[INTEL REPORT] Tariff-driven inflation and policy divergence

Unpacking corporate margins, buyback-fueled market strength, and the global rotation beyond U.S. leadership

Table of contents:

Introduction.

Corporate margins, consumer prices, and trade policy.

Corporate entities under pressure.

The Inflationary ripple effect.

U.S. market performance.

Fueling EPS and market indices.

Domestic sector performance and allocation shifts.

Insider activity and market sentiment.

Global market opportunities.

Europe's renewed momentum.

Asia's emerging strengths.

Central bank actions and key indicators.

The ECB's dovish turn.

The Federal Reserve's steady hand.

Positioning for future growth and risk mitigation.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

Market dynamics over the past week displayed intricate interactions, necessitating careful quantitative interpretation. U.S. equities maintained bullish momentum, notably among large-cap and tech-driven sectors. However, the primary mechanism underpinning this bullishness has been aggressive corporate share buybacks, driving EPS higher through reduced outstanding share counts rather than organic revenue growth. Concurrently, the escalating tariff environment continues exerting measurable pressure on corporate profitability, manifesting distinctly as consumer-driven inflation. Internationally, quantitative indicators point to a rotation in investor sentiment: markets in Europe and specific Asian regions are experiencing renewed capital inflows, signaling diminishing relative outperformance of U.S. equities.

From a macroeconomic modeling standpoint, central bank divergence introduces additional complexity. The ECB’s continued accommodative posture through rate cuts contrasts markedly with the Federal Reserve's cautious, data-responsive stance, particularly sensitive to employment metrics and tariff policy uncertainties. These divergent monetary policies underpin a sustained global liquidity environment, as quantitatively evidenced by the concurrent rally in speculative assets like Bitcoin, a proxy indicator for systemic risk appetite and liquidity conditions.

For quantitatively-driven investors, several critical implications emerge. Portfolio diversification beyond domestic assets warrants increased priority, given robust momentum signals emanating from international markets. Simultaneously, tariff-induced inflation pressures necessitate quant-based hedging strategies aimed at preserving purchasing power and portfolio stability. Moreover, investors should quantitatively analyze global central bank policy trajectories to accurately forecast potential shifts in cross-border capital flows and associated market volatility. With the impending release of U.S. non-farm payrolls data, statistical models currently indicate stability, suggesting an opportune interval for recalibration of portfolio allocations.

Examining market fundamentals through a quantitative lens further clarifies underlying concerns. The sustained U.S. equity rally largely reflects corporate financial engineering strategies rather than substantive economic expansion. Record-level stock repurchases effectively inflate EPS metrics, a statistical artifact of share-count reduction rather than genuine operational improvements. This financial engineering phenomenon occurs amidst contractionary GDP signals for Q1 2025, largely attributable to pre-tariff import surges and escalating trade uncertainties. Quantitative analysis of capital expenditures reveals caution among firms, prioritizing short-term buybacks over long-term productive investments, indicative of tempered growth expectations.

Consequently, investors must carefully dissect headline EPS growth, distinguishing genuine earnings improvements from mechanical share reductions. A market excessively reliant on financial engineering, absent robust underlying economic fundamentals, risks statistical instability should growth momentum falter or corporate appetite for share repurchases diminish. Therefore, quantitative assessments remain essential to ascertain whether observed equity market performance genuinely reflects sustainable operational growth or merely transient financial structuring.

