[INTEL REPORT] Strategic allocation amid China’s energy dominance

Energy hegemony, policy volatility, and market concentration in the 2025–2026

Table of contents:

Introduction.

The new energy order.

China's solar hegemony.

A leap towards energy independence.

Raw material crisis.

U.S. volatility and european instability.

The Federal Reserve under siege.

Europe's political fault line.

Market structure, concentration and conflict.

The magnificent seven.

Musk's lawsuit as a potential catalyst for de-concentration.

Investment thesis.

Strategic allocation and tactical recommendations for 2025-2026.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

The post-2008 era of synchronized global growth, disinflation, and deepening economic integration is definitively over. Investors are now confronted with a new, more challenging regime characterized by intensifying geopolitical competition, policy-driven volatility, and a profound divergence between the performance of financial assets and the health of the real economy. The central challenge for capital allocation in 2025 and 2026 is no longer the simple identification of growth, but a more nuanced understanding of its quality, resilience, and geopolitical context. The global landscape is fracturing along distinct fault lines, creating a "cocktail" of risks that demands a strategic pivot away from passive, broad-market approaches.

This report posits that three primary arenas of conflict and opportunity will define the investment environment:

First, the global energy transition has become a key battleground for strategic dominance. China is not merely a participant; it is systematically securing the entire green-technology supply chain, from the extraction of raw materials to the development of next-generation nuclear power. This strategy has created acute and underappreciated vulnerabilities for Western economies, whose green ambitions are now contingent on their primary geopolitical competitor.

Check more about this here:

Second, the global economy is increasingly subject to policy-induced volatility. The long-held principle of central bank independence is under direct political assault, most notably in the United States, creating uncertainty around the future path of monetary policy and inflation. Simultaneously, political fragmentation in Europe, starkly illustrated by the ongoing crisis in France, threatens to paralyze necessary fiscal reforms, amplifying sovereign risk and casting a pall over the continent's growth prospects. These policy risks are now a primary driver of market behavior, often overriding traditional economic signals.

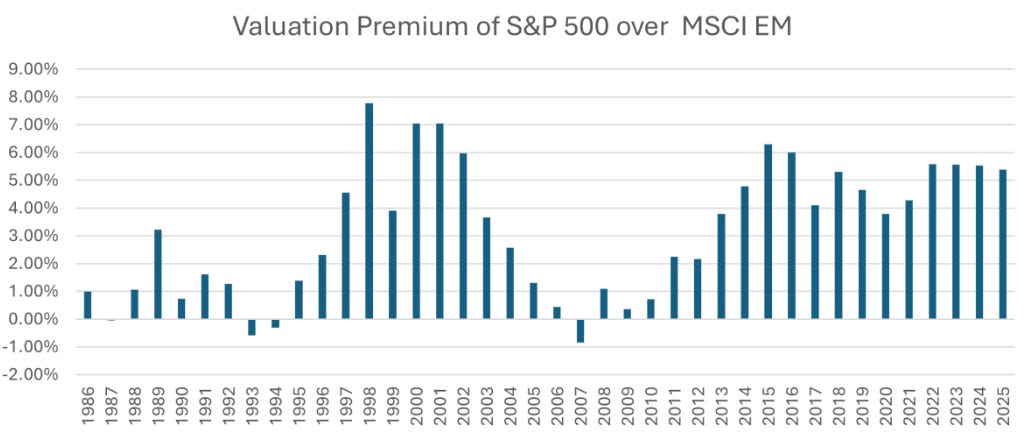

Third, the financial performance of large, multinational corporations and the valuation of their equity have decoupled from the economic reality experienced by the domestic middle class. This fracture is evident in the contrast between soaring U.S. corporate profits and the stagnant earnings of firms in Europe and emerging markets since the financial crisis.

The primary recommendation is a decisive shift in investment strategy. Passive exposure to market-cap-weighted indices is no longer a prudent path to diversification; it has become a concentrated bet fraught with geopolitical and structural risk. The path forward requires a more active, thematic, and quality-focused approach.

