[INTEL REPORT] Markets priced vs. fiscal reality Q4 2025

Valuations, negative ERP, and a selective, real-asset tilt for Q4 2025

Table of contents:

Introduction.

Markets at the peak of the cycle.

The Sovereign bebt, latent risks and central bank lifelines.

The politicization of policy.

Structural shifts in the economy.

Separating transformational technology from speculation.

Europe's structural malaise.

The new geopolitical map.

Investment strategy for Q4 2025.

Defensive pivot.

Selective value.

Fixed income.

Alternative investments.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

By September 2025, global markets are showing signs of dangerous complacency. Equity benchmarks sit at historic highs, valuations have expanded far beyond long-term averages, and volatility has been suppressed to levels inconsistent with the scale of macroeconomic and geopolitical risks. This calm is not grounded in fundamentals, but in the assumption that central banks and governments will always intervene to support asset prices.

If you want to know more about their fragile structure, check this:

That assumption is increasingly fragile. Major economies are burdened with unprecedented public debt, fiscal deficits are widening, and the policy tools once used to backstop markets are constrained by inflationary pressures and political interference. Investors are effectively betting that monetary authorities can deliver flawless execution of easing cycles at a time when their independence and credibility are under strain. History shows that faith in policy omnipotence tends to hold until the moment it suddenly breaks, and today’s market structure leaves little room for error.

Meanwhile, the global order is fragmenting in ways that will have lasting implications for capital allocation. The U.S. faces a visible erosion of institutional stability and rule-of-law predictability. Europe struggles with stagnation, demographic headwinds, and political fracture. At the same time, rival blocs led by China and Russia are building parallel systems of trade, finance, and technology standards, accelerating a world of competing “stacks” rather than a single global market. These shifts are structural, not cyclical, and they threaten to upend long-standing assumptions about reserve currencies, supply chain resilience, and the pricing of sovereign risk.

This backdrop leaves investors confronting a market priced for policy perfection but operating in a world of political dysfunction, fiscal exhaustion, and strategic rivalry. The traditional playbook of buying dips is obsolete. Instead, resilience must come from a defensive stance—one that emphasizes capital preservation, selective exposure to genuine value, and diversification into real assets and hedges that are less dependent on central bank support.

This report lays out the case for why the cycle is turning, identifies the underappreciated risks shaping the next phase of markets, and highlights where opportunities can be found amid the inevitable dislocations. The objectives are:

To survive heightened volatility.

To position portfolios for advantage.

Markets at the peak of the cycle

The central theme confronting investors in the latter half of 2025 is a divergence between euphoric market pricing and deteriorating underlying fundamentals. Global equity markets are trading on a fragile narrative of imminent and substantial policy easing, pushing valuations to levels that leave no margin for error.

The prevailing sentiment across trading desks is one of triumphant optimism. Markets are celebrating what appears to be a resilient global economy that has weathered the aggressive monetary tightening of 2022-2023, coupled with the tantalizing prospect of a coordinated central bank easing cycle. The U.S. Federal Reserve, in particular, is the focal point of this bullish narrative. Following a series of weak labor market reports and a more dovish tone from Chairman Jerome Powell, markets are pricing in a near-certainty of a rate-cutting cycle beginning in September, with expectations for multiple cuts extending through the remainder of 2025 and into 2026.

