[INTEL REPORT] Global multi-asset outlook: H2 2025

From Fed policy shifts and trade tensions to dollar dynamics and alternative assets

Table of contents:

Introduction.

Macroeconomic and geoplotical chessboard.

Interest rate policy and its market impact.

Tariffs, trade wars, and global instability.

The US dollar index and the dollar milkshake thesis.

Sentiment and market risk.

Commitment of Traders reports.

US equities.

Scenarios: Bull, base, and bear cases for Nasdaq.

Precious metals.

Fundamental drivers: Central banks, deficits, and de-dollarization.

Scenarios: Bull, base, and bear cases for Gold.

Bitcoin.

Scenarios: Bull, base, and bear cases for Bitcoin.

Strategy, allocation, and risk management.

Audio Note: Before we begin, remember that if you’re accessing this article through the Substack app, you can listen to it instead of reading it. The MarketOps section is best suited for this format.

Before you begin, remember that you have an index with the newsletter content organized by clicking on the image below.

Introduction

The consensus economic outlook for the remainder of 2025 is one of notable deceleration, marked by a delicate and potentially unstable balance between moderating growth and stubbornly high inflation. The market appears to have largely absorbed the initial news of a weaker first quarter, but the underlying drivers of this slowdown present significant headwinds for the months ahead.

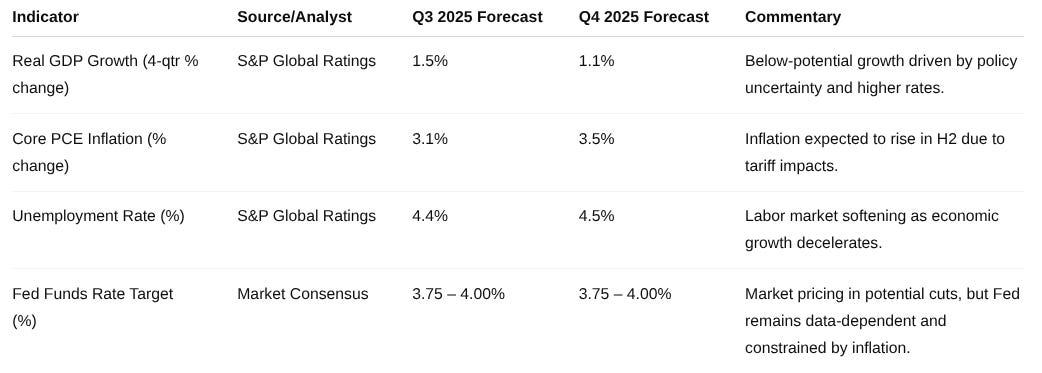

S&P Global Ratings projects a below-potential U.S. real GDP growth of 1.7% for the full year 2025, with a more pronounced slowdown expected in the latter half, weakening to just 1.1% by the fourth quarter. This forecast is broadly consistent with projections from the Congressional Budget Office, which anticipates growth cooling to 1.9% in 2025 from 2.3% in 2024. This slowdown is attributed to a confluence of factors, including slower population growth, federal government cost-cutting initiatives, and the persistent drag of higher interest rates on business and residential investment.

Inflation remains the pivotal variable. While there have been some indications of easing price pressures, core inflation remains well above the Federal Reserve's 2% target. More concerning is the forecast that core Personal Consumption Expenditures inflation—the Fed's preferred gauge—is expected to rise to a range of 3.0% to 3.5% by the end of 2025. This anticipated increase is not organic but is largely a consequence of looming tariff policies, which are expected to push up the cost of imported goods once retailers deplete their existing inventories.

This dynamic—slowing growth combined with resurgent inflation—evokes the market's underlying fear of stagflation, a term mentioned in the initial market analysis. A stagflationary environment is particularly challenging for investors, as it typically exerts downward pressure on both equities due to lower earnings and bonds due to high inflation and interest rates simultaneously. A dangerous feedback loop appears to be forming: proposed tariffs fuel inflation, which in turn constrains the Federal Reserve's ability to support the economy with rate cuts. This policy paralysis then exacerbates the economic slowdown, creating the very stagflationary conditions that markets fear most.

Rules have changed so take a look of this:

Reflecting this precarious outlook, the labor market is also showing signs of softening. The unemployment rate is projected to climb to 4.6% by the first half of 2026, up from current levels, indicating an improved but weakening balance between labor supply and demand. Consequently, the subjective probability of a U.S. recession beginning within the next 12 months has been raised to a range of 30%-35%, a significant risk driven almost entirely by the high degree of policy unpredictability.