The new energy order

The global energy transition is frequently portrayed as a collaborative, multilateral effort to combat climate change. This perspective is dangerously naive. It is, first and foremost, a geopolitical chessboard upon which a new global hierarchy is being established. In this contest, China has moved decisively to establish a commanding, and in some areas hegemonic, position. This ascendancy is not accidental; it is the result of a long-term, state-directed industrial strategy that has outmaneuvered the West. For investors, understanding the dynamics of this new energy order is critical to identifying both the profound risks embedded in the current system and the durable opportunities that will arise as the West begins to formulate a strategic response.

China's solar hegemony

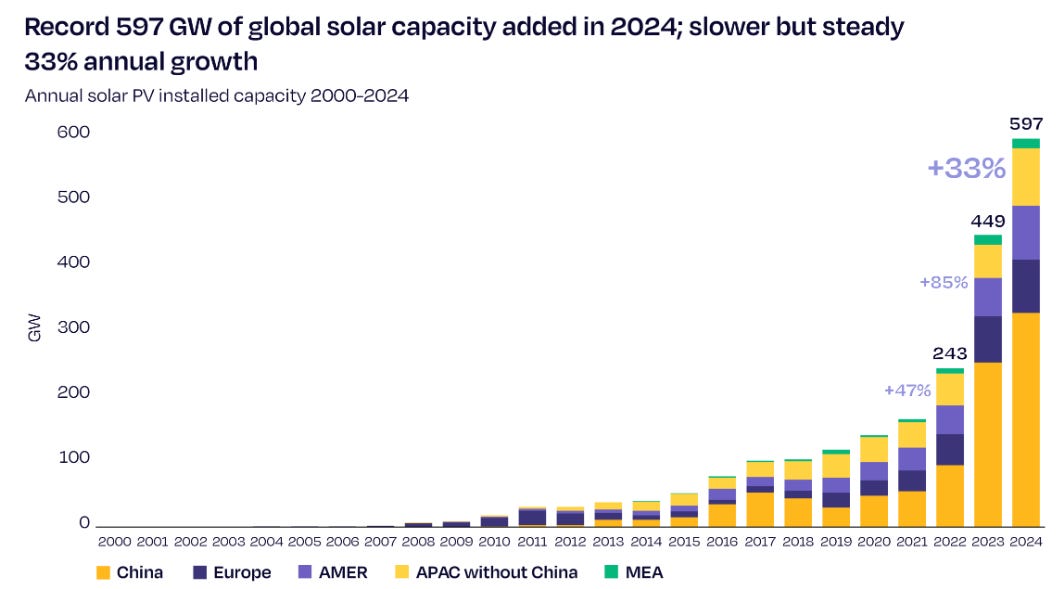

China's dominance in the solar industry is not merely a matter of manufacturing scale; it is a comprehensive, full-spectrum control over the entire global supply chain. The sheer scale of its domestic deployment is staggering. In 2024, China installed an unprecedented 329 GW of solar capacity, accounting for 55% of the global market and exceeding the combined total of the other top 10 markets. This momentum has accelerated into 2025, with a record 212 GW of new capacity added in the first half of the year alone, more than double the amount installed in the same period of 2024. This explosive growth has had a tangible impact on the country's energy mix, with wind and solar collectively generating a record 26% of China's electricity in April 2025. Projections indicate that the country's cumulative installed solar capacity will reach a stunning 900 GW by the end of 2025, solidifying its position as the world's undisputed solar superpower.

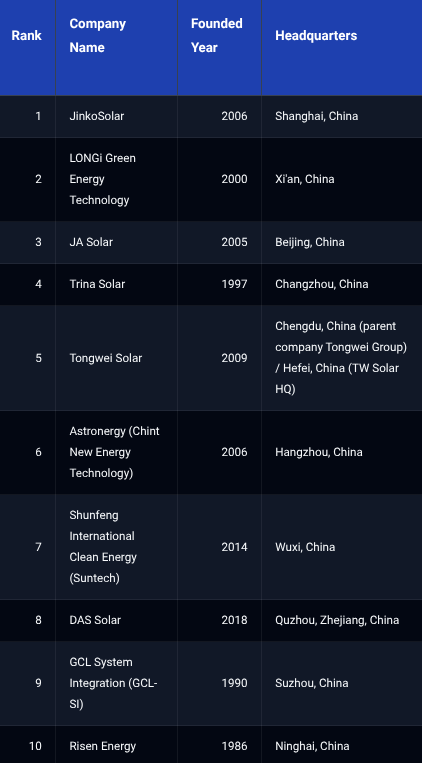

This domestic build-out provides the foundation for its global export strategy, which is led by a handful of corporate giants. Companies such as JinkoSolar, LONGi Green Energy Technology, JA Solar, and Trina Solar are the dominant forces in the global market, consistently leading module shipment rankings. However, a closer examination of recent trade data reveals a masterful strategic pivot that has profound implications for global supply chains and Western energy security.