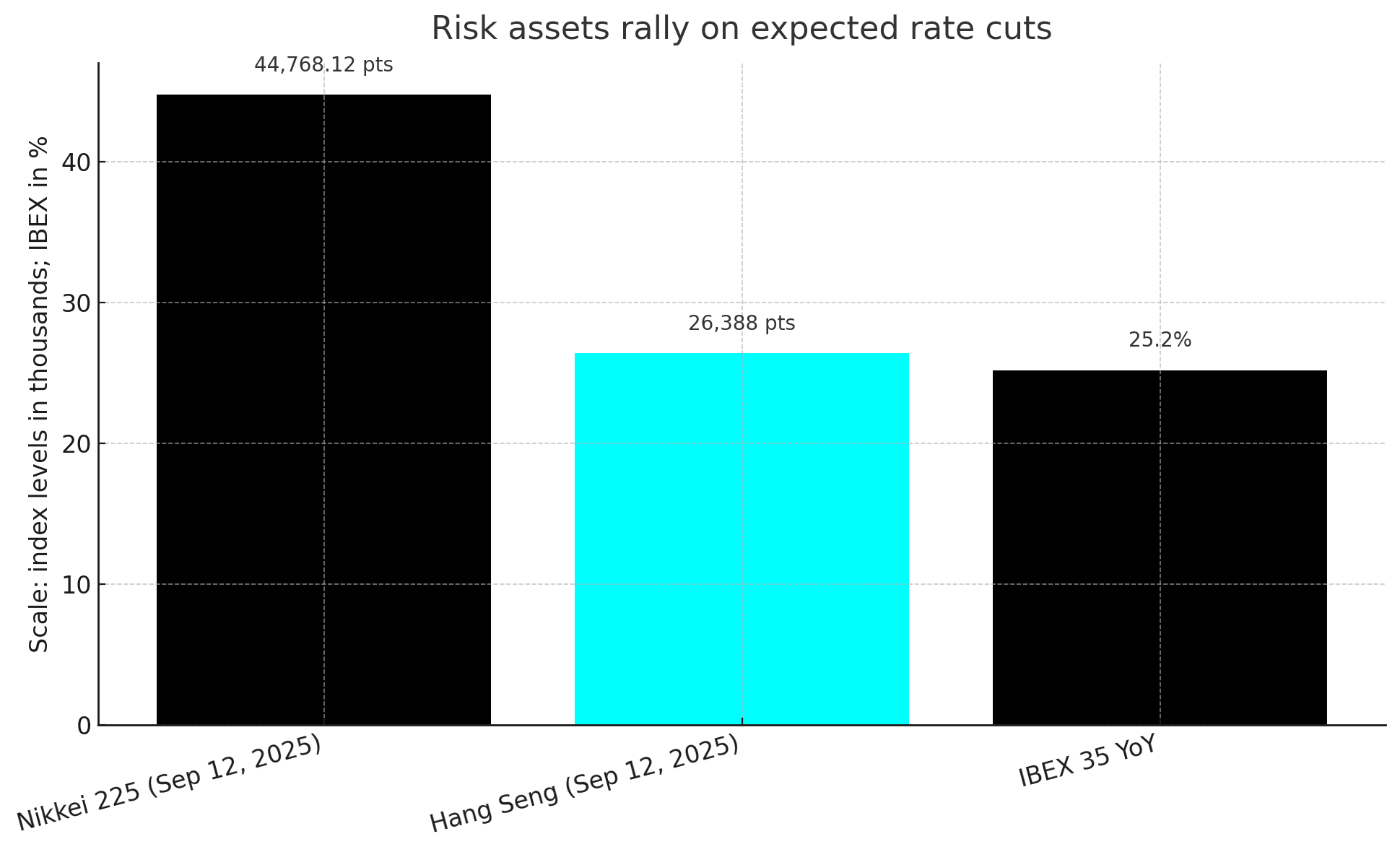

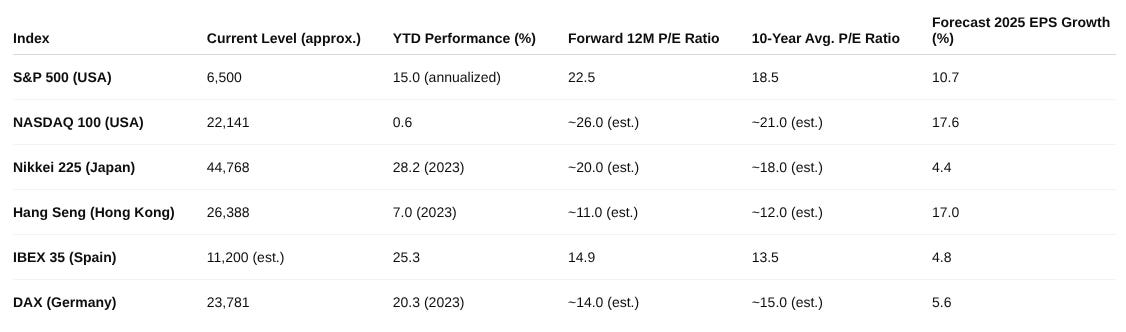

This anticipation of cheaper capital has acted as tailwind for risk assets, propelling major indices to record or multi-year highs. Japan's Nikkei 225 index has been a standout performer, closing at a remarkable 44,768.12 on September, 2025, capping a year of strong gains. In Hong Kong, the Hang Seng Index surged to a four-year high of 26,388 on the same day, fueled by the global rate-cut speculation. European markets have also participated in the rally, with Spain's IBEX 35 index posting a 25.2% gain over the past year. This robust performance has defied the historical weakness typically associated with the month of September, as investors look past near-term geopolitical and economic risks toward a future defined by lower borrowing costs and abundant liquidity.

