Table of contents:

Introduction.

Geopolitical landscape during Q4.

Engineering a Russian collapse.

The China confrontation.

Global fault lines.

Manufactured recession.

Intentional downturn or policy misstep?

Gauging economic resilience.

Portfolio allocation.

Fixed income.

Foreign exchange.

Commodities.

Equities.

Strategic outlook.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

Let's start with the new and aggressive foreign policy of the United States. This strategy represents a deliberate pivot towards geoeconomic warfare, with the explicit objective of collapsing the Russian economy to force a conclusion to the war in Ukraine and simultaneously containing the systemic challenge posed by China.

Check this report about Russia sanctions and exports control for going deeper:

This approach, centered on the unprecedented use of secondary sanctions and punitive tariffs, is the primary driver of global market volatility. The analysis contained in this report indicates that this policy is intentionally engineering a global stagflationary shock. This shock serves a dual purpose for the administration: achieving its stated foreign policy objectives while providing an external justification for a domestic economic downturn that was already signaled by weakening fundamental data.

The primary risk emanating from this strategy is a severe, synchronized global recession. This downturn will be exacerbated by inevitable retaliatory measures, the fragmentation of global supply chains, and heightened geopolitical instability across multiple theaters, from political crises in Europe to simmering conflicts in the Middle East.

A secondary, but perhaps more important, long-term risk is the structural degradation of the US-centric global financial system. This is evidenced by two paradoxical concerning market phenomena:

A sharp sell-off in U.S. Treasury bonds during a risk-off event, calling their safe-haven status into question.

And the accelerated de-dollarization efforts being coordinated by the BRICS bloc, which now represents a significant portion of the global economy.

As anticipated in previous reports, the current environment necessitates a re-allocation of investment portfolios away from strategies that thrived during the era of globalization. A significant overweight position in physical gold and gold-related equities is recommended as the premier safe-haven asset in an environment where sovereign debt is no longer risk-free. A defensive posture in equities is critical, favoring sectors that benefit directly from geopolitical conflict, such as defense and cybersecurity, while aggressively underweighting sectors at the epicenter of the trade war, namely technology and consumer discretionary. Fixed income strategy must pivot away from a reliance on traditional safe sovereign debt, which is now a source of risk, toward high-quality corporate credit and inflation-protected securities. A structurally bearish stance on the U.S. Dollar is maintained, with a preference for the Swiss Franc as the primary currency haven and a tactical view on the Japanese Yen during periods of acute market stress.

As you already know, we are facing these geopolitical risks:

Geopolitical landscape during Q4

The current market environment is not defined by traditional economic cycles but by a series of deliberate, high-stakes geopolitical maneuvers. The strategic framework of the new U.S. policy, assesses its viability by examining the required international cooperation, and maps the compounding risks from other global flashpoints that threaten to amplify the primary conflict.

Engineering a Russian collapse

The centerpiece of the new U.S. global strategy is a maximalist approach to the conflict in Ukraine. The Trump administration, through public statements by Treasury Secretary Scott Bessent, has explicitly articulated its objective is to collapse the Russian economy. This language marks a significant escalation from previous sanctions regimes, which were designed to degrade, isolate, or punish Russia's economic capacity but stopped short of seeking its outright destruction. The current policy is an act of total economic warfare.

This aggressive posture is framed as a final diplomatic off-ramp. President Trump has reportedly offered Russian President Vladimir Putin a last chance for a peace deal before initiating what is being called a second, more severe phase of sanctions . This framing is a crucial diplomatic maneuver, designed to position any subsequent economic warfare as a direct consequence of Russian intransigence. It provides a narrative intended to galvanize allied support by portraying the U.S. actions not as an escalation, but as a necessary response to a diplomatic failure.

The entire strategy, however, is built upon a critical and increasingly fragile foundation: the full cooperation of European allies. The administration is actively pressuring the European Union to join in imposing a full-spectrum regime of secondary sanctions, targeting any country or entity that continues to import Russian oil. Yet, this call for unity comes at a time of profound European division and weakness. Nations such as Hungary and Slovakia remain heavily dependent on Russian energy and are expected to resist measures that would cripple their economies. Furthermore, the moral high ground is undermined by the fact that several EU states continue to import Russian liquefied natural gas, revealing deep contradictions in the bloc's energy policy.

This pre-existing fragility has been compounded by a full-blown political crisis in France, a core pillar of the European Union. The French government, led by Prime Minister François Bayrou, has collapsed after losing a no-confidence vote. The crisis was triggered by Bayrou's attempt to pass a deeply unpopular budget that included €44 billion in savings to tackle France's spiraling public debt, which now stands at a staggering 114% of GDP. A France preoccupied with domestic political paralysis, searching for its fourth prime minister in a year, and forced to impose painful austerity on its populace is an unreliable and politically incapacitated partner for a high-risk economic war that would inevitably inflict further economic pain on its citizens. This internal chaos critically weakens the EU's ability to formulate and execute the kind of cohesive, aggressive economic policy that the U.S. gambit demands.