Macroeconomic and geoplotical chessboard

The investment landscape for the second half of 2025 is defined by a complex interplay of slowing economic growth, persistent inflation, and significant geopolitical friction. Understanding this environment requires a foundational understanding of the macroeconomic factors that will dictate market direction. Let’s take a look of the prevailing economic outlook, the critical role of central bank policy, the tangible impact of geopolitical risks, and the central importance of the U.S. dollar.

More about that in:

Interest rate policy and its market impact

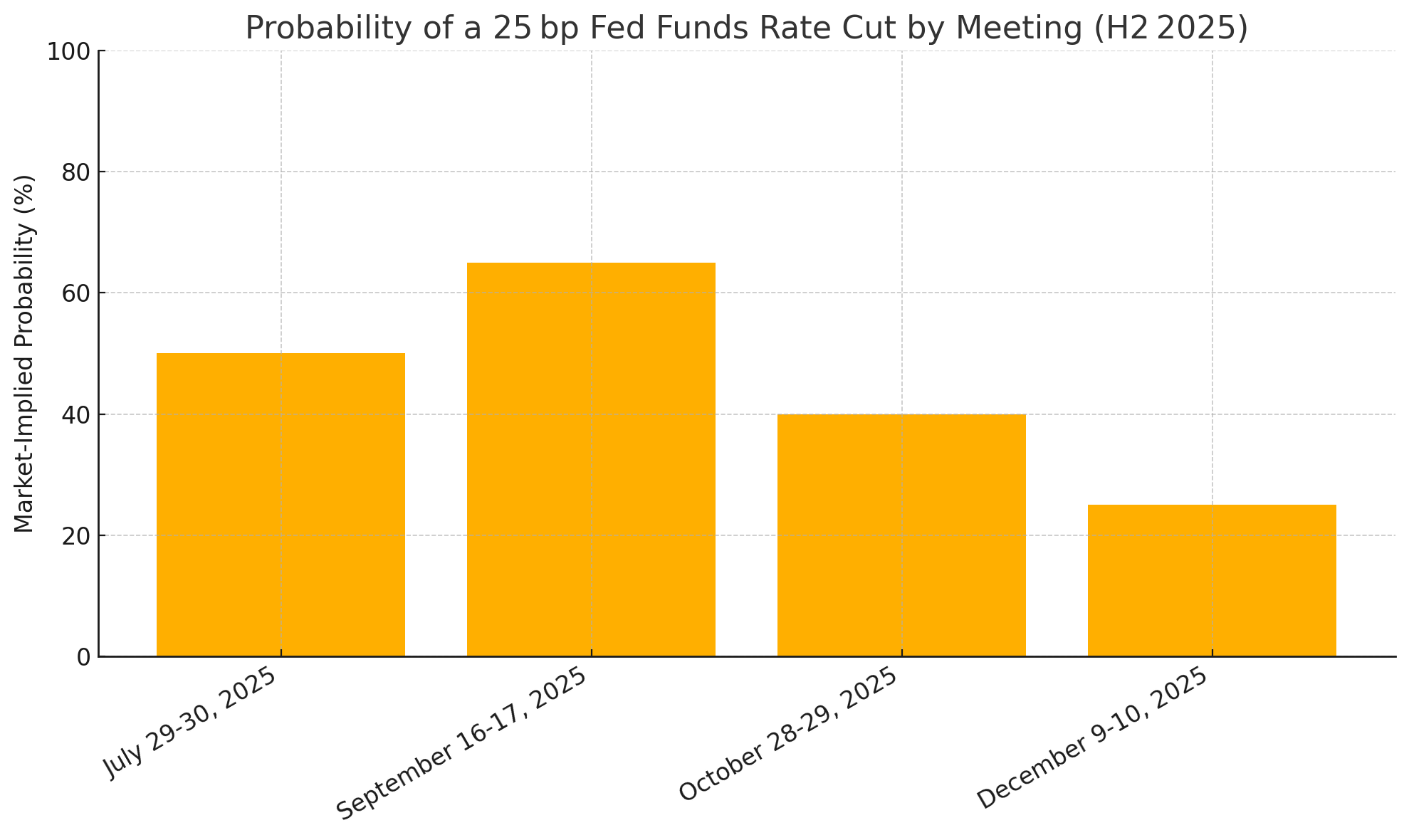

The Federal Reserve stands at the center of the market's focus for the second half of 2025. With weak economic data largely priced in, investor attention has shifted almost entirely to the prospect of monetary easing. The market is currently pricing in the possibility of one or two 25-basis-point rate cuts before the end of the year, with potential timing in the July or September meetings. The scheduled Federal Open Market Committee meetings on July 29-30, September 16-17, October 28-29, and December 9-10 are therefore the most critical dates on the economic calendar, each capable of inducing significant market volatility.

