reconstruction

The explicit framing of the post-conflict phase as the moment of the business, of the deal creates a clear, if hazardous, investment thesis. The sheer scale of the GREAT Trust, should it proceed, will generate enormous demand across multiple sectors. Obvious beneficiaries include:

Engineering, Procurement, and Construction (EPC) contractors: Global and regional firms with expertise in large-scale infrastructure will be essential. Companies like Bechtel, which has a long history of developing megaprojects in the Middle East including airports and industrial cities, are well-positioned. Other major players with a significant regional footprint include Mace Group, Egis, and numerous EPC contractors specializing in the energy and infrastructure sectors like NMDC Energy, UCC Holding, and Hyundai E&C.

Materials and heavy equipment: The removal of over 50 million tonnes of debris and the construction of new cities will require vast quantities of cement, steel, and heavy machinery. Companies like Caterpillar and Nesher Israel Cement Enterprises, which have been previously cited in the context of the region, are likely to see a surge in demand.

Technology and energy infrastructure: The plan’s focus on “smart cities,” data centers, and a new energy grid creates opportunities for technology providers, utility developers, and companies specializing in solar and gas infrastructure, particularly given the plan’s intention to develop the Gaza Marine gas field.

However, the investment landscape is fraught with peril. The ethical and political controversies surrounding the GREAT Trust create extreme Environmental, Social, and Governance (ESG) risks. Many companies potentially involved in the reconstruction have already been cited by organizations for profiting from the preceding conflict, including major defense, technology, and equipment manufacturers.

This dynamic will likely bifurcate the investment landscape. Mainstream institutional capital, bound by strict ESG mandates, may find it impossible to participate directly in the project. This could leave the field open to private equity firms, sovereign wealth funds, and family offices with a higher tolerance for reputational risk. For publicly traded companies involved, this could lead to a controversy premium on their stock prices, rewarding investors willing to overlook the significant ESG concerns but also exposing them to the risk of divestment campaigns and public backlash. Any investment in this theme must be highly selective, requiring deep due diligence and a clear-eyed assessment of the reputational and political risks involved.

While the accord creates a semblance of peace between Israel and its immediate neighbors, it does not neutralize the region’s primary destabilizing actor: Iran. Tehran’s exclusion from the diplomatic process, coupled with the continued enforcement of U.S. sanctions, leaves a major source of conflict unresolved. Throughout October 2025, senior Iranian officials have continued to issue threats to close the Strait of Hormuz, a critical chokepoint for global oil exports.

These threats are a direct response to the U.S. maximum pressure campaign and the enforcement of UN Security Council Resolution 1929, which allows for the inspection of Iranian vessels. An Iranian commander stated that the decision to close the Strait would depend on the pressure on Iranian exports. This threat represents a major, underappreciated tail risk to the global economy and the entire Middle East reconstruction narrative. An actual or attempted closure of the Strait would trigger an immediate spike in global energy prices, disrupt supply chains, and could easily shatter the fragile peace in the region. Such an event would render the Riviera de Gaza project instantly untenable and could plunge the global economy into a severe recession. For investors, the Iranian wildcard is a critical variable that must be continuously monitored, as it has the potential to override all other market drivers.

Inflation, Interest rates, and the erosion of wealth

While global attention is fixated on the geopolitical theater in the Middle East, a more insidious and far-reaching risk to investors is being deliberately obscured: the establishment of a persistent, structurally-driven inflationary environment in Western economies. The political spectacle serves as a convenient distraction from the reality that governments and central banks, faced with the choice between a painful recession and a gradual debasement of their currencies, have chosen the latter. This policy choice is creating a macroeconomic divergence globally and necessitates a fundamental rethinking of traditional portfolio construction.

Persistent inflationary environment

The dominant narrative being promoted is one of tranquility and a return to normalcy, suggesting that the threats of crisis, recession, or depression have been averted. However, this narrative masks the true cost of avoiding a downturn. The strategy employed by Western fiscal and monetary authorities is to continue stimulating their economies through deficit spending and liquidity injections—in effect, “printing money” to fund everything from defense expenditures to social programs. While this may support nominal economic growth and asset prices in the short term, its inescapable consequence is a sustained erosion of the purchasing power of fiat currency.