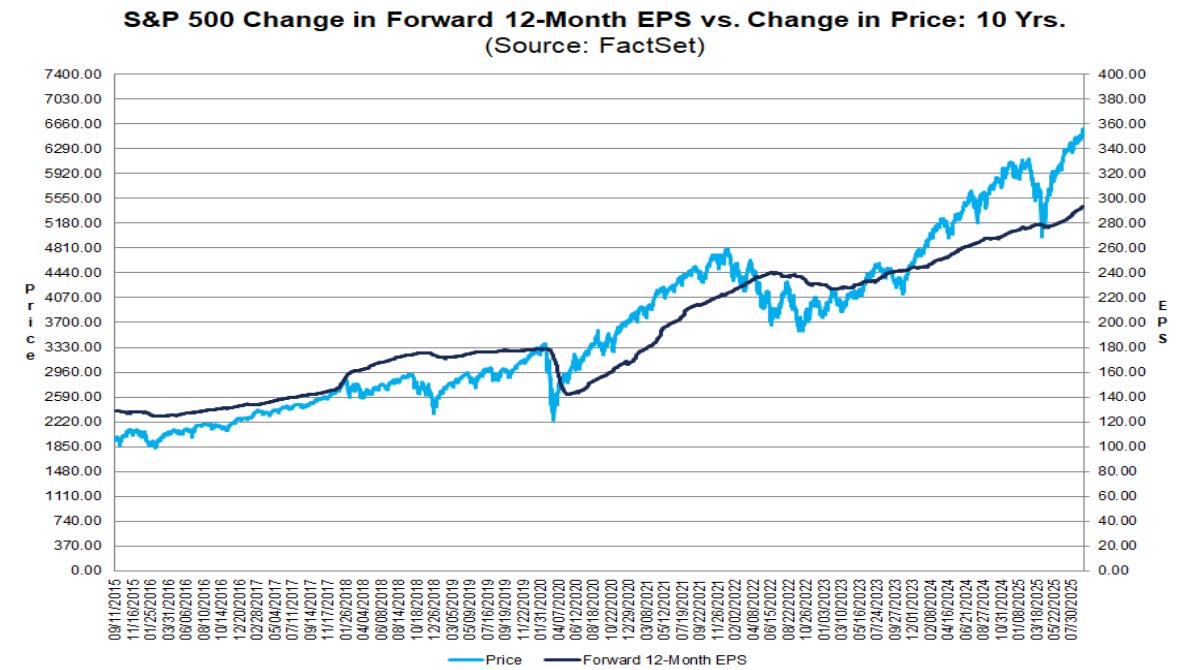

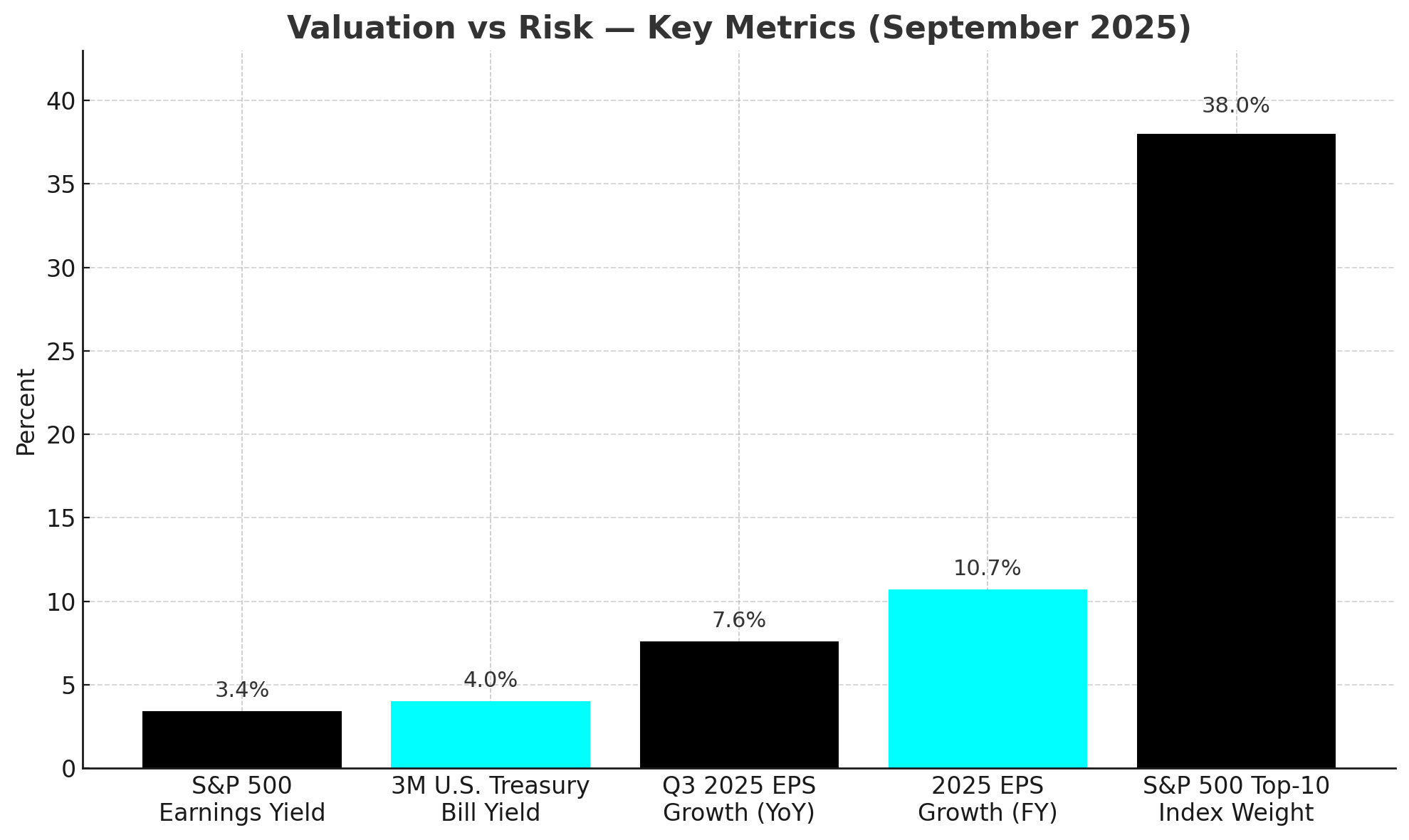

This wave of policy-driven optimism has stretched equity valuations to levels that are not only historically extreme but fundamentally unsustainable without the flawless execution of a dovish pivot by central banks. The S&P 500, the world's benchmark equity index, now trades at a forward 12-month price-to-earnings ratio of 22.5. This represents a significant premium to both its 5-year average of 19.9 and its 10-year average of 18.5. Other analyses, considering different earnings estimates, place the valuation even higher, at approximately 24 times 2025 estimated earnings per share.

The danger of this valuation premium is starkly illustrated when contrasted with risk-free rates. The S&P 500's earnings yield—the inverse of its P/E ratio—currently sits at a meager 3.4%. This is below the 4% yield offered by 3-month U.S. Treasury bills, creating a negative equity risk premium. This anomaly, where investors are compensated less for taking the risk of owning stocks than for holding short-term government debt, has not been seen since the peak of the dot-com bubble in 1999-2000, a period that immediately preceded a multi-year bear market.

While bulls point to solid corporate earnings as justification, the data suggests otherwise. The S&P 500 is forecast to deliver a respectable year-over-year earnings growth rate of 7.6% for the third quarter of 2025, with a full-year growth forecast of 10.7%. While positive, this level of growth is insufficient to justify the current valuation premium on its own. The market is not paying for current earnings; it is paying for the multiple expansion it expects to result from lower interest rates. This makes the market exquisitely sensitive to any deviation from the anticipated path of monetary easing.