However, a significant and dangerous divergence exists between the market's expectations and the Fed's operational reality. While asset markets, particularly the Nasdaq, have rallied to all-time highs on the assumption of a dovish pivot, Fed officials remain publicly cautious. Fed Chair Jerome Powell's recent congressional testimony offered only subtle hints of a more open tone toward future cuts, carefully avoiding any firm commitment. The primary obstacle is the lingering inflation impulses, which are now at risk of being reignited by the tariff policies discussed previously.

This creates a state of fragile dependency where market valuations are predicated on a future policy path that may not be achievable. The market is not trading on current robust fundamentals but rather on the hope of future liquidity injections from the Fed. Each major inflation report, such as the upcoming consumption deflator data, and every FOMC statement now functions as a binary event. A lower-than-expected inflation print or a dovish statement from the Chair could validate the market's optimism and extend the rally. Conversely, a high inflation reading or a hawkish tone emphasizing the continued fight against inflation could shatter the narrative, triggering a rapid and severe repricing of risk assets. This divergence between market desire and central bank capacity represents the primary source of systemic risk for the second half of the year.

Tariffs, trade wars, and global instability

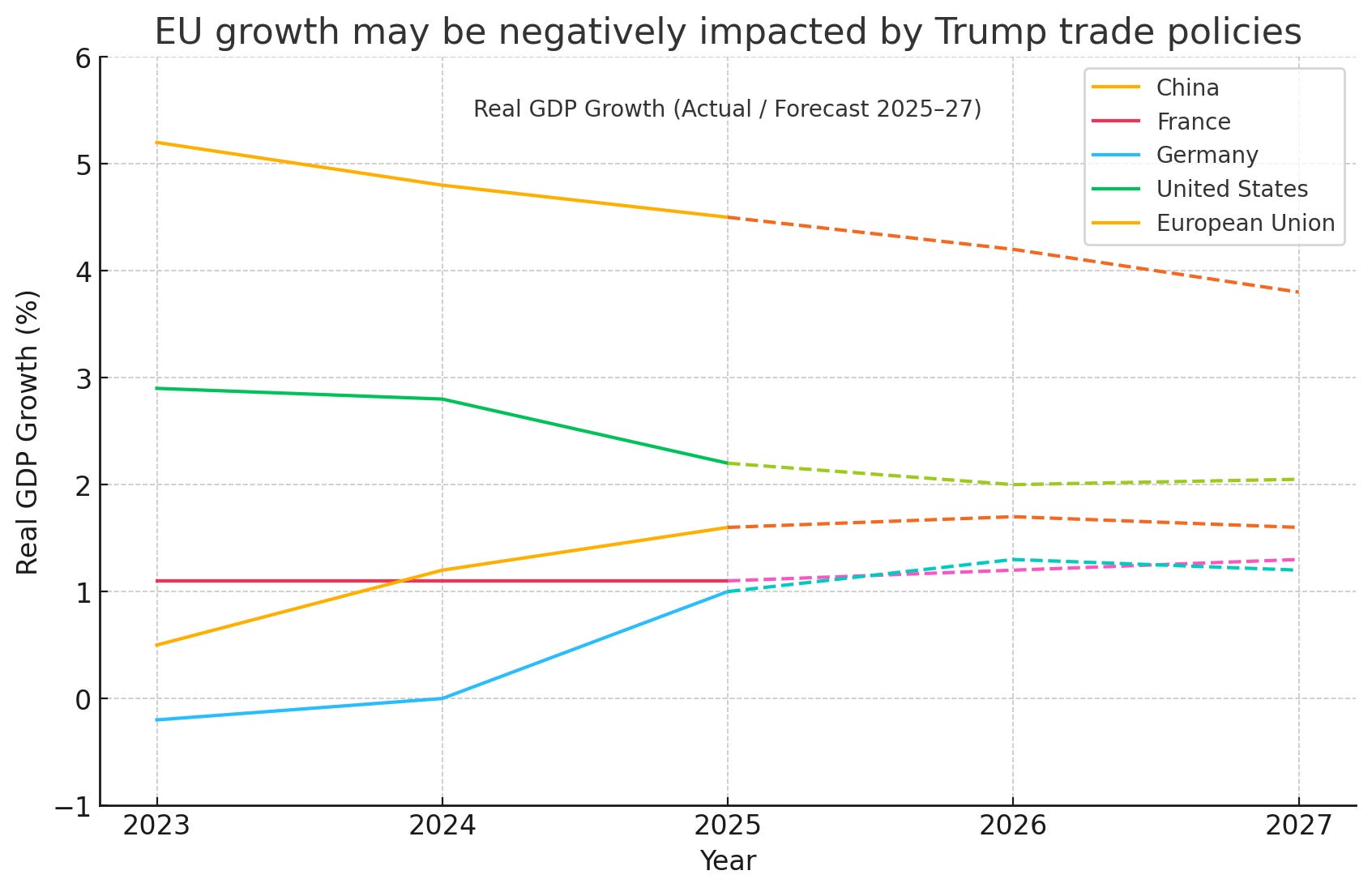

While the recent de-escalation of tensions in the Middle East provided a temporary wave of relief and a boost to risk assets, the more structural and impactful geopolitical risk for 2025 is the rising threat of a global trade war. A potentially more protectionist U.S. economic approach, with proposed tariffs of up to 60% on Chinese goods and 20% on other major trading partners, threatens to fundamentally upend the status quo.

It is critical for investors to view this risk not as a vague driver of market sentiment but as a direct and quantifiable input into economic and corporate fundamentals. Tariffs are, by definition, a tax on consumption and a direct cost increase for businesses that rely on global supply chains. Companies faced with these higher costs have two choices: absorb them, which directly compresses profit margins and lowers earnings, or pass them on to consumers, which directly fuels the inflation that the Federal Reserve is trying to combat.

This dynamic forces a rewiring of global trade flows, a costly and uncertain process that will create a new set of economic winners and losers. The uncertainty surrounding the timing, scope, and retaliatory response to these tariffs weighs heavily on business investment decisions and is a key factor in the subdued GDP growth forecasts. As the market moves into the Q3 earnings season, corporate guidance on the expected impact of these trade policies will be scrutinized intensely and could be a major catalyst for market volatility. Other global flashpoints, including the ongoing war in Ukraine and tensions in Asia, add layers of complexity and potential for unexpected shocks, but the U.S.-China trade relationship remains the central geopolitical issue for financial markets in 2025.