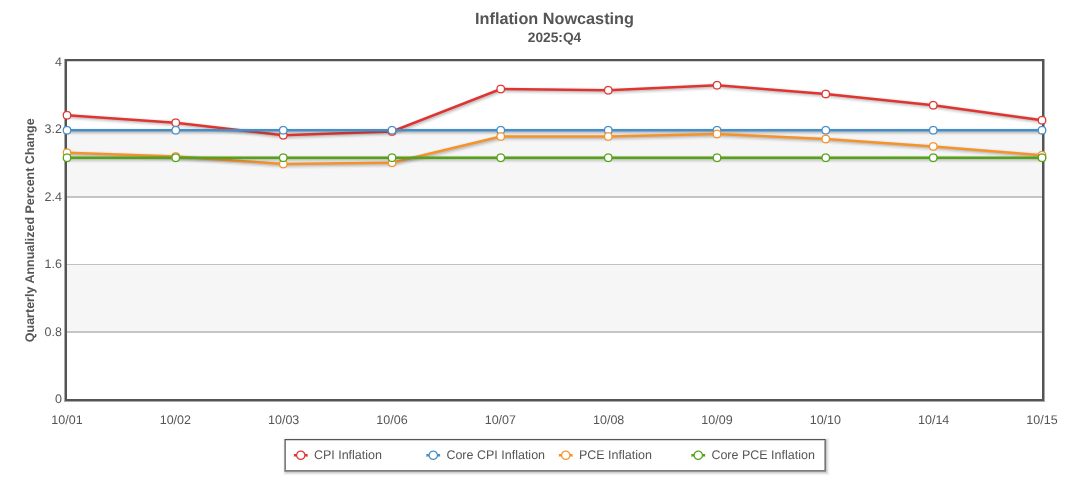

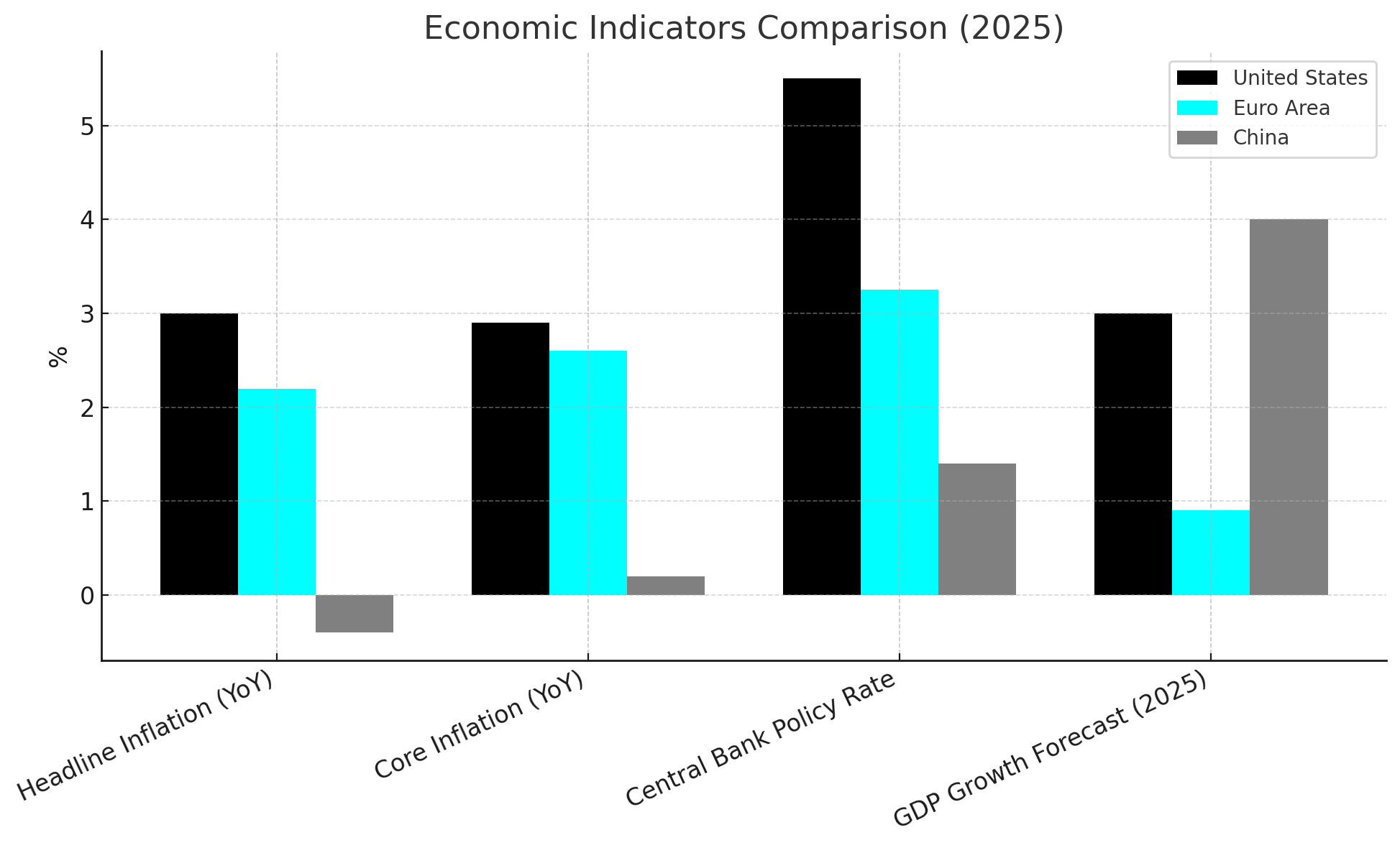

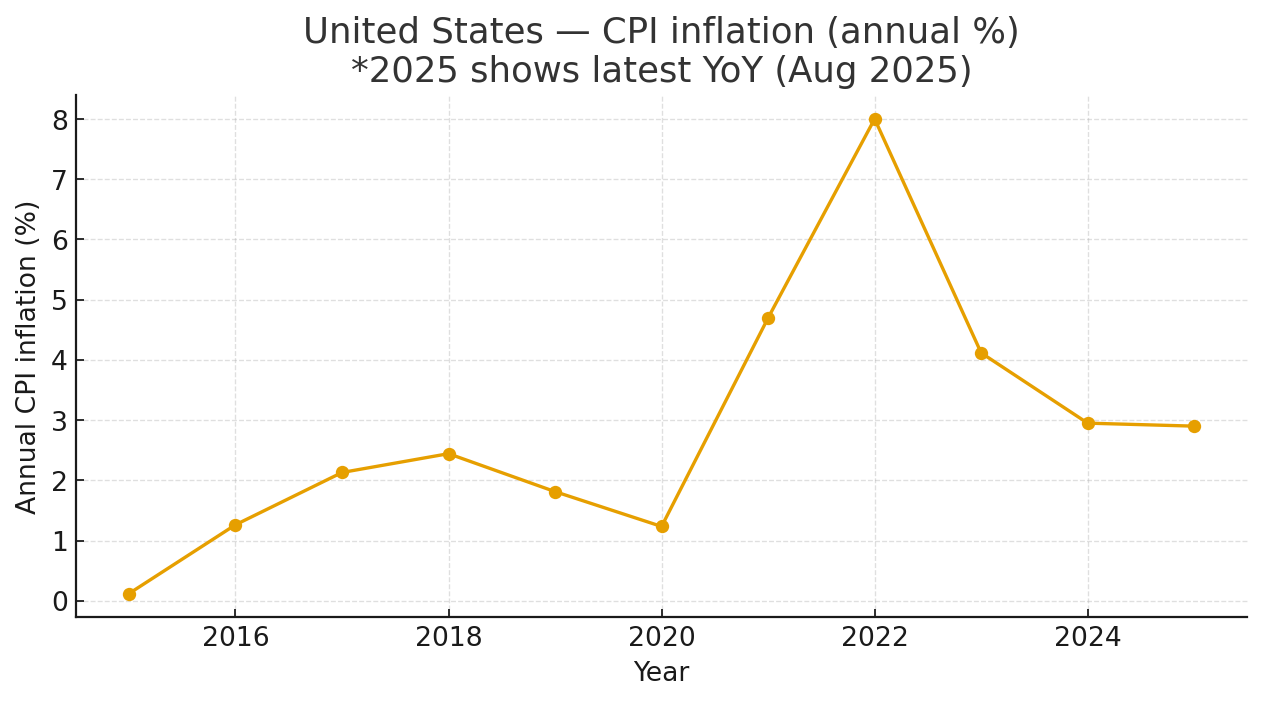

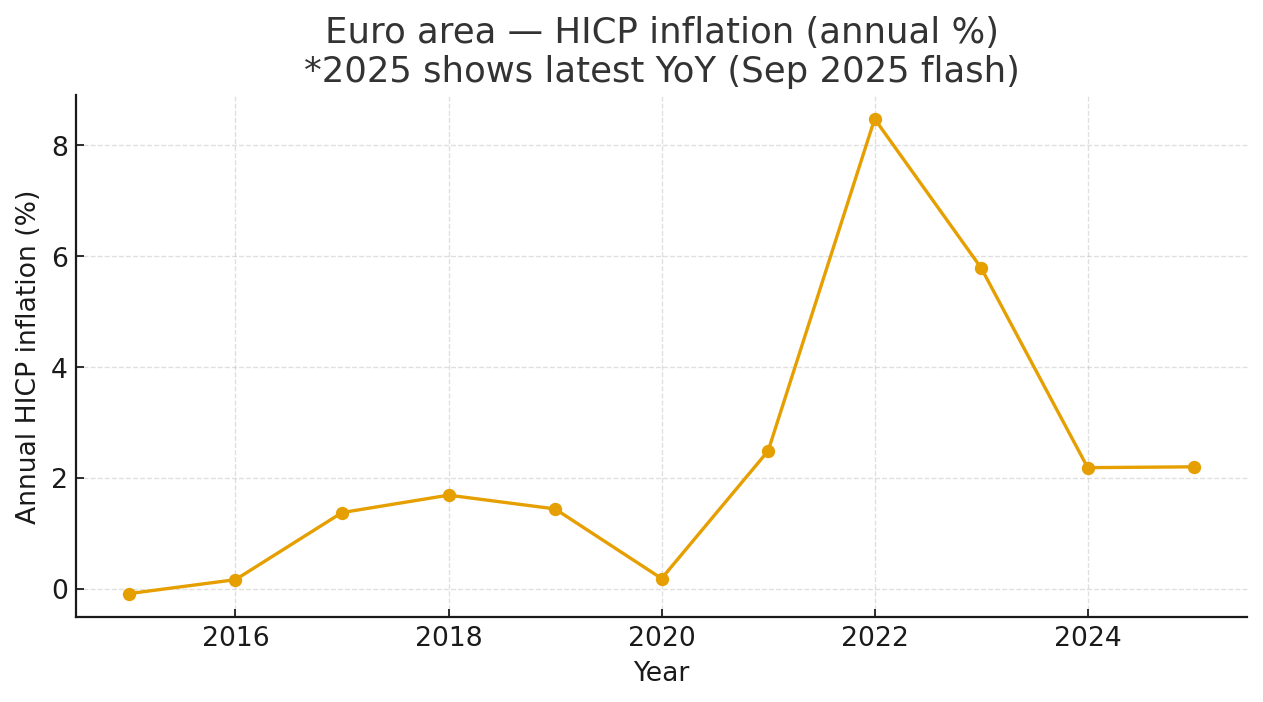

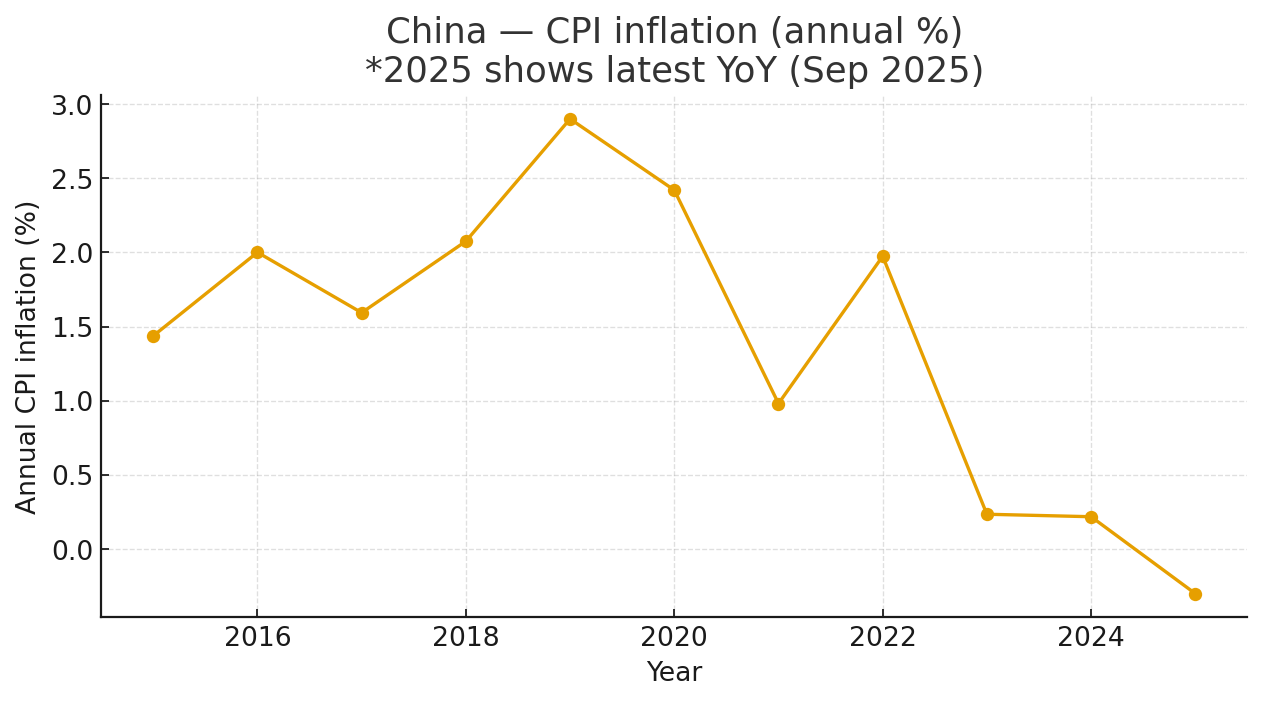

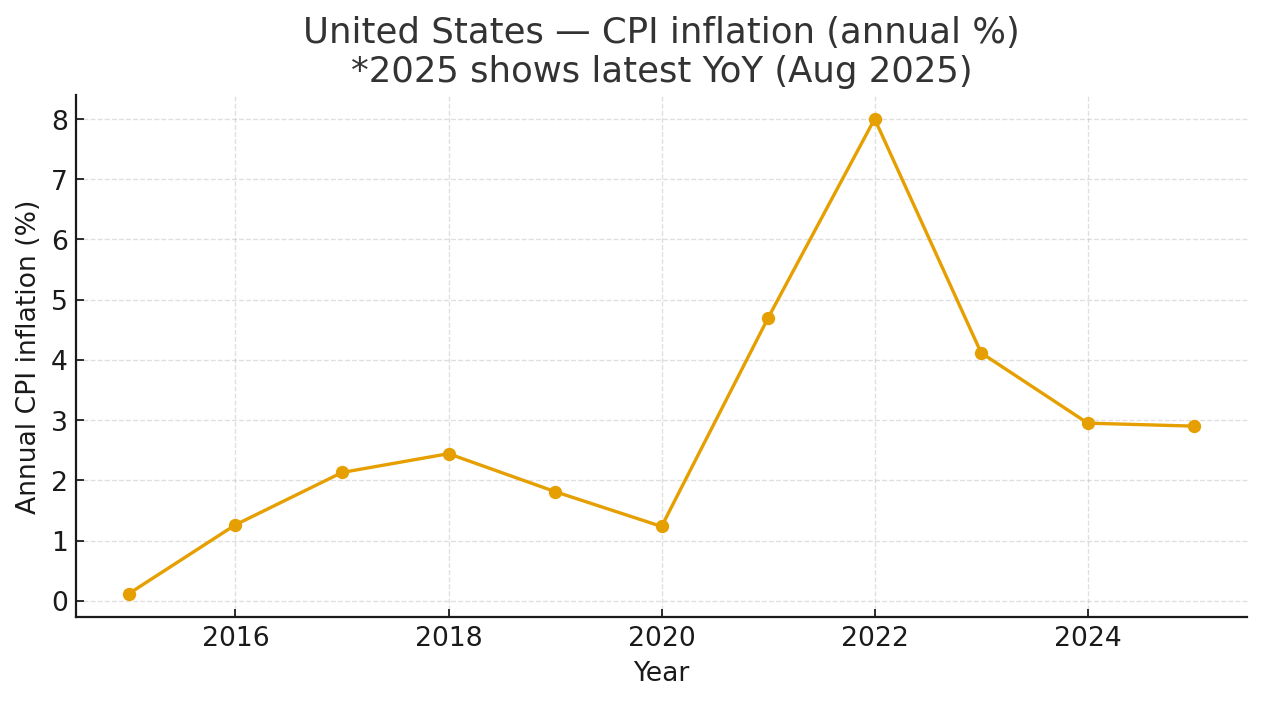

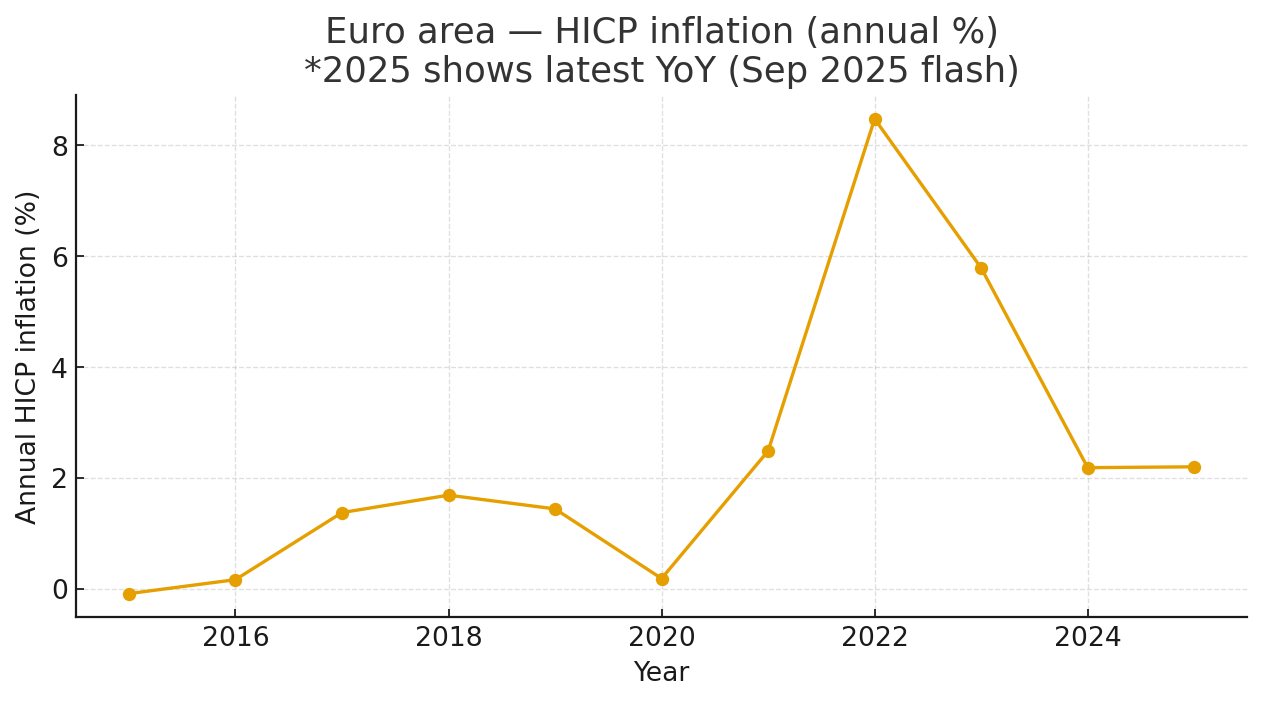

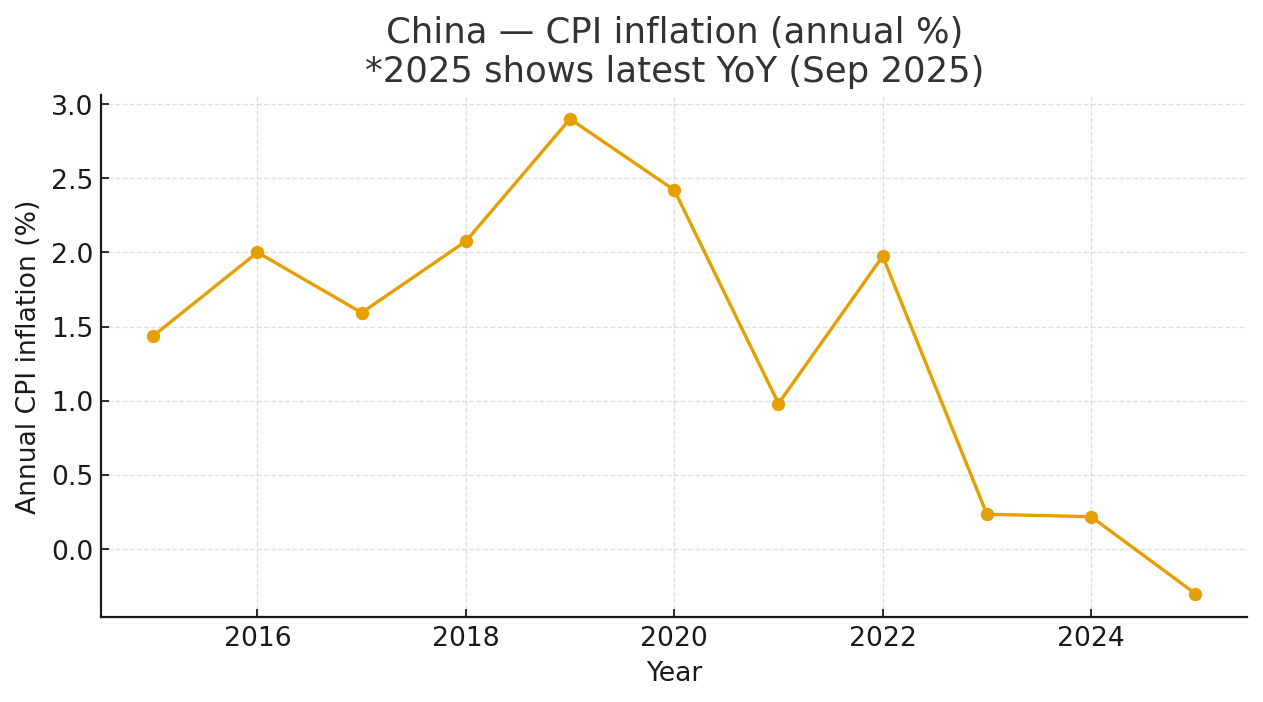