The current market environment exhibits numerous characteristics of past speculative manias, most notably the periods preceding the crashes of 1929 and 2000. Key warning signs are flashing red for investors who choose to see them. First is the extreme market concentration. The top 10 constituents of the S&P 500 now account for a historically high 38% of the index's total market capitalization, creating a fragile, narrow leadership. Second is the dominance of a compelling but unproven narrative which is being used to justify valuations that are completely divorced from near-term profitability.

Finally, there is the pervasive belief that "this time is different," and that traditional valuation metrics are no longer relevant in a new economic paradigm. This combination of narrow leadership, a speculative narrative, and the suspension of disbelief is a classic recipe for a major market correction. The market is priced for policy perfection, leaving no room for the inevitable intrusion of reality.

The structure of the market has shifted in a fundamental way. It is no longer functioning as a forward-looking mechanism that discounts future economic activity and corporate profitability. Instead, it has become a self-referential machine that primarily prices the anticipated actions and reactions of central banks. The high correlation between different asset classes, where both stocks and bonds have become vulnerable to the same inflation and interest rate shocks, is a symptom of this regime change. A risk-on rally driven by liquidity expectations is lifting all boats, regardless of their individual seaworthiness, masking significant underlying weaknesses in specific regions and sectors. This dynamic is inherently unstable. If the Federal Reserve is forced to delay its cutting cycle due to re-accelerating inflation, or if its actions are perceived as insufficient to offset other economic headwinds, the entire valuation structure of the market is at risk of a sudden and violent collapse.

This addiction to policy stimulus has fostered a moral hazard. Over the past decade, investors have been conditioned to believe that central banks will always provide a backstop in times of stress, effectively privatizing gains while socializing losses. This belief incentivizes market participants to ignore fundamental risks and increase leverage, confident that they will be bailed out by a flood of liquidity at the first sign of trouble. This behavior inflates asset bubbles and dramatically increases the severity of the eventual correction, which occurs when the backstop proves insufficient, is withdrawn, or is overwhelmed by the scale of the crisis. The current calm in the markets should not be mistaken for stability; it is the complacency born from this deep-seated moral hazard.

The Sovereign bebt, latent risks and central bank lifelines

Beneath the placid surface of global equity markets lies a deep and widening fault line in the sovereign bond market. Major developed economies are encumbered by unsustainable levels of public debt, a situation that has been papered over, but not resolved, by years of unprecedented central bank intervention.

The fiscal position of the G7 nations has deteriorated to levels not seen since the immediate aftermath of World War II. As of mid-2025, public debt-to-GDP ratios have reached alarming heights across the developed world. Japan leads this dubious ranking with a staggering ratio of approximately 237%. The United States follows with debt at 124.3% of GDP, France at 116.3%, and the United Kingdom at over 100%.

These are not merely historical artifacts of past crises; they are actively worsening. The U.S. government deficit is projected to remain above a deeply unsustainable 6% of GDP for the foreseeable future, continuously adding to its $37 trillion debt pile. Similarly, France's budget deficit is hovering near 6%, and its public debt is on a trajectory to exceed 118% of GDP by 2026. This relentless accumulation of debt is occurring in an environment of rising interest rates, creating a toxic feedback loop where higher borrowing costs increase deficits, which in turn necessitates even more borrowing.

After years of dormancy during the era of quantitative easing, market discipline is reasserting itself. The so-called bond vigilantes—investors who sell government bonds to protest inflationary or fiscally irresponsible policies—are stirring once again. Their actions are visible in the rising compensation, or term premium, that investors are demanding to hold long-dated government debt in the face of persistent deficits and political instability.