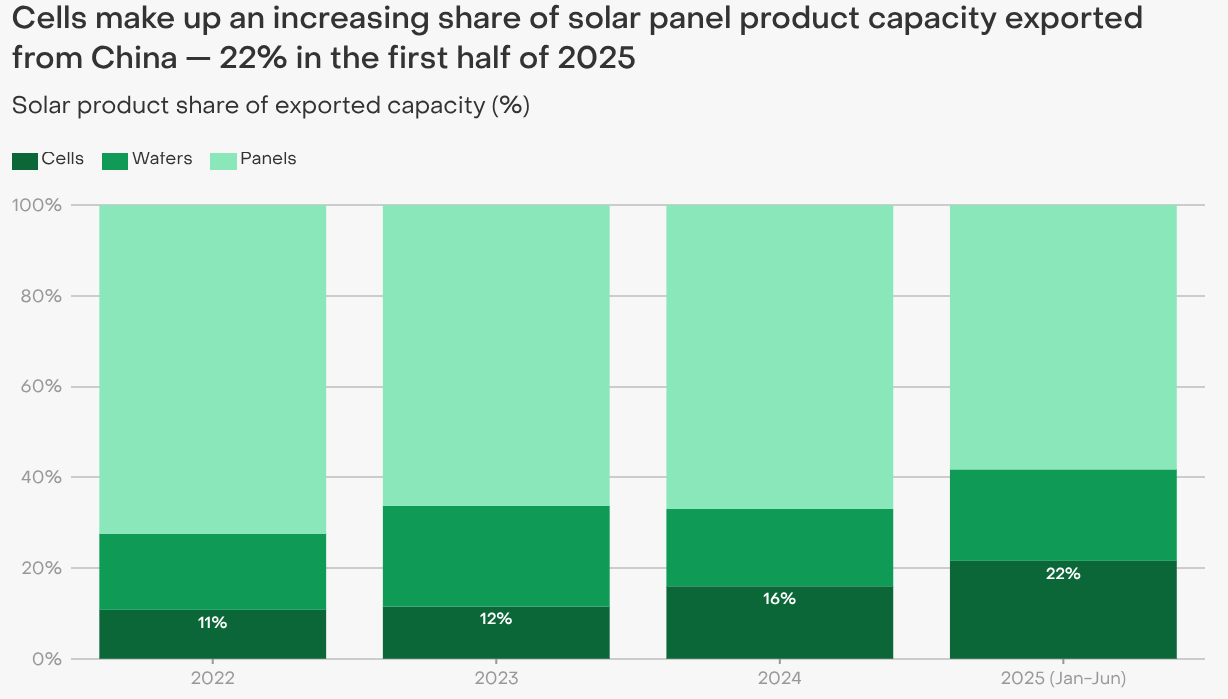

While China's exports of finished solar panels have begun to stagnate, falling by 5.2% year-over-year in the first half of 2025, its exports of higher-value, more technologically intensive components have surged. Over the same period, exports of solar cells grew by 76%, and exports of solar wafers increased by 26%. These upstream components now constitute over 40% of China's total solar product exports, a dramatic shift from previous years.

This is not a sign of weakness, but a calculated response to Western industrial policy. As the United States, Europe, and India implement tariffs and subsidies—such as the U.S. Inflation Reduction Act—to incentivize domestic panel assembly, they aim to "onshore" the final, least complex stage of the manufacturing process. Rather than fighting a low-margin battle against these protectionist measures, Chinese firms are strategically ceding this final assembly step. They are instead leveraging their immense economies of scale and technological lead to consolidate their control over the most critical and capital-intensive upstream segments of the value chain: the production of polysilicon, ingots, wafers, and high-efficiency cells. The 82% collapse in solar cell prices since late 2022, driven by this massive Chinese capacity, makes it economically unfeasible for new entrants in other countries to compete without sustained, large-scale government subsidies.