The data from October 2025 supports this thesis. In the United States, the Cleveland Fed’s Inflation Nowcasting model projects year-over-year CPI inflation at 3.00%, with core CPI at 2.93%. In the Eurozone, the Harmonised Index of Consumer Prices for September was 2.2%, with the more persistent services component running at 3.2%. While these figures are below the multi-decade highs seen previously, they remain stubbornly above the 2% target that central banks are mandated to maintain.

This inflationary pressure in the West stands in stark contrast to the situation in Asia. China is grappling with deflationary forces, with consumer prices forecast to fall by 0.1% year-over-year. This global macroeconomic divergence is a critical feature of the current landscape, creating different challenges and policy responses across major economic blocs. The analysis presented in the source material projects that the West is entering a new inflationary era, with an average annual inflation rate of around 3% becoming the norm for the next decade. This seemingly modest figure, when compounded, will have a devastating effect on real wealth, potentially destroying over a third of an individual’s purchasing power by 2035 if wages do not keep pace.

This table quantifies the divergence shaping global markets. The U.S. and Europe are battling persistent inflation with relatively high policy rates, yet their growth outlooks are modest. China, in contrast, faces deflation and is employing accommodative policy to stimulate a much higher rate of growth. This disparity is the primary driver behind the differing central bank policies and the strategic case for diversifying away from Western fiat currencies.