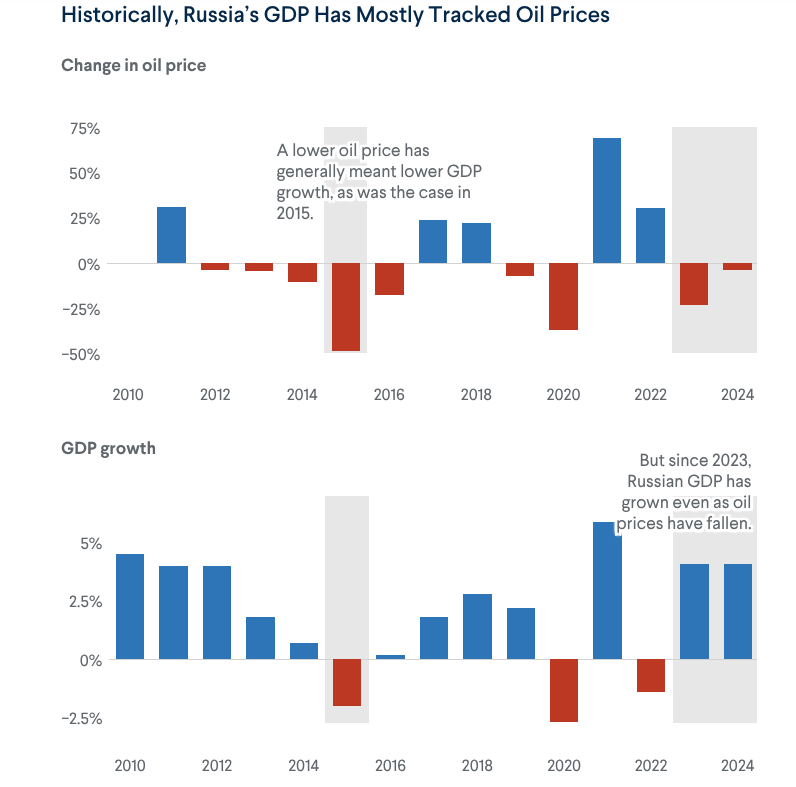

While the U.S. focuses on its economic offensive, Russia is not a passive target. Its responses are likely to be asymmetric and unpredictable. Former Russian President Dmitry Medvedev's recent threats of annihilation against Finland, a NATO member, demonstrate a clear willingness to escalate military tensions directly along the alliance's borders. Economically, Russia has proven its ability to adapt to sanctions by reorienting trade towards Asia and utilizing a shadow fleet of unregistered vessels to transport its oil, indicating a degree of resilience that may frustrate U.S. objectives.

The American strategy is therefore predicated on a foundational flaw. It requires unified and unwavering European support at the very moment a key European power is politically disintegrating over the fiscal pressures that would be exacerbated by such a conflict. The political instability in France is not a separate issue; it is a direct and critical vulnerability in the U.S. geoeconomic plan. Furthermore, the U.S. is betting that it can control the ladder of economic escalation. This is a dangerous assumption. Faced with an existential economic threat aimed at total collapse, Russia is far more likely to escalate in domains where it perceives an advantage. This could include hybrid warfare, large-scale cyber-attacks against Western critical infrastructure, or direct military provocations against NATO's periphery. This creates a perilous mismatch: the United States is fighting an economic war, but Russia may choose to respond on a military chessboard, risking an unintended and potentially catastrophic conflict.