The result? A victory for the West. The new panel assembly plants being built in Arizona or Gujarat do not represent a genuine reduction in dependency on China. Instead, they represent a shift in dependency to a more critical, harder-to-replace link in the supply chain. These new Western factories are, in effect, tethered to a Chinese-controlled upstream ecosystem. For investors, this creates a clear risk profile: Western solar panel assemblers, despite being the intended beneficiaries of domestic policy, carry a significant and under-appreciated geopolitical supply risk. The true pricing power and long-term strategic value remain concentrated in the hands of China's upstream industrial champions.

A leap towards energy independence

Beyond its dominance in solar, China is aggressively pursuing a dual-track strategy in next-generation nuclear power that could fundamentally alter the global energy map and grant it the long-sought prize of energy independence. This ambition is most evident in its rapid progress in both pure nuclear fusion and hybrid fusion-fission technologies.

In the realm of nuclear fusion, China's state-backed artificial sun projects are consistently achieving world-first milestones. The Experimental Advanced Superconducting Tokamak recently set a new world record by sustaining a stable, high-confinement plasma operation for an unprecedented 1,066 seconds, more than doubling its previous record. This achievement is a critical step toward the goal of continuous power generation. Concurrently, the new-generation HL-3 tokamak has reached groundbreaking temperatures for both atomic nuclei and electrons, surpassing 100 million degrees Celsius for both simultaneously for the first time. These are not merely scientific curiosities; they are tangible engineering advances that are solving the core challenges of containing and sustaining the reactions needed for fusion energy.

Even more significant from a near-term commercial perspective is the hybrid fusion-fission Xinghuo project. This revolutionary design uses the high-energy neutrons from a fusion reaction to trigger a more efficient fission reaction in surrounding materials, promising to maximize energy output while minimizing long-lived radioactive waste. With a reported budget of approximately $2.76 billion, the Xinghuo plant is planned to be the world's first commercial-scale reactor of its kind, aiming for connection to the national grid by 2030. This timeline is remarkably aggressive, positioning China to potentially leapfrog the international ITER fusion research project in France, which is not expected to be operational until 2035 at the earliest.

This determined push into advanced nuclear technology is driven by a core strategic imperative. China's greatest geopolitical vulnerability is its profound dependence on imported fossil fuels, a dependency that exposes it to volatile global energy prices, requires payment in U.S. dollars, and relies on maritime supply routes that can be interdicted. A breakthrough in fusion or fusion-fission power offers a definitive solution to this strategic dilemma, providing a path to a near-limitless, domestically controlled, and clean source of baseload energy.

Achieving this goal would not only secure China's energy independence but would also position it as the world's leading exporter and standard-setter for the most advanced energy technology of the 21st century. This would create a new vector of technological dependency for developing nations, reinforcing China's global influence in a manner analogous to the way oil has shaped geopolitics for the last century. While direct investment in these state-controlled mega-projects is largely inaccessible, the long-term ripple effects present clear signals for investors. It points to a structural bearish outlook for nations whose economies are heavily reliant on fossil fuel exports. Conversely, it suggests a long-term bullish case for the ecosystem of companies that supply the specialized materials (like superconductors), advanced robotics, and high-precision control systems essential for the construction and operation of these next-generation nuclear facilities.