Mapping the policy paths of the Fed, ECB, and PBOC

The divergent macroeconomic realities are forcing the world’s major central banks onto different paths.

The U.S. Federal Reserve: The Fed is in a difficult position. While its stated goal remains 2% inflation, it faces mounting political pressure to cut interest rates, especially as the labor market shows signs of weakening and erratic trade policies weigh on growth. The central bank’s room for maneuver is becoming increasingly constrained, caught between an inflation rate that is still too high and a growth outlook that is losing steam. The market anticipates rate cuts, but the timing and magnitude are highly uncertain.

The European Central Bank (ECB): The ECB has already pivoted to a more dovish stance, having cut its key deposit rate to 3.25% in October 2025, with further cuts anticipated. This policy is a response to the floundering core Eurozone economies, particularly Germany, which is struggling with a loss of manufacturing competitiveness and faces a potential third consecutive year of contraction. While headline inflation has moderated, the ECB’s own staff project it will average 2.3% in 2025, still above target. The ECB is prioritizing growth over a strict inflation-fighting mandate.

The People’s Bank of China (PBOC): Facing deflationary pressures and a sluggish property sector, the PBOC is moving in the opposite direction. It is implementing a moderately loose monetary policy, utilizing a mix of general rate cuts and targeted support mechanisms to channel credit towards strategic sectors. The goal is not just short-term stabilization, but a long-term economic transition towards new quality productive forces such as advanced manufacturing, green technology, and digital finance.

This policy divergence will be a primary driver of global capital flows and currency exchange rates. The accommodative stances in the West, in an environment of persistent inflation, directly support the investment case for assets that can act as a store of value outside the traditional fiat system.

Strategic case for hard assets

The combination of persistent Western inflation, unsustainable fiscal deficits, and the use of the dollar-based financial system for geopolitical leverage (e.g., sanctions freezing Russia’s dollar-denominated assets) is accelerating a structural trend: de-dollarization. Central banks and institutional investors globally are increasingly seeking to diversify their reserves away from the U.S. dollar and into hard assets that cannot be arbitrarily devalued.

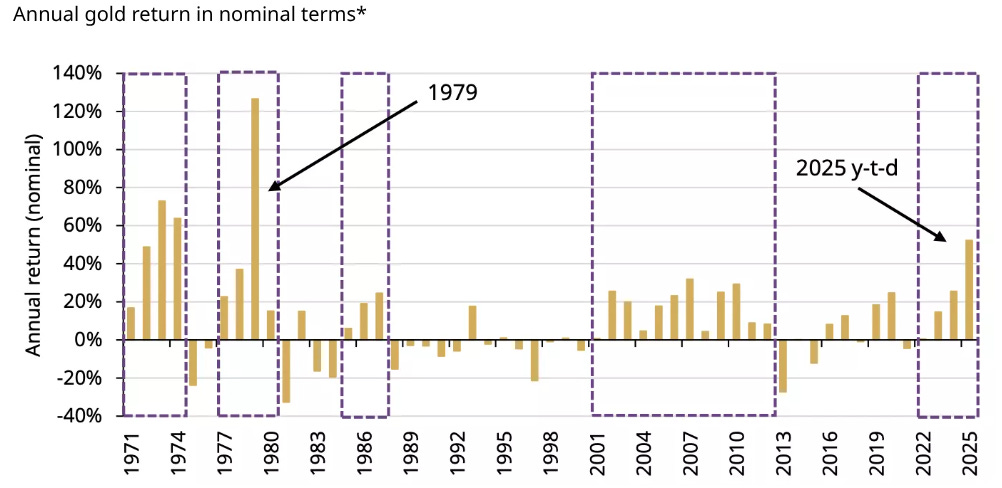

This trend is the primary force behind the historic rally in precious metals. In October 2025, gold surpassed the psychologically significant milestone of $4,000 per ounce, putting it on track for its best calendar year performance since 1979. This is not a speculative frenzy; it is a rational response to currency debasement. The rally is being driven by sustained buying from central banks, strong inflows into gold-backed ETFs, and investors seeking a safe haven from both inflation and geopolitical uncertainty. As one hedge fund manager noted, investors are beginning to see gold as a safer bet than the U.S. dollar, a concerning development for the long-term status of the greenback.