The US dollar index and the dollar milkshake thesis

The direction of the U.S. Dollar Index is arguably the single most important variable for the multi-asset outlook in the second half of 2025. The initial analysis provided paints a bearish picture, suggesting the dollar is in free fall as it discounts future Fed rate cuts. This view is supported by technical analysis showing a breakdown of key long-term support levels around 97.5-98.0, with a potential downside target near 90. The bearish fundamental case is underpinned by concerns over mounting U.S. government debt and persistent trade deficits.

However, a potent and non-consensus bullish case for the dollar must be considered as a primary risk scenario. This outlook is driven by three main factors:

U.S. economic outperformance: As detailed previously, the U.S. economy, while slowing, continues to show more resilience than other developed economies in Europe and Japan.

Monetary policy divergence: While the Fed is contemplating cuts, other major central banks may be forced to ease policy more aggressively, maintaining a favorable interest rate differential for the dollar.

Inflationary impact of tariffs: As discussed, tariffs are inflationary. Persistent inflation would force the Fed to delay rate cuts, contradicting the market's primary bearish thesis for the dollar and leading to a potential repricing higher.

This bullish scenario is encapsulated by the Dollar Milkshake Theory. This theory posits that the U.S. dollar's unique position as the world's primary reserve currency and unit of debt creates a paradoxical situation. In a global crisis or a period of synchronous monetary tightening, the global financial system's immense demand for dollars to service debts and find safe-haven assets sucks capital into the U.S. This creates a massive dollar rally, even if the U.S. is the source of the instability.

The path of the DXY acts as a lynchpin for all other asset classes discussed previously. If the bearish consensus view holds and the dollar weakens, it would provide a significant tailwind for assets priced in dollars, such as Gold and Bitcoin, and would also be supportive of U.S. multinational stocks with large foreign earnings. However, if the bullish Dollar Milkshake scenario unfolds—potentially triggered by an escalating trade war or another global shock—the consequences would be severe.

A surging dollar would exert immense pressure on Gold and Bitcoin, tighten global financial conditions, strain emerging markets, and likely trigger a broad, risk-off event in equities. Therefore, an investor's entire strategic positioning for H2 2025 hinges on their view of the dollar, making the DXY the master variable to watch.