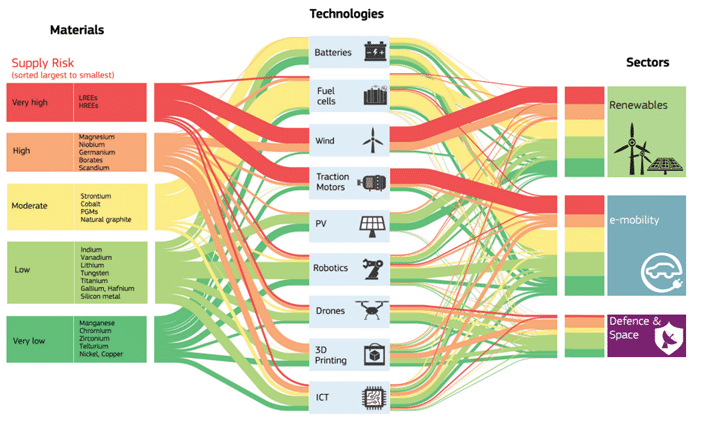

Raw material crisis

The ambitious green energy targets set by Western nations are built upon a fragile and dangerous foundation: a near-total dependency on China for the critical raw materials required for their construction. This dependency is not a market accident but the direct result of a strategic failure by the West to secure its own supply chains.

The data paints a stark picture of this vulnerability. China currently processes or refines 95-97% of the world's rare earth elements (essential for wind turbine magnets and EV motors), 100% of the refined natural graphite used in battery anodes, 70% of the global cobalt supply, and nearly 60% of both lithium and manganese. This dominance extends across the entire green-tech spectrum. China also controls at least 60% of the global manufacturing capacity for solar panels, wind systems, and batteries. Recognizing this acute risk, the European Union has enacted a Critical Raw Materials Act, which sets a goal of depending on no single third country for more than 65% of any strategic raw material by 2030. However, this is a distant and ambitious target that does little to address the immediate vulnerability.

This dependency is being actively weaponized. Global export restrictions on critical raw materials have increased fivefold since 2009, with China leading the way by placing controls on gallium and germanium exports, which are crucial for semiconductors and renewable technologies. This creates a precarious situation where the West's ability to meet its climate goals is subject to the geopolitical whims of its primary strategic rival.

This situation is the result of a fundamental and self-inflicted policy paradox in the West. For decades, Western governments have simultaneously promoted a rapid transition to green technologies while actively discouraging the domestic mining and refining of the necessary raw materials through stringent environmental regulations, complex permitting processes, and local opposition. This has created an irreconcilable conflict between stated policy goals and practical industrial capability.

China, operating without such self-imposed constraints, has systematically exploited this strategic gap. It has aggressively secured mining rights across Africa and Latin America and invested heavily in building out its domestic refining and processing capacity. In effect, the West has outsourced the most environmentally challenging and capital-intensive parts of the clean energy supply chain to China. This has allowed Beijing to achieve its dominant position not just through industrial prowess, but by capitalizing on the internal policy contradictions of its competitors.

This presents a clear and compelling investment dichotomy. The most significant bottleneck, and therefore the most compelling long-term investment opportunity, in the Western energy transition lies not in the deployment of finished products like EVs or wind farms, but in the urgent need to build a secure and resilient upstream supply chain. This points to a structural bull case for mining and processing companies that operate in politically stable, non-Chinese jurisdictions such as Australia, Canada, and Chile. It also creates tailwind for innovative recycling and urban mining companies that can create a circular economy for these strategic materials, thereby reducing primary extraction demand. Conversely, Western companies that are heavily exposed to the current fragile supply chain—from electric vehicle manufacturers to wind turbine producers—face a significant and persistent risk to their margins and production capabilities.

U.S. volatility and european instability

In the current investment regime, political and policy decisions are increasingly supplanting traditional economic fundamentals as the primary drivers of market outcomes. Investors must now analyze the political landscape with the same rigor they apply to balance sheets and economic data. Two critical focal points of this policy-driven volatility are the intense pressure being exerted on the U.S. Federal Reserve and the deepening political fragmentation that is paralyzing Europe's core economies. Navigating this environment requires a tactical approach that anticipates policy shifts and their second-order effects on asset prices.

The Federal Reserve under siege

The U.S. Federal Reserve is facing an unprecedented political pressure campaign that threatens its long-standing independence and creates significant uncertainty for monetary policy. President Donald Trump has publicly and repeatedly called for the central bank to enact aggressive interest rate cuts, demanding a reduction in the federal funds rate from its current level of 4.3% to as low as 1.3%. This campaign has escalated to include an attempt to remove Governor Lisa Cook from the Fed's board, a move widely seen as an effort to install a more politically compliant majority. The market has taken note of this pressure, with futures pricing indicating a high probability of a rate cut at the Federal Reserve's September meeting.