The China confrontation

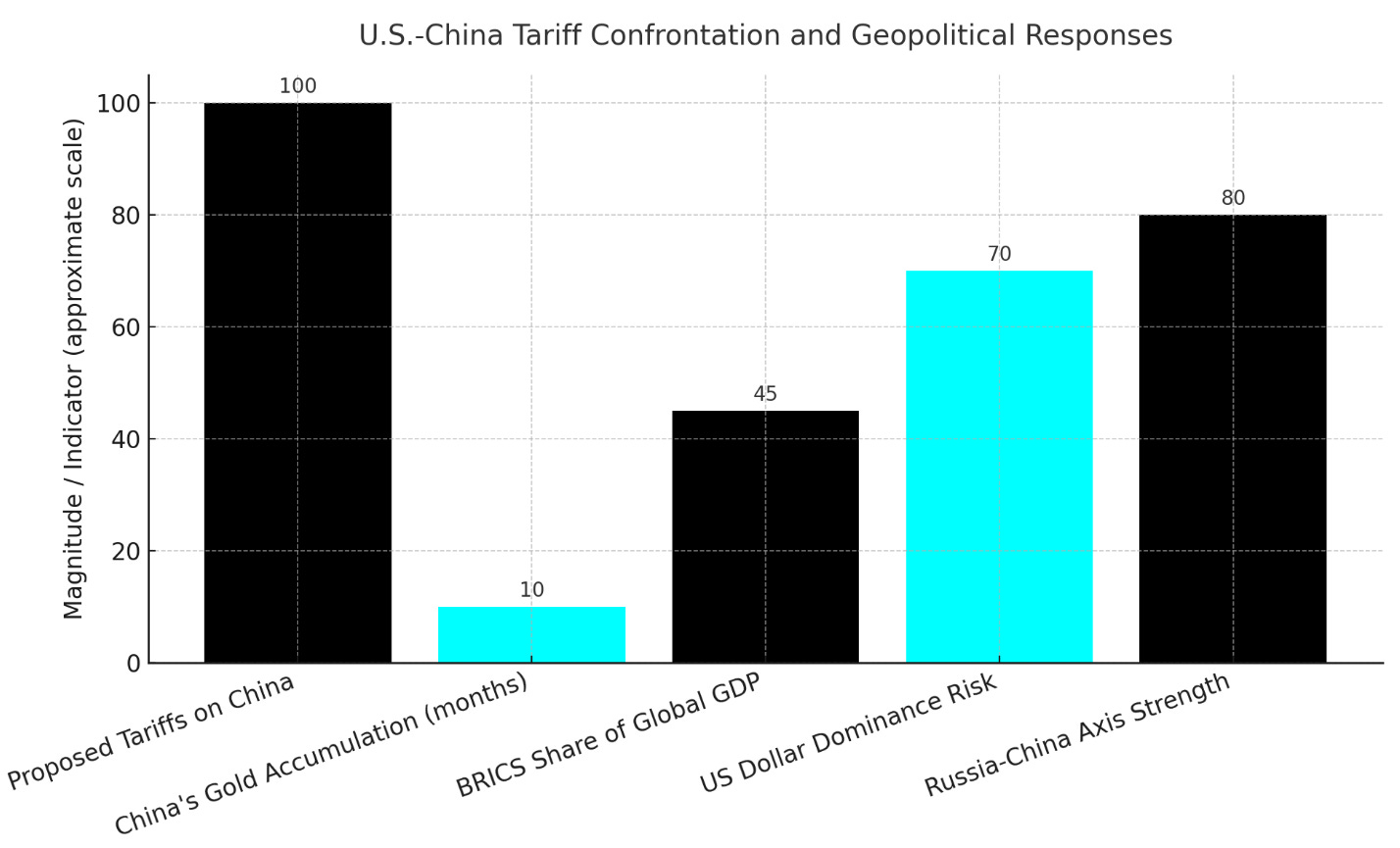

The primary weapon in the U.S. arsenal for collapsing Russia's economy is the imposition of secondary tariffs on countries that purchase Russian oil. As the principal buyer of Russian crude, China is the principal target of this policy. The proposed tariffs are not merely punitive; they are designed to be prohibitive. Reports indicate potential tariff levels as high as 100%, a figure that goes far beyond the measures seen in the previous U.S.-China trade war. This action is intended to force Beijing into an impossible choice: abandon its strategic energy partner or lose access to Western consumer markets. In effect, this policy reignites the U.S.-China trade war on an unprecedented and far more dangerous scale.

China, however, is not waiting passively for the impact. It has been actively preparing for such a confrontation. Beijing is reportedly helping Russian energy giants raise necessary funds and has been systematically increasing its central bank's gold holdings, with the People's Bank of China adding to its reserves for ten consecutive months. This is a clear and deliberate strategy to build a financial shield against sanctions and dollar dependency, reducing its vulnerability to the very economic coercion the U.S. now seeks to apply.

This confrontation is not merely bilateral. It has catalyzed a broader geopolitical realignment. The BRICS nations—an expanded bloc now including Brazil, Russia, India, China, South Africa, Egypt, Indonesia, Iran, the UAE, and Ethiopia, and representing over 45% of global GDP—are holding an emergency summit to formulate a coordinated response. In a display of unity, leaders from the bloc's core non-Western economies have publicly denounced the U.S. actions. Brazil's President Lula da Silva has labeled the policy tariff blackmail, while China's Xi Jinping has condemned the trade wars and tariff wars. In a more direct challenge, Iran has explicitly proposed the creation of a formal BRICS mechanism to jointly counter U.S. sanctions.

The use of secondary sanctions and punitive tariffs against an economy of China's scale and systemic importance represents a strategic miscalculation that will likely cause permanent damage to the U.S. dollar's global dominance. Secondary sanctions derive their impact from the centrality of the U.S. dollar and the indispensable nature of the U.S. financial system; access to this system is the stick used to enforce compliance. By targeting not just a rogue state but major pillars of the global economy like China and India, the U.S. is compelling the world's largest non-Western economies to build and adopt alternative systems as a matter of national security and self-preservation. The emergency BRICS summit, the calls for a joint anti-sanction mechanism, and China's massive gold accumulation are not merely reactive, defensive measures; they represent the accelerated construction of a parallel financial architecture designed to operate outside of U.S. control. In its attempt to win a short-term economic battle against Russia, the U.S. is catalyzing a long-term strategic defeat: the erosion of the very financial hegemony that gives its sanctions their power.