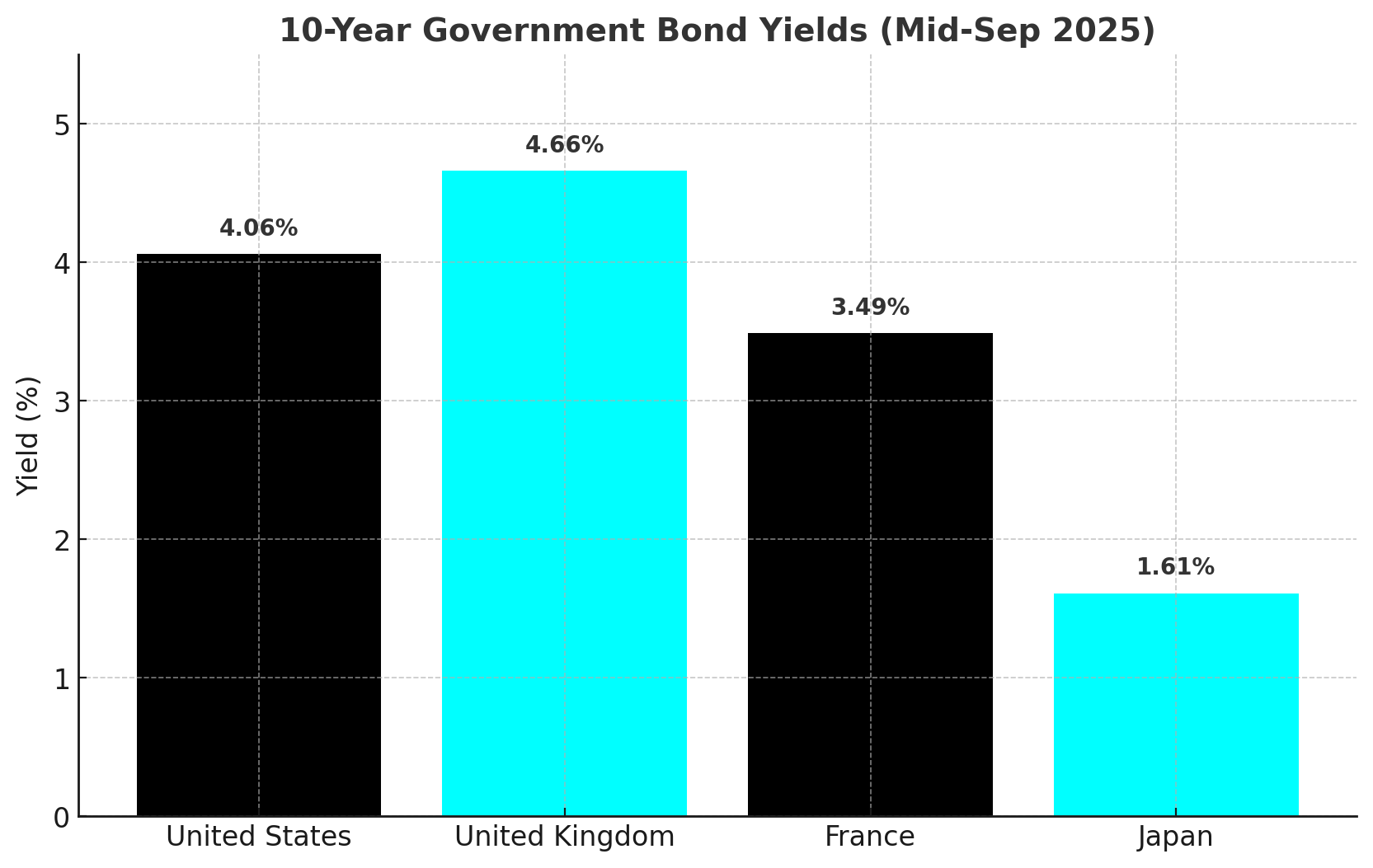

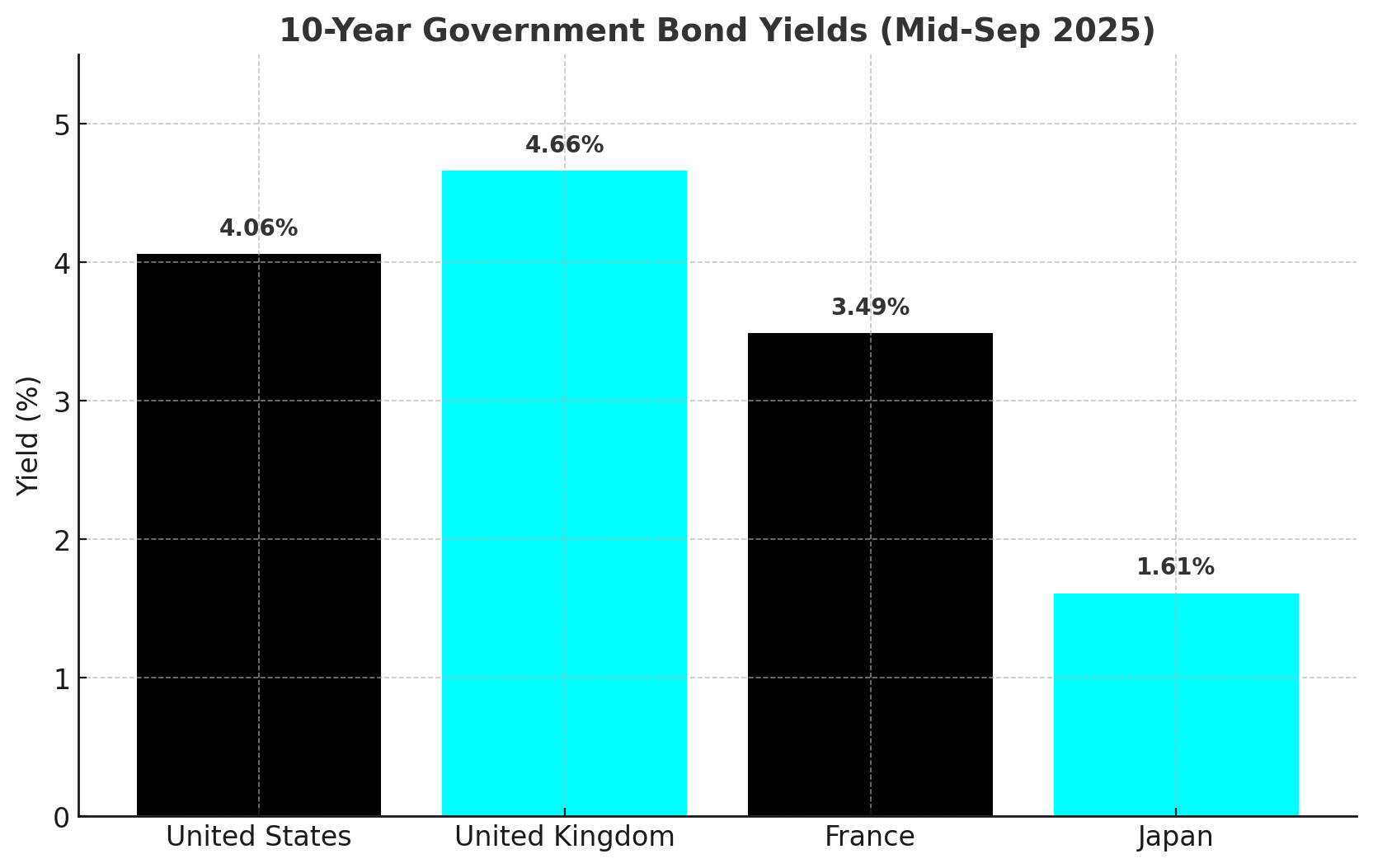

This renewed vigilance is reflected in a broad-based sell-off in long-term government bonds, pushing yields significantly higher. As of mid-September 2025, the yield on the benchmark 10-year U.S. Treasury note stands at 4.06%. In the United Kingdom, the 10-year gilt yield has climbed to 4.66%. The situation is particularly acute in France, where political turmoil has pushed the 10-year bond yield to 3.49%, at times exceeding the yield on historically riskier Italian debt—a clear signal of acute market stress. Even in Japan, where yields have been suppressed for decades by the central bank, the 10-year government bond yield has risen to 1.61%, a multi-decade high that signals a major regime shift. In response to this deteriorating fiscal outlook, major institutional investors are taking defensive action. PIMCO, one of the world's largest bond managers, has publicly stated it is reducing allocations to longer-dated U.S. government bonds, a clear vote of no confidence in the long-term fiscal sustainability of the world's primary reserve issuer.

The primary reason a full-blown sovereign debt crisis has not yet erupted is the presence of a powerful, if sometimes unspoken, central bank backstop. The financial system is operating under the assumption that monetary authorities possess both the tools and the political will to intervene to prevent a disorderly collapse in bond markets. This assumption is not without merit. The Bank of England, having learned the harsh lessons of the 2022 Liability-Driven Investment crisis, has institutionalized its emergency response by creating the Contingent Repo Facility. This facility is designed to provide backstop liquidity to non-bank financial institutions, such as pension funds, to prevent the kind of forced selling of gilts that nearly brought the UK financial system to its knees.