Corporate margins, consumer prices, and trade policy

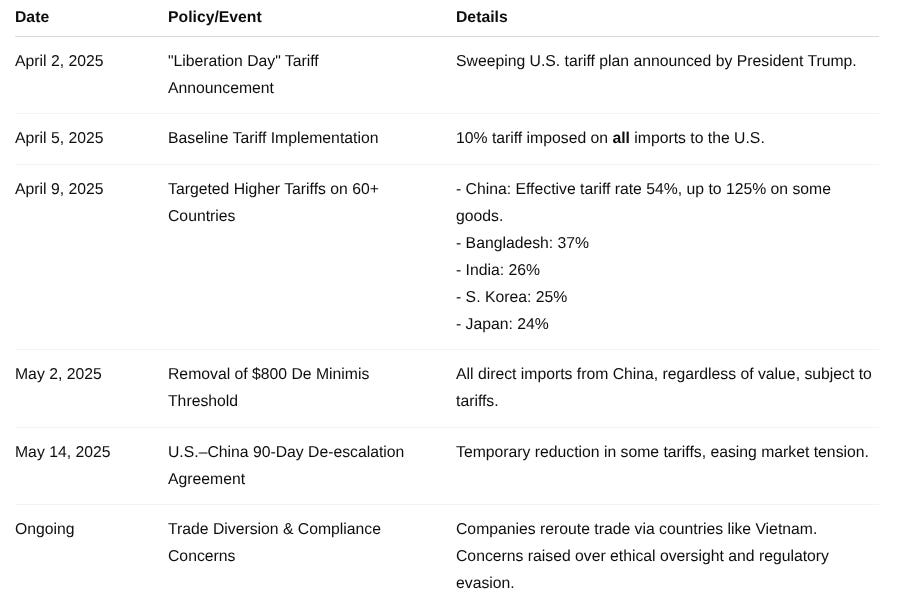

The global trade landscape continues to be defined by escalating tariffs, particularly following the U.S. administration's recent actions. On April 2, 2025, a significant policy shift occurred, dubbed Liberation Day by President Trump, as sweeping new tariffs were enacted. This initiative imposed a baseline 10% tariff on all imports to the U.S., effective April 5, 2025, with even higher tariffs targeting approximately 60 additional countries, effective April 9, 2025. China faced the most substantial increases, with an effective tariff rate soaring to 54% after April 9, building upon existing levies, culminating in an overall rate of 125% on certain Chinese goods. Other nations, including Bangladesh (37%), India (26%), South Korea (25%), and Japan (24%), also saw considerable tariff hikes. A notable procedural change was the elimination of the $800 de minimis threshold for duty-free imports from China on May 2, 2025, effectively making small direct consumer purchases economically unfeasible.

The initial announcement of these extensive global tariff policies triggered an immediate global stock market crash, underscoring the market's sensitivity to heightened trade tensions. However, a subsequent 90-day de-escalation agreement between the U.S. and China, effective May 14, temporarily reduced some of these heightened tariffs, contributing to a more positive market sentiment in May.

Corporate entities under pressure

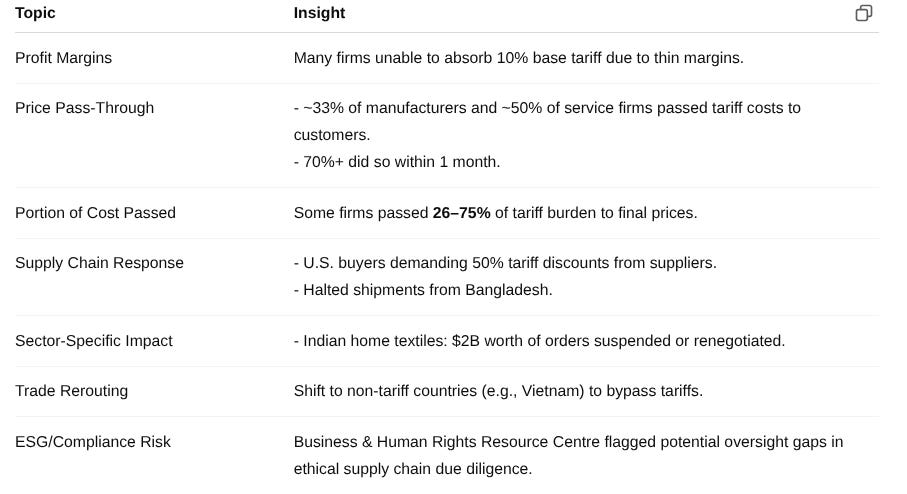

The impact of these tariffs on corporate entities has been immediate. Many companies, especially those with limited financial strength or thin profit margins, are finding it difficult to absorb the base 10% tariff. Evidence strongly indicates that companies are rapidly passing these increased costs onto consumers.

Nearly one in three manufacturers and almost half of service companies have already transferred tariff costs to their end products. A smaller, yet significant, segment of businesses has passed on an even larger portion—between 26% and 75%—of the tariff burden to their final prices. The speed of this pass-through is striking, with more than 70% of companies raising prices within a month or less, effectively disproving the initial expectation that businesses would simply absorb these additional costs due to their insufficient margins.

This pressure extends globally, impacting supply chains far beyond U.S. borders. Reports indicate that U.S. buyers are aggressively demanding price reductions, sometimes as much as half the tariff cost, from Chinese suppliers, leading to delays in orders and business losses for these manufacturers. Similar pressures, including halted shipments and demands for discounts, have been reported in Bangladesh, and India's home textiles industry has been particularly hard hit, with orders worth at least $2 billion reportedly subject to renegotiation or suspension.

This situation points to a significant consequence: a forced, and potentially rapid, restructuring of global supply chains. Companies are not merely absorbing tariffs; they are actively seeking to mitigate them through aggressive supplier negotiations or by rerouting trade through non-tariffed countries. For instance, the Commerce Secretary's statement that "Vietnam's Just a Pathway of China" to the U.S. suggests a strategic effort to divert trade. This trade diversion, while offering a temporary reprieve for some businesses, introduces increased complexity and potential ethical concerns, as evidenced by the Business & Human Rights Resource Centre's unanswered outreach to fashion brands regarding human rights due diligence amidst supply chain shifts.

Investors should therefore analyze the supply chain resilience and adaptability of companies in their portfolios, recognizing that those with diversified sourcing and strong negotiating power may navigate this environment more effectively.

