Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Why normal assumptions fail—and how real distributions give you real edge

You’ve used Gaussians as default—only to misprice volatility, underestimate tail risk, and overfit noise. The problem? Market behavior isn’t normal. And neither should your models be.

This chapter gives you the distributional toolkit real quants use to match models to markets.

What’s inside:

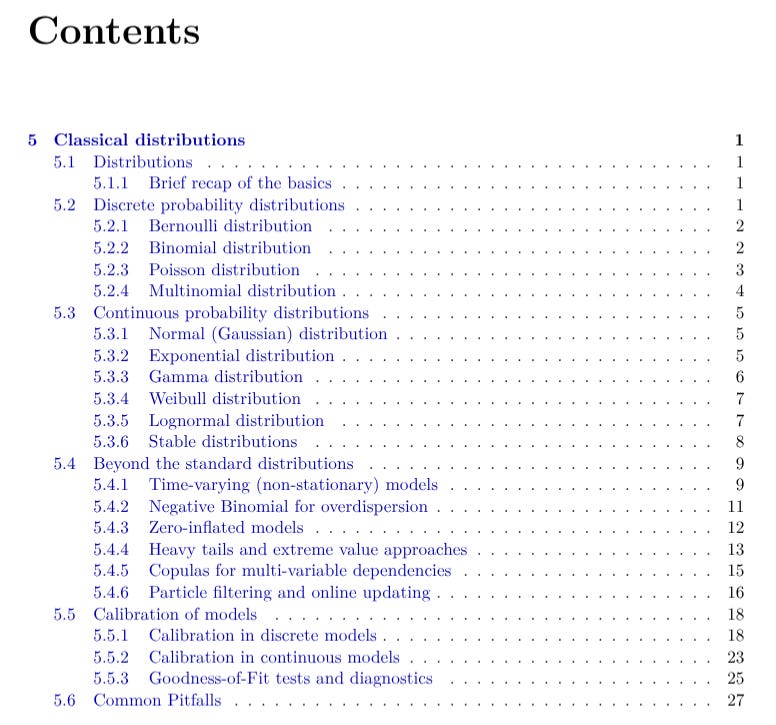

Discrete distributions decoded: Bernoulli, Binomial, and Poisson—modeled as real-time order arrivals, market states, and clustering effects in actual trading.

Beyond the bell curve: Exponential, Gamma, Weibull, Lognormal, and Stable distributions—each with tactical uses and Python simulations for trade sizes, timing, and volume.

Advanced adaptations: Zero-inflated models, Negative Binomial for overdispersion, and non-stationary intensity processes to model what markets actually do.

Heavy tails, real risks: Extreme value theory, Pareto exceedances, and GPD calibration for accurate drawdown and tail-event modeling.

Copula models: Move beyond linear correlation—capture nonlinear dependencies between market variables with bivariate simulations.

Real-time calibration: Maximum likelihood, method-of-moments, and particle filters for adaptive parameter estimation under live market data.

This isn’t textbook statistics. This is distributional survival for markets where the tails matter more than the center—and where fitting the right law can mean the difference between risk-managed and wrecked.