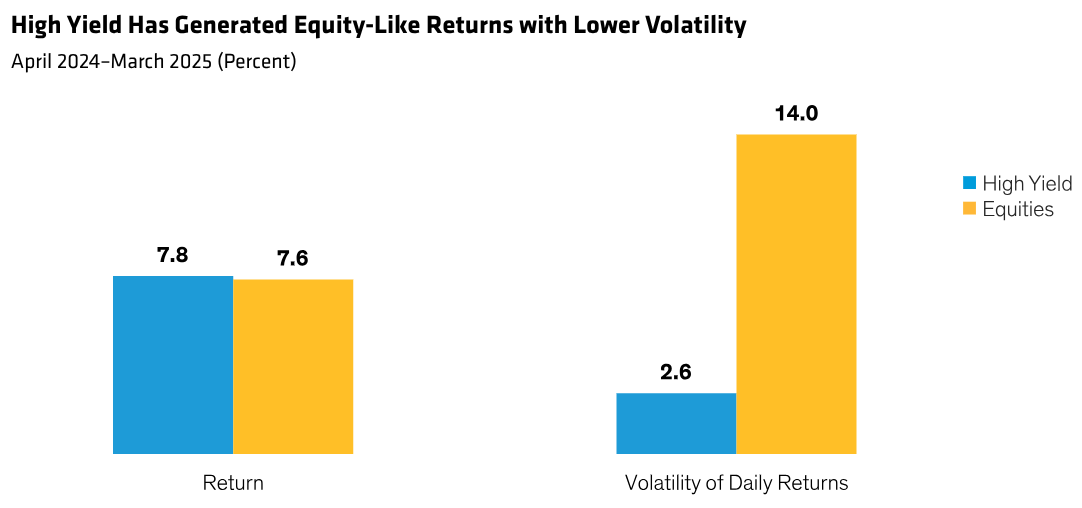

Sentiment and market risk

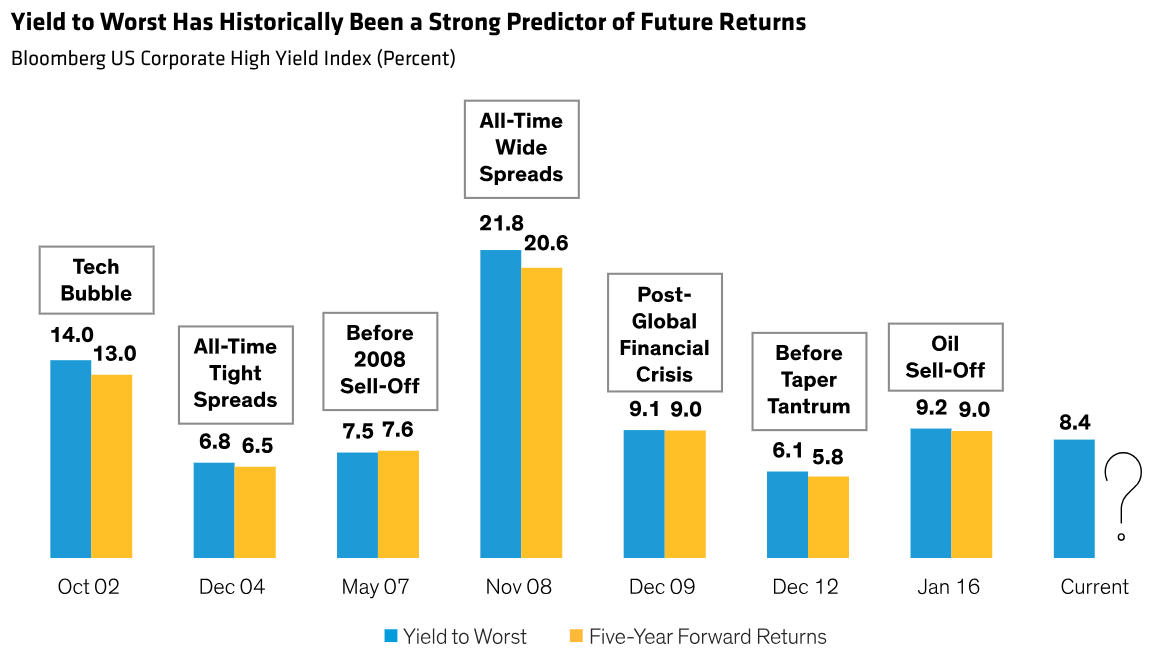

As identified in the initial market analysis, the iShares iBoxx High Yield Corporate Bond ETF serves as an excellent barometer for the market's appetite for risk. Because high-yield bonds are issued by companies with weaker credit profiles, investor willingness to buy these bonds reflects confidence in the economic outlook and corporate profitability. The price action of HYG is highly correlated with the stock market, often acting as a leading indicator for broad risk sentiment.

Currently, the signal from HYG is overtly positive. The ETF is trading at or near historical highs, exhibiting a strong upward trend with significant verticality. This suggests that investors are not currently fearful of widespread corporate defaults and are comfortable taking on credit risk.