The Inflationary effect

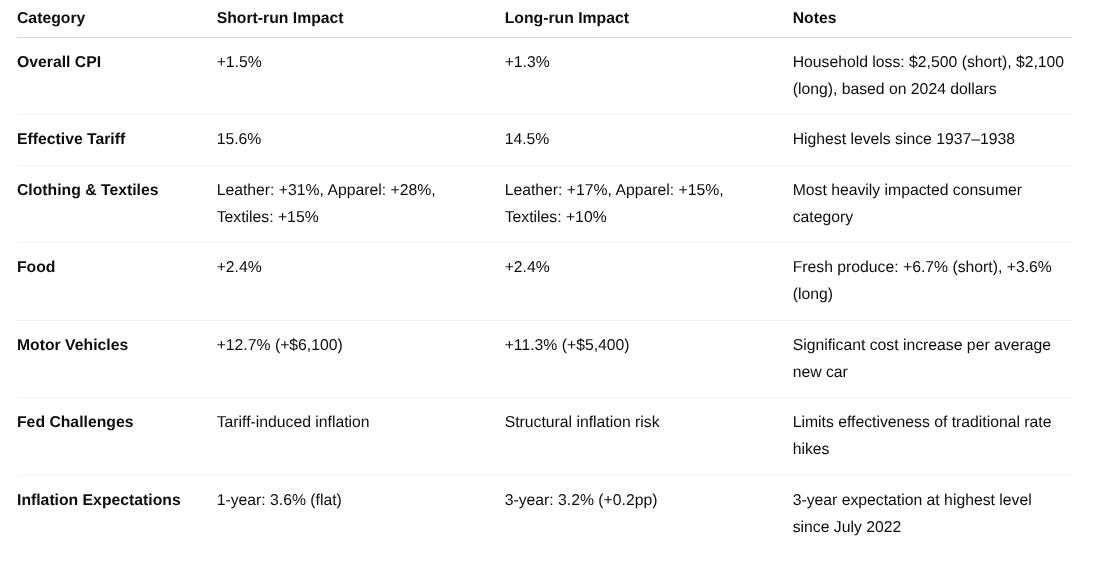

The swift pass-through of tariff costs is translating into what has been termed express inflation, posing a considerable challenge for Fed Chair Jerome Powell and the Federal Reserve as they endeavor to maintain stable interest rates. The Congressional Budget Office estimates that the tariffs implemented between January 6 and May 13, 2025, will lead to an average annual inflation increase of 0.4 percentage points in 2025 and 2026, culminating in a 0.9% higher price index by 2026.

As of June 1, 2025, the overall average effective U.S. tariff rate faced by consumers stands at 15.6%, the highest observed since 1937. This is projected to cause a 1.5% rise in the overall price level in the short-run, equivalent to an average per household consumer loss of $2,500 in 2024 dollars. Even after consumption shifts, the average tariff rate is estimated to remain at 14.5%, the highest since 1938, resulting in a long-run price increase of 1.3% and a $2,100 loss per household.

Specific consumer categories are disproportionately affected by these tariff-induced price increases:

Prices for leather products—including shoes and handbags—are expected to surge by 31% in the short-run, remaining 17% higher in the long-run. Apparel prices are projected to rise by 28% in the short-run, settling at 15% higher in the long-run, while textiles could see a 15% increase in the short-run, remaining 10% higher in the long-run.

Anticipated to rise by 2.4% in both the short and long-run. Fresh produce is initially 6.7% more expensive, stabilizing at 3.6% higher over time.

Projected to increase by 12.7% in the short-run and 11.3% in the long-run, translating to an estimated additional cost of $6,100 for an average new car in the short-run and 5,400inthelong−run.

Median inflation expectations for April 2025 were mixed, with the one-year-ahead horizon remaining unchanged at 3.6%, while the three-year-ahead horizon increased by 0.2 percentage points to 3.2%, reaching its highest reading since July 2022.

This situation creates a complex policy bind for the Federal Reserve. The Fed's dual mandate includes both full employment and price stability—a 2% inflation target:

If inflation is primarily being driven by supply-side shocks, such as tariffs, rather than excessive demand, conventional monetary tightening—raising interest rates—might not be the most effective tool and could inadvertently stifle economic growth.

Conversely, if the Fed prioritizes supporting the labor market by holding or cutting rates, it risks allowing this tariff-induced inflation to become entrenched, potentially pushing inflation sustainably above its 2% target.

This suggests that the Fed's decision-making process will be unusually challenging, potentially leading to a prolonged period where inflation remains higher than desired, or a more aggressive tightening cycle if tariff impacts persist and broaden. Investors should closely monitor inflation data and consider assets that historically perform well in inflationary environments, as the current environment presents unique challenges for monetary policy.

U.S. market performance

U.S. equity markets demonstrated robust performance in May 2025, with major indices recording significant gains. The S&P 500 rose by 6.15% to 6.3%, the Nasdaq Composite surged by 9.56% to 9.7%, and the Dow Jones Industrial Average advanced by 3.94% to 4.2%. Small-cap stocks, as represented by the Russell 2000, also saw substantial increases of 5.2% to 5.3%. This strong momentum was evident in early May, when the S&P 500 achieved a 9-day winning streak, its longest in two decades.